Low-income households turn to lenders outside banks as emergency cash source... Card loans near 43 trillion won [The Paradox of Mortgage Loan Regulations (2)]

- Input

- 2026-06-01 18:12:31

- Updated

- 2026-06-01 18:12:31

■ Card loans keep rising this year... close to 43 trillion won

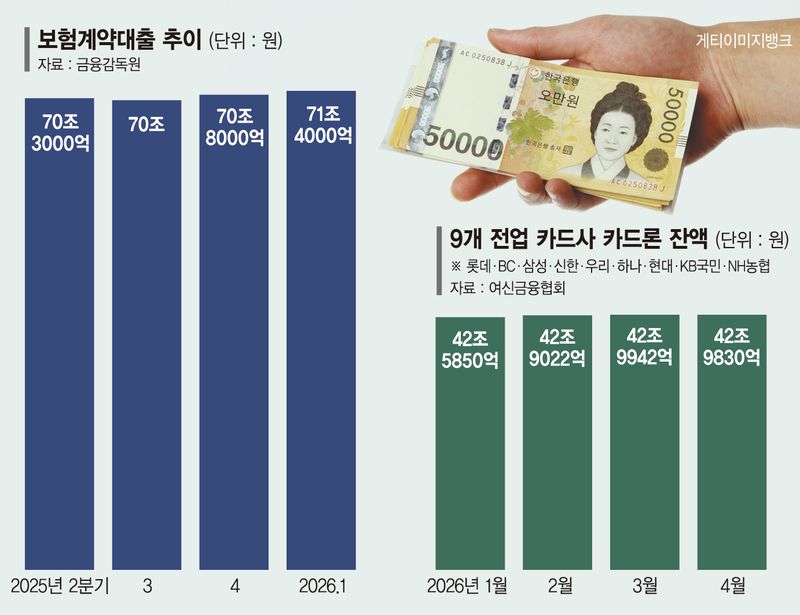

According to the Credit finance industry on the 1st, the outstanding balance of card loans at nine specialized credit card companies stood at 42.983 trillion won at the end of April. Card loans had been on a downward trend after the household debt measures announced in June last year, falling to 41.8375 trillion won at the end of September under the impact of DSR regulations and household lending volume controls.

The mood changed in the first quarter of this year. The balance rose to 42.585 trillion won at the end of January, 42.9022 trillion won at the end of February, and 42.9942 trillion won at the end of March.

The rise in card loans eased somewhat in April, but the quality of debt appears to be deteriorating. The outstanding balance of card loan refinancing loans increased 15.7% from 1.3817 trillion won at the end of last year to 1.5983 trillion won at the end of April this year. By contrast, total card loan balances rose just 1.5% over the same period. That suggests demand for refinancing, aimed at lowering or postponing repayment burdens on existing loans, is growing faster than overall card loan demand. In addition, the revolving balance for payment deferrals, which allows cardholders to postpone bill payments, rose by 34 billion won from the previous month to 6.7065 trillion won in April.

The sharp increase in mid-rate loans offered by card companies also shows the spillover effect of bank lending restrictions. In the first quarter, private mid-rate loan supply by eight specialized credit card companies reached 2.5708 trillion won, up 61.4% from 1.5928 trillion won a year earlier. It was the first time that private mid-rate loan supply by card companies exceeded 2 trillion won.

Both volume caps and regulatory incentives are driving card companies to expand mid-rate lending. Financial authorities are keeping the annual growth rate of card companies' household lending balances at around 1% to 1.5% compared with the end of the previous year. However, to encourage funding for borrowers with mid- to low-credit scores, the FSC excludes 20% of mid-rate loans extended by card companies from household lending volume management.

A financial industry official said, "After bank lending regulations were tightened, some mid- to high-tier borrowers who previously borrowed from first-tier banks have flowed into card loans, which is also increasing the amount classified as mid-rate loans." The official added, "As bank lending is being tightened, borrowers are moving toward card company mid-rate loans and card loans."

■ Policyholder loans rise by 110 billion won

Demand for emergency cash outside banks is also evident in the insurance sector. According to the FSS, household lending balances at insurance companies stood at 134.5 trillion won at the end of the first quarter, up 500 billion won from the previous quarter. Of that increase, policyholder loans, which allow borrowers to take out money against their insurance policies, rose by 600 billion won. In other words, the increase in household lending at insurers came from policyholder loans.

Looking at the period since the household debt measures announced in June last year, household lending at insurers rose only 100 billion won, from 134.4 trillion won at the end of June last year to 134.5 trillion won at the end of March this year. Over the same period, policyholder loans increased by 1.1 trillion won, from 70.3 trillion won to 71.4 trillion won. Policyholder loans let customers borrow within the amount of the surrender value of their insurance policies. Because they require little in the way of separate credit checks or loan screening, they are easy for borrowers with limited income documentation or urgent cash needs to use.

In response, insurers are raising the bar by lowering policyholder loan limits and taking other steps. Samsung Fire & Marine Insurance has decided to suspend policyholder loans for some health insurance products starting next month.

If the effect of household lending regulations is not a reduction in borrowing demand but a shift to loans outside banks, the risks tied to household debt could grow even larger. A financial industry official said, "When bank lending volume is tightened, borrowers in need of funds move to card loans, mid-rate loans, revolving credit, and policyholder loans." The official added, "With the real economy still sluggish, these loans could increase repayment burdens for borrowers, which is worrying."

[email protected] Reporter Ye Byeong-jeong Reporter