Europe's EV Market Revives on High Oil Prices... K-Battery Firms Poised for a Rebound Under 'Made in EU'

- Input

- 2026-07-09 05:59:00

- Updated

- 2026-07-09 05:59:00

[Financial News] As high oil prices from the Middle East persist, analysts say Europe's electric vehicle (EV) market could move beyond a simple rebound and enter a phase of structural expansion. High fuel taxes already make internal combustion engine vehicles expensive to run, and for consumers who can charge at home or at work, EVs have already secured a strong edge in total cost of ownership (TCO). On top of that, as the European Union (EU) restructures its battery supply chain around local production, the policy shift could also provide a rebound opportunity for domestic battery makers whose market share is now under pressure.

■ Economics highlighted by high oil prices, EU moves into industrial policy

According to Yuanta Securities Korea on the 8th, Europe's EV market is shaped more by operating costs and policy conditions than by vehicle prices, unlike the U.S. market. Because of high fuel taxes, the cost of running internal combustion engine vehicles is structurally high, which has made EVs' total cost of ownership more attractive. The gap is widening further as international oil prices rise again amid tensions in the Strait of Hormuz.

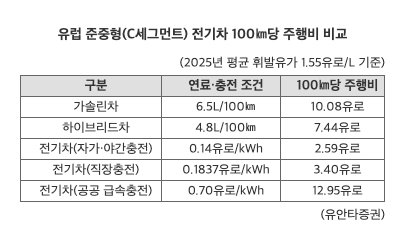

In Yuanta Securities Korea's "Secondary Battery 2H26 Outlook" report, the driving cost of a gasoline car in Europe's mid-sized C-segment is estimated at 10.08 euros per 100 km, while a hybrid costs 7.44 euros. By contrast, an EV costs just 2.59 euros with home or overnight charging, and 3.40 euros even with workplace charging.

Researcher Ianna Lee at Yuanta Securities Korea said, "In Europe, gasoline and diesel taxes are high, so the operating cost of internal combustion engine vehicles is structurally expensive. For consumers who can charge at home or at work, the fuel-cost savings of a Battery Electric Vehicle (BEV) are significant." She added, "Demand for BEVs in Europe is currently being supported by company-car users, leasing customers, high-mileage drivers, and consumers with dedicated parking, home charging, or access to low-cost overnight rates."

Policy is also favorable. The automotive industry is a core sector in Europe, supporting about 13.8 million direct and indirect jobs, so the EU is treating the EV transition not only as climate policy but also as industrial policy to protect manufacturing and employment. In fact, the European Commission (EC) proposed an amendment in December last year that eased the planned full ban on internal combustion engine vehicle sales in 2035 by lowering the emissions reduction target from 100% to 90%. At the same time, it is tightening restrictions on the battery supply chain.

The key measure is the Industrial Acceleration Act (IAA), proposed in March. Under the IAA, only EVs that meet the 'Made in EU' requirement can receive public procurement, subsidies, and tax benefits. For automobiles, at least three core components, including battery cells, must be produced within the region, rising to five from 2030. In addition, the UK-EU Trade and Cooperation Agreement will impose a 10% tariff from 2027 on vehicles that do not meet the 65% local battery-cell content requirement. Both systems favor companies with cell plants in Europe.

■ Pressured K-Battery firms, with local production as the key to a rebound

Europe's EV market is already recovering. According to SNE Research, EV deliveries in Europe reached 1.988 million units in the first five months of this year, up 27.5% from a year earlier and accounting for 55.4% of the global market excluding China. During the same period, China fell 10.4% and North America declined 27.6%, suggesting that the growth center is shifting toward Europe and non-China Asia.

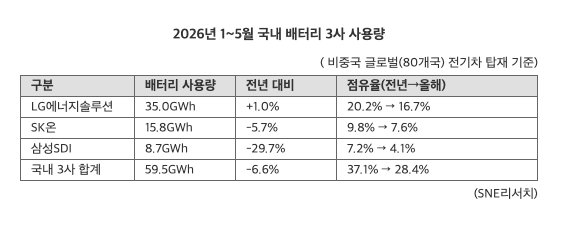

Domestic battery makers, however, remain under pressure. SNE Research said the market share of the three Korean battery makers in the non-China market fell 8.7 percentage points year on year to 28.4% in the January-May period. LG Energy Solution rose just 1.0% to 35.0 GWh, while SK On fell 5.7% to 15.8 GWh and Samsung SDI dropped 29.7% to 8.7 GWh.

Meanwhile, Chinese players such as CATL have rapidly expanded into non-China markets. In Europe, the market share of Korean battery makers, which reached 70% in 2020, has fallen to 35% in 2025 as low-cost Chinese products have expanded.

The key to a rebound lies in the local production requirements under the TCA and the IAA. Lee Yong-uk, a researcher at Hanwha Investment & Securities, said, "The UK's tougher TCA requirements and the EU's IAA announcement are a signal that discriminatory subsidies and tax benefits for Chinese products are being made concrete." He added, "In particular, if the IAA's detailed anti-China provisions are strongly specified, utilization rates at the three domestic battery makers, which remained in the 40% range in 2025, are expected to recover to 60% to 80% by 2028."

SK On is being mentioned as a likely beneficiary thanks to its European base and customer network. Its main client, Volkswagen Group, saw global EV sales excluding China rise 7.6% year on year to 517,000 units in the first five months of this year, ranking first and signaling a recovery. In particular, SK On's second plant in Komárom, Hungary, is reportedly running both cell and module production lines and maintaining utilization in the mid-80% range, which could bring forward the timing of a return to profitability.

An industry source said, "Europe is moving toward placing greater emphasis on local production and supply chain stability even in the EV market." The source added, "Domestic companies with production bases in Europe may benefit from policy changes and recovering demand."

eastcold@fnnews.com Kim Dong-chan Reporter