"I Bought on Margin and Lost 30% in Samsung Electronics and SK hynix. What Should I Do?"... What Return Is Needed to Recover Principal [In Chi-beom's Stock Investment Boot Camp]

- Input

- 2026-06-13 09:00:00

- Updated

- 2026-06-13 09:00:00

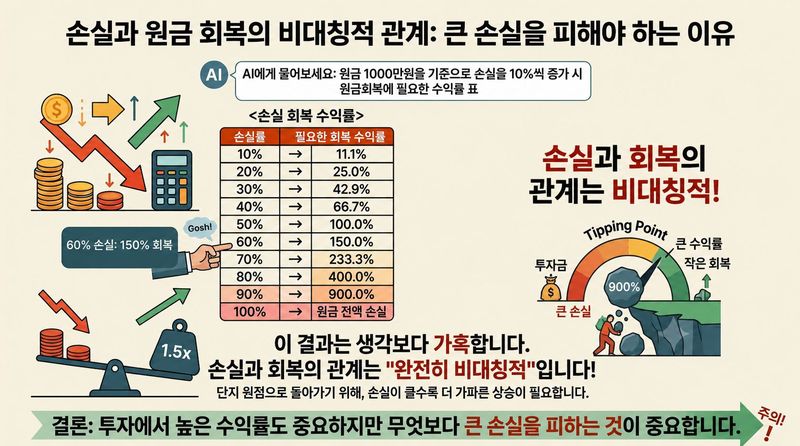

[Financial News]"This will probably be remembered as the first time I managed to protect something." Hot Stove League (2019, Episode 16, line by Baek Seung-soo, played by Namkoong Min)That line is from the final episode of the baseball drama Hot Stove League (2019), spoken by Baek Seung-soo, played by Namkoong Min. What is it that investors in their 20s must protect in the stock market? Is it a high win rate? A big profit? Or avoiding losses? This time, let’s look at what young individual investors must protect when investing. Before that, here is a quick quiz.If an investor suffers a 30% loss on principal, what return is needed to recover the original amount?An investor who started with 10 million won lost 3 million won after a 30% decline. "If I lose 30%, do I just need a 30% gain to get back to even?" No. A 30% gain on the reduced 7 million won would bring the account to 9.1 million won (= 7 million won × 1.3), so a much larger return is needed. To return to the original 10 million won, the investor must earn exactly 42.86%.

The relationship between loss and recovery is asymmetric

Ask AI: "Using 10 million won as the starting principal, please make a table showing the return needed to recover principal as the loss rate increases by 10% increments." The result looks harsher than expected. If the loss is 60%, a 150% return is needed. At 70%, the required return rises to 233%. At 80%, it jumps to 400%. And if the loss reaches 90%, an astonishing 900% return is needed just to get back to where you started. What is striking is that this is not the return needed to make money, but only the return needed to return to zero.This reveals an important fact. The relationship between loss and recovery is not symmetrical. It is asymmetric. In other words, the larger the loss, the steeper the return required to recover principal. This is why, in investing, avoiding large losses matters even more than chasing high returns.

