Rising Funding Costs, Frozen Fees Deepen Woes for Credit Card Companies [The Two Faces of Rising Interest Rates (4)]

- Input

- 2026-06-15 18:12:11

- Updated

- 2026-06-15 18:12:11

■ Funding costs move with interest rates

According to the financial sector on the 15th, recent inflationary pressure and growing caution over monetary policy have strengthened market expectations that the benchmark rate could be raised.

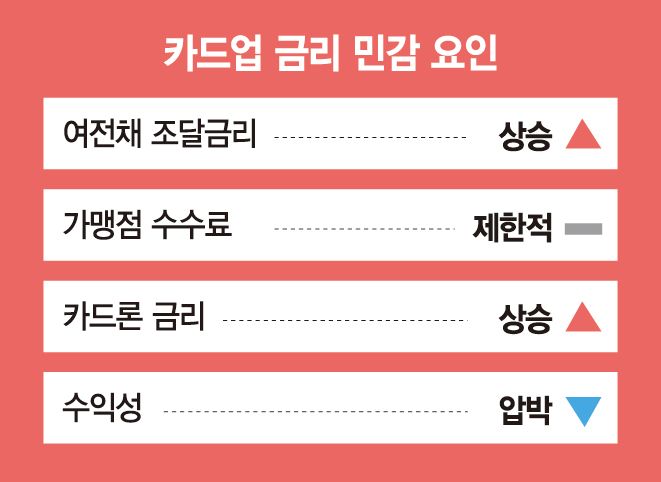

The main funding method for credit card companies is issuing Specialized credit finance company bonds. These bonds are a way for card issuers to borrow money by paying investors a set interest rate, and they are directly affected by market rate movements. The yield on unsecured, AA+-rated, three-year Specialized credit finance company bonds has moved from the mid-3% range earlier this year to the mid-4% range recently.

As rates rise, credit card companies face two burdens at once. They must pay higher rates when issuing new bonds, and they must refinance maturing debt that was raised at lower rates in the past at more expensive levels. If the credit spread over Korean Treasury Bonds widens, the added credit premium can further increase pressure on funding costs.

Merchant fees are difficult to adjust quickly because of regulations and contract structures. Costs change rapidly with market rates, but revenues cannot keep pace. An industry official said, "Funding rates reflect market conditions quickly, but merchant fees are structurally limited in how much they can be adjusted," adding, "In a rising-rate environment, higher cost burdens are unavoidable."

■ Card Loan risks are expanding

Credit card companies are supplementing their revenue base through lending assets such as Card Loan and cash advance products. Card Loan is one of their key revenue sources, as it involves lending money based on a borrower's creditworthiness and earning interest in return.

However, in a rising-rate environment, Card Loan can also become a burden. As higher funding costs are partly passed on to Card Loan rates, borrowers face heavier interest payments, which could weaken repayment capacity and lead to higher delinquency rates.

In fact, Card Loan rates have been showing a gradual upward trend. Among eight dedicated card issuers — Lotte Card Co., Ltd., BC Card, Samsung Card, Shinhan Card, Woori Card, Hana Card, Hyundai Card and KB Kookmin Card — Card Loan rates rose from the 13.3% range in February to the 13.4% range in March and the 13.5% range in April. With financial authorities maintaining their stance on household debt management, it is also difficult for card issuers to aggressively expand lending assets.

Industry watchers say the renewed focus on the credit card business reflects once again how sensitive it is to interest-rate changes. A financial sector official said, "The credit card business is structured so that higher rates directly translate into higher funding costs," adding, "Because it is difficult to fully offset that through revenue, earnings volatility could widen depending on the interest-rate environment."

imne@fnnews.com Hong Ye-ji Reporter