SME Non-Performing Loans Triple Those of Large Companies, So Banks Chose to Sell Them [Bank of Korea's First-Half Financial Stability Report]

- Input

- 2026-06-24 11:28:51

- Updated

- 2026-06-24 11:28:51

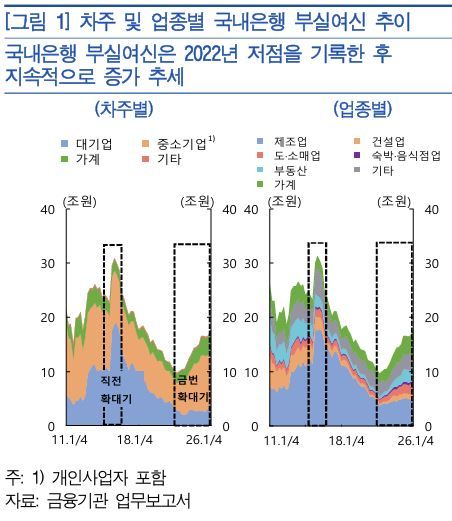

According to the '2026 First-Half Financial Stability Report' published by the Bank of Korea on the 24th, the amount of non-performing loans held by SMEs stood at 10.5 trillion won as of the first quarter. That is nearly three times the 3.6 trillion won recorded for large companies.

During the previous expansion phase in 2015 and 2016, bad loans rose mainly among large companies as vulnerable industries such as shipbuilding and shipping, including Daewoo Shipbuilding & Marine Engineering, saw a deterioration in debt repayment capacity and entered full-scale restructuring. Since 2022, however, SMEs have taken that place.

In fact, the share of bad loans held by large companies was 60.4% in the first quarter of 2016, but it fell to 20.5% in the first quarter of this year, or about one-third of its previous level. By contrast, the SME share rose from 32.2% to 58.9%. The delayed recovery in service sectors such as wholesale and retail and real estate appears to be spreading across industries as a whole.

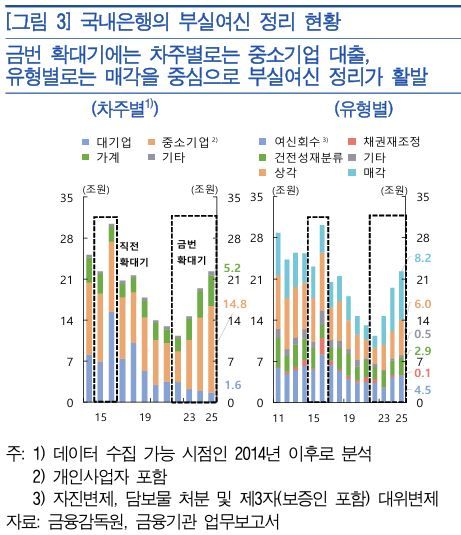

A Bank of Korea official explained, "In the previous expansion phase, the scale of claim restructuring increased during creditor-led corporate normalization processes, and self-resolution through write-offs and loan recovery was significant." The official added, "In this expansion phase, the scale of resolution through sales is larger."

Last year, the amount resolved through sales reached 8.2 trillion won, or 36.7% of the total. That was ahead of loan recovery, at 20.4% or 4.5 trillion won, and write-offs, at 27.1% or 6 trillion won. Since recovery and write-offs require more time and effort, the result suggests that sales are seen as more favorable in terms of management burden.

The Bank of Korea official noted, "As bad loans have expanded mainly in SME lending, where the share of collateralized loans is high, banks have preferred bulk sales rather than write-offs, which are mainly used to dispose of unsecured bad debts." The official added that the volume is being absorbed by Non-Performing Loan (NPL) Specialized Investment Firms, which can raise large amounts of capital and endure long investment and recovery cycles.

By borrower type, the notable trend in sold bad loans is the increase in individual borrowers. In 2015, corporate borrowers, including small and medium-sized corporations, accounted for 77.2% of bad loan sales, largely due to the restructuring of large companies. In 2025, however, individual borrowers such as sole proprietors made up 41.5%, driven by weak domestic demand and higher lending rates. That marks a sharp increase from 22.8% ten years earlier.

taeil0808@fnnews.com Kim Tae-il Reporter