When banks tightened lending, borrowers turned to more expensive debt... Non-bank household loans jump by KRW 13 trillion [The Paradox of Mortgage Regulations (1)]

- Input

- 2026-05-31 18:16:19

- Updated

- 2026-05-31 18:16:19

■ Banks shrink, non-banks expand

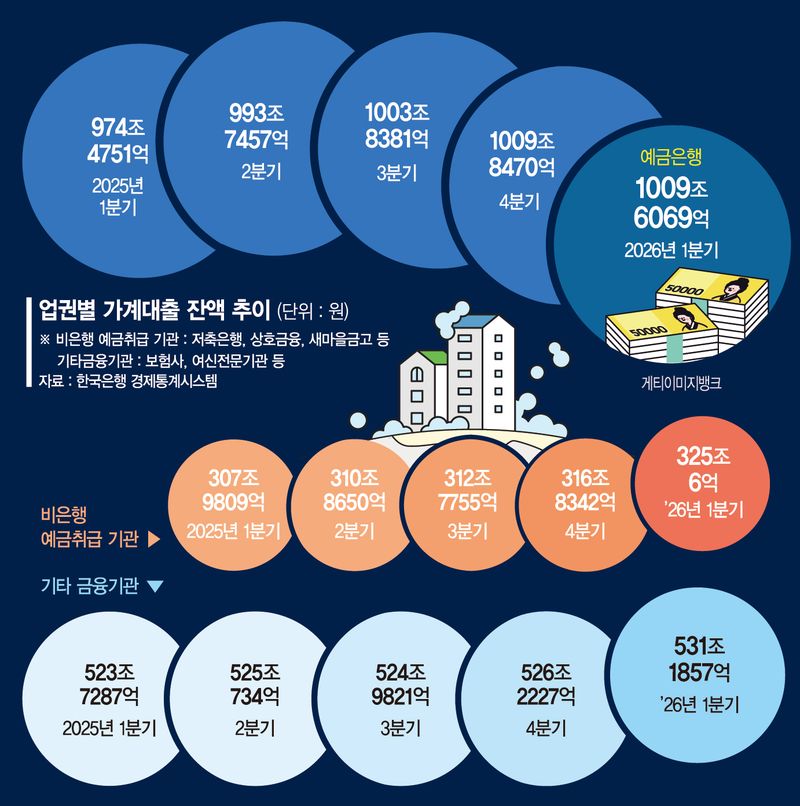

According to the Bank of Korea Economic Statistics System on the 31st, household credit outstanding stood at KRW 1,993.11 trillion in the first quarter of this year, up by about KRW 14 trillion from the previous quarter's KRW 1,979.088 trillion. Household credit is a broad measure of household debt that combines household loan balances and sales credit such as card spending. Over the same period, household loan balances rose by KRW 12.8893 trillion from the previous quarter to KRW 1,865.7932 trillion, while sales credit increased by KRW 1.1322 trillion to KRW 127.3177 trillion.

The increase in household lending was led by non-bank lenders. Household loans at deposit banks fell by KRW 240.1 billion from the previous quarter to KRW 1,009.6069 trillion. After rising for 12 straight quarters since the first quarter of 2023, household loan balances at deposit banks turned downward as lending regulations took effect. By contrast, household loans at non-bank deposit-taking institutions, including savings banks, mutual finance cooperatives and the Korean Federation of Community Credit Cooperatives, rose by about KRW 8 trillion from the previous quarter to KRW 325 trillion. Household lending at other financial institutions, including insurance companies and specialized credit finance companies, also increased by about KRW 5 trillion.

The shift toward non-bank lenders was especially clear in other loans, including credit loans and overdrafts. In the first quarter, total other loans rose by KRW 4.8372 trillion from the previous quarter to KRW 687.162 trillion. While other loans at deposit banks fell by KRW 57.74 billion over three months, other loans at other financial institutions increased by about KRW 7.9 trillion. In effect, funding demand blocked at banks moved to credit card companies, insurance companies and other financial institutions.

■ Debt remains, but moves to higher rates

Even within the banking sector, some say household debt management should not focus only on total volume. They argue that even if household lending growth at banks is kept under control, borrowers' interest burdens and delinquency risks can rise as funding demand shifts to non-bank lenders.

A financial industry official said, "It is hard to say household debt management has been successful just because household lending growth at banks has slowed." The official added, "If borrowers have moved to secondary financial institutions or other financial institutions, the overall household debt risk can build up in a different form."

The official continued, "As upward pressure on interest rates grows, borrowers pushed out of banks may end up using loans with relatively higher rates, which could further increase financial costs for vulnerable borrowers in the future." The point is that even if the size of household debt is the same, the interest burden and repayment structure facing borrowers can deteriorate, lowering the quality of debt.

Bank loans generally carry lower interest rates and have a higher share of long-term, installment repayment structures, while non-bank loans tend to have a larger share of short-term, high-interest products. If an economic slowdown or falling income is added to the mix, soundness risks could grow, especially among vulnerable borrowers.

The problem is that tighter household lending rules have not eliminated borrowers' funding needs. Another financial industry official said, "Demand for home purchases will not disappear in the short term just because of household lending regulations." The official added, "Borrowers who cannot get loans from first-tier banks may move to second-tier lenders, insurance companies, capital firms or card loans, and this balloon effect could become even larger going forward." The official also warned that if the share of high-interest loans rises in the process, it could lead not only to higher delinquency rates but also to greater pressure on household finances.

[email protected] Lee Hyun-jung Reporter