Is It Okay to Invest 2 Million Won Out of a 2.7 Million Won Salary? [Personal Finance Q&A]

- Input

- 2026-06-07 07:00:00

- Updated

- 2026-06-07 07:00:00

[Financial News] A man in his 20s who has been working for just four months says he puts 2 million won into his securities account as soon as he gets paid. He believes now is the time to save money while he can still rely on his parents' support. He currently lives at home and commutes to work in his parents' car. His goal is to build up a lump sum quickly and move out to a place near his office. However, because most of his salary goes into investments, he sometimes falls short on living expenses. He sought financial advice to find out whether he can keep saving and investing this way, and how much he should be setting aside.

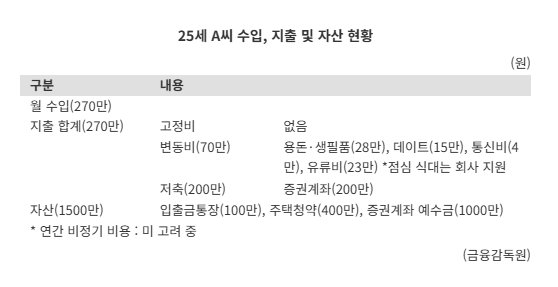

The 25-year-old man earns 2.7 million won a month. He has no irregular annual income. His monthly spending also totals 2.7 million won. He has no fixed expenses. Variable expenses amount to 700,000 won, including 280,000 won for allowance and daily necessities, 250,000 won for dating, 40,000 won for mobile service, and 230,000 won for fuel. Lunch is covered by his company. He saves 2 million won a month in his securities account. He has not yet calculated his irregular annual expenses. His assets total 15 million won, including 1 million won in a deposit and withdrawal account, 4 million won in a housing subscription account, and 10 million won in cash held in his securities account.

According to the Financial Supervisory Service (FSS) on the 7th, young workers should first understand their spending structure accurately before focusing on investing. The agency added that they must also account for irregular expenses, not just monthly spending, in order to calculate how much they can realistically save.

The first step is to break down monthly expenses. Fixed costs that are essential for working life include housing, mobile service, transportation, and lunch. In this case, the man uses his parents' car, pays no housing costs, and receives lunch support, so his burden is relatively light. Controllable spending categories include allowance, daily necessities, and exercise costs, and the FSS said his current spending level is appropriate.

Irregular expenses should be managed by setting an annual budget from the start. Travel, clothing and beauty expenses, and congratulatory or condolence payments are not paid every month, but they can add up to a large amount over a year. Without advance planning, spending can become excessive, forcing a person to withdraw savings and ultimately eroding total assets.

The FSS suggested setting the man's annual irregular-expense budget at 4.1 million won and managing it by setting aside 350,000 won a month in a separate account.

It also recommended dividing accounts by purpose. A salary account should be used for automatic transfers to cover essential fixed expenses such as transportation and mobile service. Living expenses, allowance, and dating budgets should be moved to a separate account and controlled with a check card. A dedicated account for irregular expenses should also be created, with 350,000 won deposited each month.

Once monthly spending is organized, it becomes possible to calculate how much can be saved each month. In this case, the man's monthly income of 2.7 million won minus 700,000 won in monthly expenses and 350,000 won in monthly irregular-expense savings leaves 1.65 million won.

However, the advice was that putting all of his money into investments should be adjusted. Young workers often do not yet have enough investment experience or knowledge, so concentrating all funds in investments can be risky.

An FSS official said, "Rather than pursuing returns through short-term trading, it is important to build investment experience from a long-term perspective," adding, "A steady asset-building strategy is needed, using youth-focused policy financial products and an Individual Savings Account (ISA)."

The FSS recommended allocating the 1.65 million won in monthly savings as follows: 500,000 won to a Youth Future Savings Account, 650,000 won to a regular savings account, and 500,000 won to an ISA.

It also advised delaying moving out and buying a car for as long as possible. Living independently could add about 1 million won a month in rent, maintenance fees, and food costs, while buying a car would also bring a heavy burden from insurance, taxes, and upkeep.

An FSS official said, "The early years of working life are a time to lay the foundation for asset building," and added, "It is worth setting a goal of saving 20 million won a year while systematically managing monthly and irregular expenses, and planning to build 100 million won in seed money over five years in the long term."

You can receive free personalized financial counseling by searching for the FINE financial consumer portal in an internet search engine or by calling the Financial Supervisory Service Call Center 1332 and selecting option 7 for financial advisory services.

[email protected] Park Ji-yeon Reporter