A Young Worker in His 20s Says He Cannot Save Money Even With a Side Job... How Can He Build a Lump Sum? [Q&A on Wealth Management]

- Input

- 2026-07-05 05:00:00

- Updated

- 2026-07-05 05:00:00

[Financial News] A man in his 20s, identified as A, works a full-time job and also takes on a part-time job when the opportunity arises. His monthly income has increased, but his savings have not grown as much as he expected, leaving him worried. During the week, he had little personal time, so he spent heavily on weekend dates with his girlfriend as a form of compensation. After recently breaking up, he applied for counseling, thinking he now needs to cut spending and save more in earnest. He currently saves on some living expenses because his company provides housing and lunch. He wants to know how he should increase the share of his money going into investments and savings.

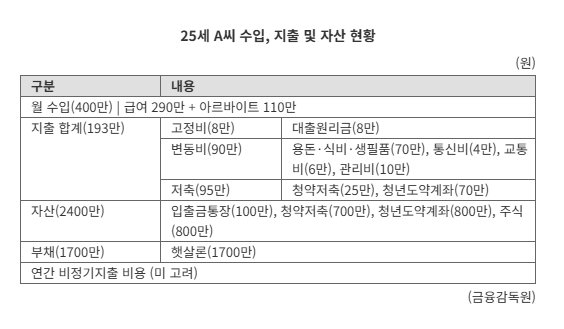

A's monthly income is 4 million won. He earns 2.9 million won from his job and 1.1 million won from his part-time work. His fixed expense is 80,000 won in principal and interest payments on a Sunshine Loan. His variable expenses total 900,000 won, including 700,000 won for pocket money, food and daily necessities, 40,000 won for telecom bills, 60,000 won for transportation, and 100,000 won for maintenance fees. He saves 950,000 won a month, including 250,000 won in a housing subscription savings account and 700,000 won in a Youth Leap Account. His assets total 24 million won, including 1 million won in a checking account, 7 million won in a housing subscription savings account, 8 million won in a Youth Leap Account, and 8 million won in stocks. He also has 17 million won in debt from a Sunshine Loan. He is not separately accounting for annual irregular expenses.

According to the Financial Supervisory Service on the 5th, for A, who earns additional income beyond his salary, it is advisable to keep spending within the limits of his existing income and direct the extra income into savings.

Before setting a savings goal, it is important to understand how much you spend. If you do not know how much you spend in a month or in a year, or how much you actually need, there is a high chance that you will end up withdrawing your savings to cover living expenses again. In that case, it becomes difficult to steadily build assets.

The first thing A should do is organize his expenses and set a spending budget. Expenses can be divided into monthly expenses and irregular expenses. Monthly expenses include fixed costs, food, pocket money and telecom bills. Irregular expenses include travel, shopping and congratulatory or condolence payments. A had been saving on housing and lunch through company support, but as weekend spending increased, he tended to spend most of his part-time income as well.

It would also help to split bank accounts and build the habit of using a debit card. One approach is to use the salary account only for automatic transfers of fixed expenses, while managing spending such as living costs, food and pocket money in a separate account. If he transfers only the budgeted amount into that account and uses a debit card, he can spend more deliberately.

The Financial Supervisory Service advised A to keep monthly variable expenses at around 900,000 won and set separate annual budgets of 1.5 million won for irregular expenses such as medical bills and congratulatory or condolence payments, and 2.1 million won for emergency funds. The annual budget for irregular expenses and emergency savings, totaling 3.6 million won, should be set aside monthly. Before that, he should repay the Sunshine Loan as early as possible after receiving his salary to reduce fixed expenses.

In that case, after subtracting 900,000 won in variable expenses and 300,000 won for irregular expenses and emergency savings from his monthly income of 4 million won, A could save 2.8 million won a month. If he maintains that pace, he could accumulate about 34 million won in one year and about 100 million won in three years.

The Financial Supervisory Service recommended that A continue contributing 700,000 won a month to the Youth Leap Account to benefit from tax exemptions and government matching contributions. It also advised reducing the housing subscription savings account, which is not very competitive, to 100,000 won a month and adding another 1.5 million won a month to installment savings to focus on building a lump sum. Investing should begin with spare funds and enough time. The agency suggested a strategy of investing 500,000 won a month in an Individual Savings Account (ISA) through regular installments.

A Financial Supervisory Service official said, "For young workers just starting out, the priority should be to build a lump sum first, while gaining investment experience and gradually improving their skills with a portion of their funds." The official added, "Even if the stock market has posted strong returns recently, you should keep in mind that it will not necessarily deliver high returns in the future."

You can receive free, customized financial consumer counseling by typing the Financial Supervisory Service's financial consumer portal, Fine, into an internet search box or by calling the Financial Supervisory Service Call Center 1332 (press 7 for financial advisory services).

nodelay@fnnews.com Park Ji-yeon Reporter