A high win rate does not necessarily mean high returns

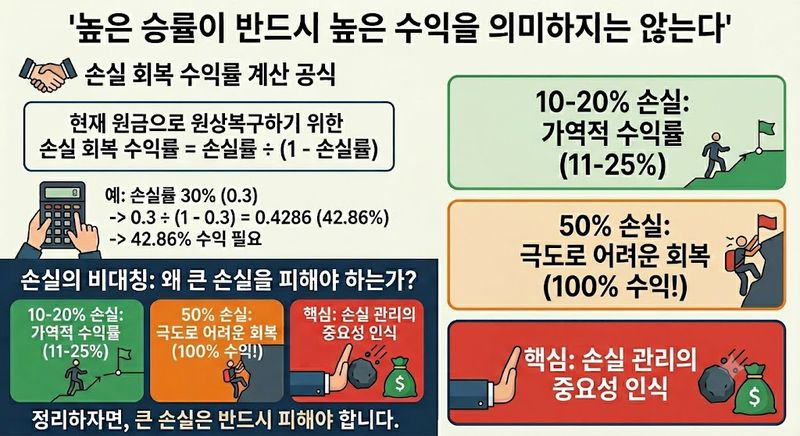

Would you like to calculate the "loss-recovery return" needed to bring your current loss rate back to principal? Here is a simple formula. Loss-recovery return needed to restore principal = loss rate ÷ (1 - loss rate). For example, if the loss rate is 30% (0.3), then 0.3 ÷ (1 - 0.3) = 0.4286, meaning a 42.86% gain is required to recover principal.In short, when losses are around 10% to 20%, recovery is still possible with reversible returns of about 11% to 25%. But once losses exceed 50%, recovery becomes extremely difficult because returns of more than 100% are required. I hope this helps explain why recognizing the asymmetry of losses is so important, and why loss management matters. Let me emphasize once again: large losses must be avoided.

Now that we understand the asymmetry of losses, is reducing losses enough? Beginner investors often fall into another trap here: obsession with win rate. They believe that a high win rate guarantees high returns. Do you remember the "Disposition Effect" I mentioned before? The tendency to sell too quickly when prices rise and to hold on until the end when they fall is called the Disposition Effect. Because of this psychological bias toward avoiding losses, inexperienced investors often sell as soon as they make even a small profit. They want to lock in a win quickly.

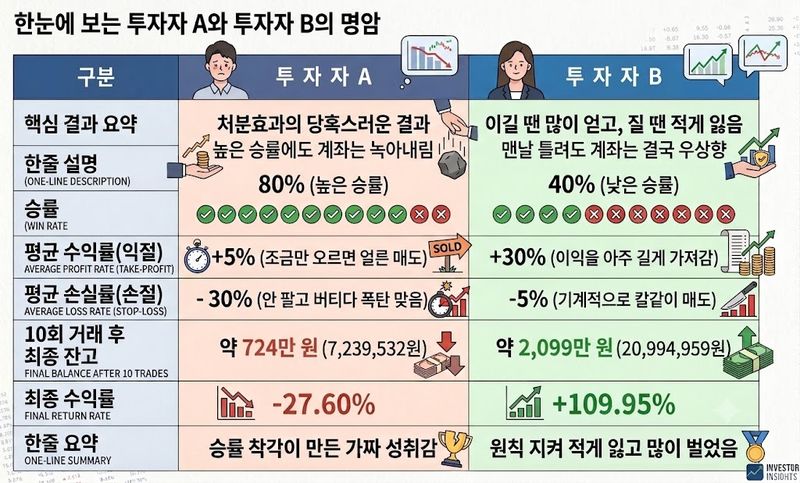

An investor with a high win rate who still loses money

What happens to an investor with an 80% win rate trapped in the Disposition Effect?Here is an example. Investor A, trapped in the Disposition Effect, has an 80% win rate. Once a gain is secured, returns do not matter. If a trade makes 5% profit, A sells immediately. On the other hand, when a trade goes into the red, A becomes an involuntary long-term investor and just holds on. As a result, the loss rate reaches -30% (assumed). Let’s assume 10 trades. First, let’s calculate the multiplier applied to the account each time. When A wins, the account grows by 5%, so principal (1) + profit (0.05) = 1.05 times the original amount. When A loses, 30% is lost, so principal (1) - loss (0.3) = 0.7 times the original amount.In other words, after Investor A’s 10 trades, the account ends up as 10 million won multiplied by 1.05 eight times and 0.7 twice. To make it easier to understand, let’s assume the eight wins came first and the two losses came afterward. The order does not matter because multiplication gives the same result either way.

In formula form, it is 10 million won × 1.058 (8 wins) × 0.72 (2 losses). Calculated as 10 million won × 1.47745544 × 0.49,the final balance is about 7.24 million won (7,239,532 won), a loss of -27.60% from the original principal. Of course, real investors do not always have such an extreme profit-and-loss structure, but this example shows that win rate alone cannot determine investment performance.

