The Paradox of Multi-Homeowners With Net Assets of 1 Billion Won: Weaker Debt-Repayment Capacity Than Homeowners Without a House

- Input

- 2026-06-24 18:12:14

- Updated

- 2026-06-24 18:12:14

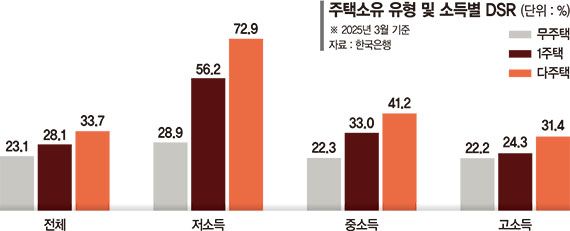

The reason is that most of their assets are concentrated in real estate, leaving them with excessive debt relative to income. The Bank of Korea said they are vulnerable to market interest rate changes and housing price fluctuations, making preemptive soundness management necessary. 7% as of March last year. 1%.

4% for households without a home. This means that while their debt burden looks manageable relative to assets, their repayment capacity is weaker than that of households without a home when measured against income. 4% recorded for high-income households. Deterioration in the soundness of borrowers owning three or more homes was also confirmed in the numbers.

52% for two-home owners. Because multi-home households hold a large share of their portfolios in real estate, their ability to cope with debt through financial assets was relatively limited. 007 billion won, about seven times the 145 million won held by households without a home. 55 times for households without a home, a gap of nearly threefold.

A Bank of Korea official said, "Single-home households that own a home for residence should maintain access to loans within their repayment capacity. Multi-home households, which are heavily affected by market interest rate and housing price changes, need stronger preemptive soundness management and an orderly reduction in housing sales. Households without a home are facing higher housing costs due to rising rent and jeonse prices in the Capital Region, so policy support for vulnerable groups is needed.

" The Bank of Korea also examined potential risks in the domestic commercial real estate market. Transaction volume for commercial properties such as retail stores, offices, and warehouses has been on a downward trend since peaking in 2021, and reached 36,000 deals in the first quarter of this year, below the long-term average of 59,000. Vacancy is another problem, and conditions are more serious in Non-metropolitan areas.

5% recorded in the Capital Region.

4% for households without a home. This means that while their debt burden looks manageable relative to assets, their repayment capacity is weaker than that of households without a home when measured against income. 4% recorded for high-income households. Deterioration in the soundness of borrowers owning three or more homes was also confirmed in the numbers.

taeil0808@fnnews.com Kim Tae-il Reporter