A Worker in His 30s Says He Made Money on Domestic and Overseas Stocks and ETFs, but Wants to Know How to Save on Taxes [Tax and Finance Q&A]

- Input

- 2026-06-28 05:00:00

- Updated

- 2026-06-28 05:00:00

[Financial News] A worker in his 30s, identified as Mr. A, recently began investing in large blue-chip stocks, U.S. tech stocks, and several exchange-traded funds (ETFs) as domestic and overseas stock markets have shown unprecedented momentum. He has made solid gains, but his concerns have also grown. After seeing profits worth tens of millions of won from overseas stock ETFs, he became worried about how much tax he might owe. He applied for a financial consultation to find out how taxes are applied to investment products and whether there are any ways to reduce them.

According to KB Securities on the 28th, taxes generated from stock trading are applied very differently depending on the market and the nature of the product, so beginner investors need to be especially careful.

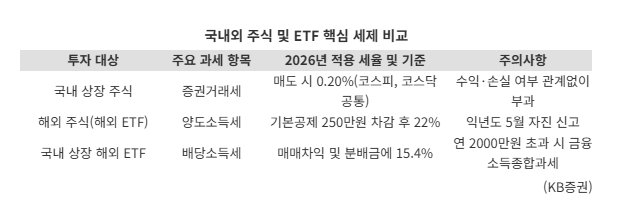

For Korean individual investors investing in overseas stocks, one key issue is the relationship between capital gains tax and exchange rates. For overseas stocks and overseas-listed ETFs, investors must file and pay capital gains tax of 22%, including local income tax, in May of the following year on net profits for the year after deducting the basic exemption of 2.5 million won.

Many investors mistakenly believe that if they do not convert dollar proceeds into won after selling, no foreign exchange gain is generated. But under tax law, capital gains are calculated by converting the acquisition and sale settlement amounts into won using the standard exchange rate on each respective date. In other words, regardless of whether the money is exchanged, taxable gains are calculated in won based on the exchange rate at the time of the transaction. As a result, exchange-rate fluctuations and taxes are closely linked.

It is also important to remember that capital gains tax on overseas stocks is imposed based on net profit after combining all realized gains and losses for the year. If one stock has produced a large gain, selling another stock with an unrealized loss in the same year can reduce net profit and the tax base through a strategy known as offsetting gains and losses. However, losses cannot be carried forward to offset gains in the following year.

Go-un Lee, a tax advisory committee member at KB Securities, advised, "When trading domestic-listed overseas equity ETFs, investors should be careful about tax traps."

If you buy ETFs directly in the U.S. market, they are taxed at 22% as capital gains tax, which is separate taxation. By contrast, trading gains from domestic-listed overseas ETFs are classified as dividend income and taxed at 15.4%.

At first glance, the 15.4% dividend income tax rate may look more favorable than the 22% capital gains tax applied to direct overseas investment. However, if the combined amount of trading gains and distributions exceeds 20 million won a year, the investor may become subject to comprehensive financial income taxation. In that case, the income is combined with salary or business income, and a steep progressive tax rate of up to 49.5% may apply, increasing the burden. This is why asset diversification is essential for high-net-worth investors.

For ordinary individual investors, trading gains from buying and selling listed domestic stocks are tax-free unless they are major shareholders. Domestic stocks are subject only to securities transaction tax, with a rate of 0.2% applied on sales in both the KOSPI and KOSDAQ markets. The current threshold for major shareholders of listed domestic stocks is a market value of 5 billion won per stock. Even if a stock price surges during the year and exceeds 5 billion won, the investor is excluded from major shareholder taxation as long as the threshold is not exceeded at the final point on the last day of the previous fiscal year.

Meanwhile, starting this year, the tax-free scope for capital reduction dividends funded by capital reserves has been reduced, creating new taxable cases. This means that major shareholders of listed companies and some investors in unlisted shares will be taxed on the portion exceeding the acquisition cost as dividend income. Ordinary retail investors in listed stocks will continue to receive the same tax-free treatment for capital reduction dividends as before.

A separate taxation system for dividend income from high-dividend listed companies has also been introduced. It applies to cash dividends from listed companies with a dividend payout ratio of at least 40%, or at least 25% if they increased dividends by more than 10% from the previous year. Even taxpayers subject to comprehensive financial income taxation may choose separate taxation for dividend income from high-dividend companies instead of including it in comprehensive taxation, which can reduce the burden. However, the measure is temporary and will apply only through 2028.

KB Securities recommended using an Individual Savings Account (ISA) to cope with the complex tax environment. If investors place domestic-listed overseas ETFs or high-dividend stocks in an ISA account instead of a regular account, they can benefit from tax exemption and separate taxation.

The committee member stressed, "At a time like this, it is more important than ever to clearly understand the tax status of the products you invest in and to build a smart portfolio that strategically uses tax-saving tools."

nodelay@fnnews.com Park Ji-yeon Reporter