A Tightening Cycle Could Last Up to a Year, With Focus on Narrowing the Korea-U.S. Rate Gap [Market Watches Shin Hyun-song's Rate Hike Move]

- Input

- 2026-07-12 18:21:11

- Updated

- 2026-07-12 18:21:11

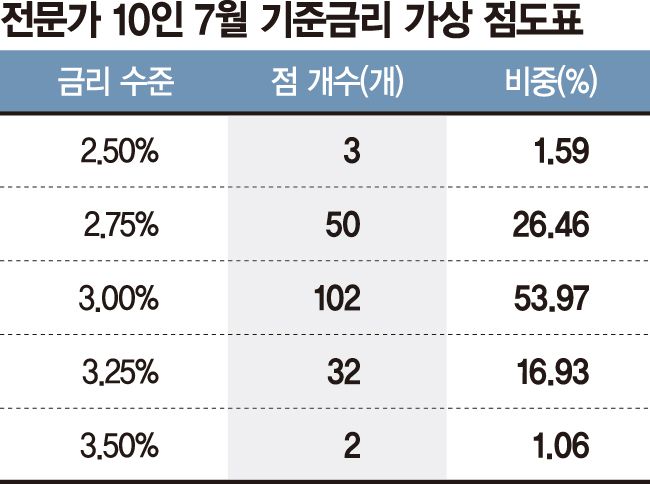

On the 12th, Financial News asked 10 market experts about a hypothetical July dot plot, which the Bank of Korea releases in February, May, August and October. Excluding one respondent who gave no opinion, 102 of the 189 total dots from the remaining nine experts were placed at 3.00%. That accounts for 54.0% of the total. All respondents agreed that the Monetary Policy Board will raise the benchmark rate by 25 basis points this month, meaning another hike within six months is seen as likely.

A stronger tightening path was also considered possible. In that period, 32 dots were placed at 3.25%, which would mean three hikes, and two dots at 3.50%, which would mean four hikes. By comparison, 50 dots were placed at 2.75% and three at 2.50%.

The tightening cycle is generally expected to continue through the first half of next year. If it starts this month, it would be the first such cycle in three years and six months since January 2023, when the rate was raised from 3.25% to 3.50%. It is also expected to last about a year. Six of the 10 experts said the cycle would end in the fourth quarter of this year or the first quarter of next year. Their view is that after two hikes this year and one more next year, the rate would rise to 3.25% and then be held steady.

Three others pointed to the first half of next year, including the second quarter. Choi Jemin, a researcher at Hyundai Motor Securities, said, "If headline consumer inflation stays in the high 2% range and core inflation in the mid-2% range through the first quarter of next year, then falls to the mid-2% range and low-2% range in the second quarter, the rationale for further rate hikes will weaken."

Shin Eol, a researcher at Sangsangin Investment & Securities, said, "If the war in Iran does not continue, inflation could be controlled to some extent with a 50 to 75 basis point hike." He added, "Monetary policy alone cannot change the direction of the exchange rate, so it is difficult to justify additional hikes on that basis. A slowdown in domestic demand also appears unavoidable."

The remaining expert saw the tightening cycle ending after the first half of the year, when semiconductor export growth is expected to gradually slow. By then, the export-led expansion centered on semiconductors would likely fade. Overall economic growth would also have to be revised down, removing a major justification for tightening.

Next year's economic growth forecast stands at 2.1%. The International Monetary Fund (IMF) has projected as much as 2.5%, but the key point remains that growth will weaken compared with this year. Ahn Yeha, a researcher at Kiwoom Securities, said, "The board will consider whether inflation continues to rise and whether there is room to raise the economic growth forecast."

■ About 27% are paying attention to the exchange rate

The survey also found that the Monetary Policy Board is likely to weigh the rise in the won–dollar exchange rate at nearly 30% of its benchmark rate decision. The Bank of Korea has officially set price stability as the first goal of monetary policy, but with the lower bound of the exchange rate already seen at 1,500 won, it is judged to have little choice but to narrow the interest rate gap between South Korea and the United States, which underpins that level.

When 10 market experts were asked how much the rise in the won–dollar exchange rate would affect the July Monetary Policy Board meeting, the average response was 27%. Jeong Yong-taek, chief economist at IBK Investment & Securities, gave the highest figure at 50%, followed by Baek Yoon-min, a researcher at Kyobo Securities, at 40%. Other estimates included 10% from Park Sang-hyun, a researcher at iM Securities, and 15% from Lee Jae-hyung, a researcher at Yuanta Securities Korea.

Current upward pressure on the won–dollar exchange rate comes from overseas investment by domestic investors and foreign capital leaving the local stock market. But the widening interest rate gap between South Korea and the United States is seen as the main factor drawing dollars into the U.S. and reinforcing the structure of a weak won and a strong dollar. The current benchmark rate is 2.50% in South Korea and 3.50% to 3.75% in the United States.

taeil0808@fnnews.com Kim Tae-il Reporter