An investor who benefits despite frequent losses

What happens with a low 40% win rate and frequent losses? On the other hand, you can still win even with a low win rate.Investor B has a poor win rate: 40%. But B tends to take a lot when winning. In winning trades, B takes +30% (assumed). B also has a personal stop-loss rule and sells immediately if the price falls 5%. In other words, B is a savvy trader. Again, let’s assume 10 trades.First, let’s calculate the multiplier applied to the account each time. In formula form, it is 10 million won × 1.34 (4 wins) × 0.956 (6 losses). Calculated as 10 million won × 2.8561 × 0.7350919, the final balance is about 20.99 million won (20,994,959 won), or a 109.95% gain. This is also just a setup for understanding, not advice that any one case is always right or a recommendation of specific numbers.

Use mechanical stop-losses as your shield whenever you lose

This is why even an investor with an 80% win rate can fail in the stock market. Sometimes I see young investors who are too obsessed with win rate. The win rate in stocks is a little different from the win rate in sports like boxing. In boxing, a decision win and a knockout win both count as one victory. The stock market is different. So what should you do from now on? It is simple. In trades where you are winning, take as much profit as possible. In trades where you are losing, cut losses mechanically according to your preset stop-loss rule.If a company or stock is not one that can take a "calculated risk" through thorough research and continuous analysis, then use mechanical stop-losses as your shield every time you lose. And it would be good to steady your mind with the thought that this habit is ultimately the first step toward victory. Losses endured under your own stop-loss rules help you overcome psychological biases such as loss aversion and the disposition effect. And when you win, think about what your own method is for letting profits run.

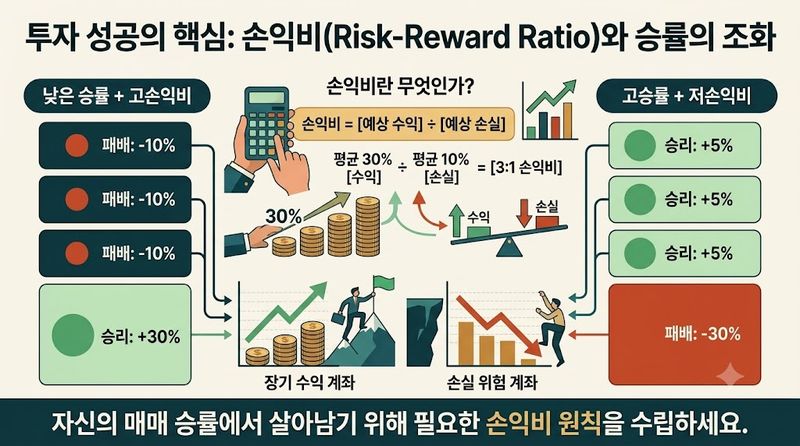

Understanding the asymmetry of losses and win rates, and setting a risk-reward ratio that fits your own win rate. In one sentence, everything explained so far comes down to the risk-reward ratio.The risk-reward ratio refers to "the ratio between the expected profit and the expected loss from a single investment." For example, if an investor makes an average of 30% and loses an average of 10%, the risk-reward ratio (profit:loss) is 3:1.As we saw earlier,even with a low win rate, a good risk-reward ratio can generate profits over the long term.Conversely, even with a high win rate, a poor risk-reward ratio can still lead to losses. I recommend that each of you calculate, "What risk-reward ratio do I need to survive with my current trading win rate?"

What young individual investors must protect is their own money, that is, their investment principal. The most important thing in investing is not making huge profits, but surviving in the market for a long time. If you understand the asymmetry of losses, move beyond the illusion of win rate, and stick to your own risk-reward principles, your investing can gradually move from survival to growth.

[About the Author]

Executive Director In Chi-beom worked for 30 years in corporate communications, consistently handling PR, IR, ESG, and CSR across finance at Samsung Life Insurance, IT at AhnLab, Inc., Hancom, and SK Communications, and retail at Samsung Tesco. He is currently focused on writing books about investing and corporate communications at KPI Investment Advisory. He believes that successful stock investing begins with automating the right habits for handling money.

ksh@fnnews.com Kim Seong-hwan Reporter