[Editorial] Urgent Improvements Needed for the Volatility-Boosting Samsung Electronics and SK Hynix 2x Leveraged ETF

- Input

- 2026-06-24 18:22:44

- Updated

- 2026-06-24 18:22:44

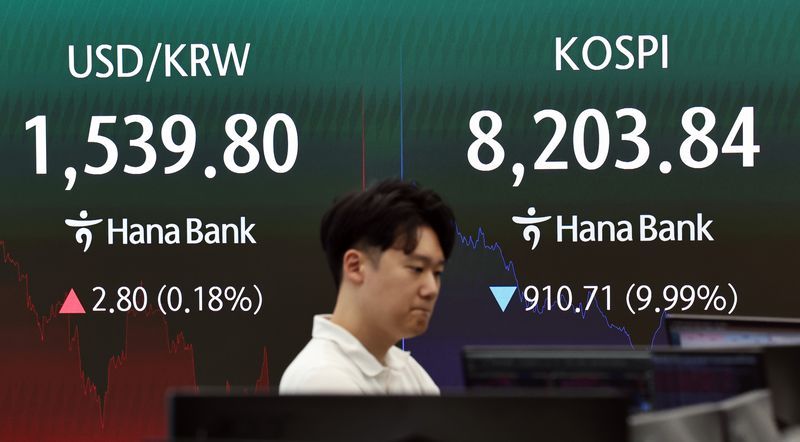

On the 23rd, the KOSPI fell by nearly 10 percent, marking its largest-ever drop. The two single-stock leveraged ETFs, introduced a month ago, plunged by an average of 25 percent, far exceeding the market's decline. This is only one example. Since the products were launched, investors caught in the trap of the so-called negative compounding effect have seen losses snowball as the market repeatedly rose and fell. Critics also say that concentrating leverage on two stocks that account for a large share of KOSPI market capitalization is amplifying market volatility.

Lee Chan-jin, Governor of the Financial Supervisory Service, said, "I regret not having stopped it more forcefully." It is unusual for the head of the financial authorities to publicly acknowledge the possibility of policy failure. Hwang Sung-yeob, chairman of the Korea Financial Investment Association, also expressed concern, saying, "I am worried because losses could grow larger."

The issue is drawing attention overseas as well. Bloomberg News and Nikkei, Inc. recently reported that the sharp declines in U.S. and European markets were affected by shocks originating from South Korea. They said the situation worsened as selling pressure tied to the Samsung Electronics and SK hynix leveraged ETFs added to the downturn. Nomura Securities also warned that "the structural dynamics surrounding leveraged ETFs are amplifying volatility" and that they "could trigger a butterfly effect that reaches the other side of the globe."

The product was introduced last month to broaden investor choice and absorb demand that might otherwise flow overseas into the domestic market. It allows investors to gain leveraged exposure with relatively little capital and can also help improve market liquidity. It also aligns with global trends, as similar products are already available in major markets such as the United States and Japan.

But now that the side effects have become reality, it is urgent to come up with corrective measures. It will not be easy to remove a product that has already been introduced, but that does not mean authorities can simply stand by. If the head of the financial authorities is publicly speaking of "regret" and "reflection," then every possible measure should be considered. First, the launch of similar ultra-high-risk products should be approached with caution. An eagerness to boost market activity must not obscure the risks of speculative financial products.

To protect investors, it is necessary to tighten deposit requirements, reduce credit limits, and consider raising margin ratios. When excessive leverage is combined with borrowed investment, market instability can worsen further. Investor eligibility standards should also be raised, including by extending the current two-hour mandatory pre-investment education, and oversight of securities firms' improper sales practices must be strengthened. It is late, but authorities should now move quickly to minimize market distortions and investor losses.