"Won 3 million? Even the unemployed are fine... All you need is one family contact". When I clicked the quick-cash ad, hell broke loose [Recorder of the Low Places]

- Input

- 2026-05-31 06:00:00

- Updated

- 2026-05-31 06:00:00

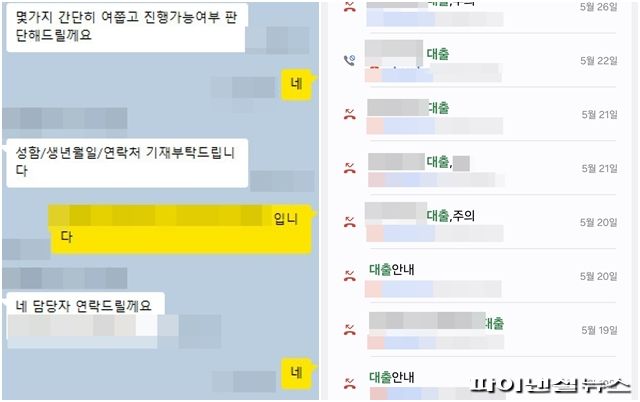

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

\r\n People struggling to pay for living expenses, hospital bills, and credit card debt look for another path outside the formal financial system. At that crossroads, there are also illegal loans that appear to be nothing more than a 'simple consultation.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.' In [Recorder of the Low Places], we examined how personal information becomes collateral even before money is borrowed, and looked into the pain of victims through actual private-loan and illegal lending consultations.

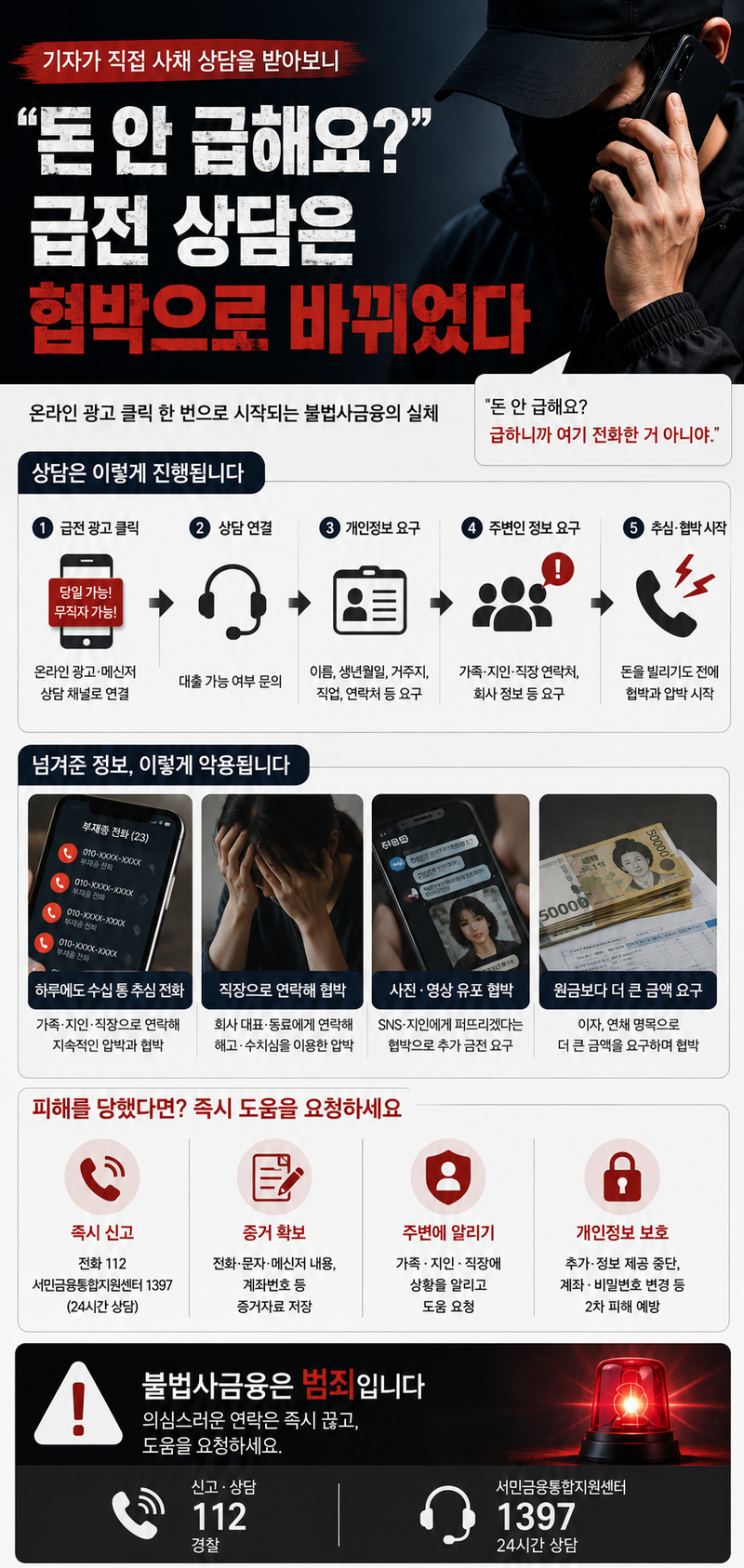

Clicking a quick-cash ad leads straight to a consultation channel Search portals and social media platforms were full of phrases such as "same-day approval," "available for the unemployed," "credit score doesn't matter," and "mobile loan. " When someone in urgent need of cash clicked on them, they were immediately connected to a chat room or consultation channel.

If the consultation process asked for a social media account or information about people nearby, that data could be used to identify the victim's network or to intensify collection pressure. The consultations generally began like ordinary loan inquiries.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

One channel asked for a name, date of birth, and contact number. Another told the user to stay in the chat room while it was "checking product approval.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon." Yet another explained that using a mobile phone line was simpler than a small loan. A warning on the online chat screen said, "Channel with unverified business information," but the consultation continued anyway.

The channels differed, but the information they demanded was similar. Before discussing loan amounts, interest rates, or repayment methods, they repeatedly tried to confirm personal details and reachable people nearby first.

The questions kept coming: Could family contact numbers, friends' numbers, workplace contacts, and the company phone number be provided? Rather than income or credit, which banks usually check, the process seemed focused on identifying who could be pressured if the borrower failed to repay. Once the number was handed over, illegal loan calls came dozens of times a day When the reporter asked why they needed the contact details of people around him, the consultation went no further.Rather than explaining loan eligibility or review procedures, the other side cut off the conversation with a remark like, "Then look elsewhere. " No loan contract was signed and no money was actually deposited.But by then, the name, date of birth, and part of the phone number left during the consultation had already been handed over. Even after the reporter stopped the conversation, similar loan-related calls continued for days.Some numbers were labeled in a caller ID app as "loan," "loan guidance," or "warning. " Dozens of calls came in every day, enough to disrupt work.Because the reporter used a dual reporting number, it was easy enough to clean up the line and move on. But the situation is different for someone who truly needs emergency cash.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

If family contact details and workplace information have already been handed over in a situation where rent, hospital bills, credit card debt, and living expenses are all overdue, it is hard to simply end the relationship by cutting off the consultation. In other words, personal information and relationships become a weakness before the money is even borrowed .

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.The reporter also tried to contact actual victims during the investigation, but many were reluctant to speak to the media. The burden of being identified and the fear of further retaliation were too great.

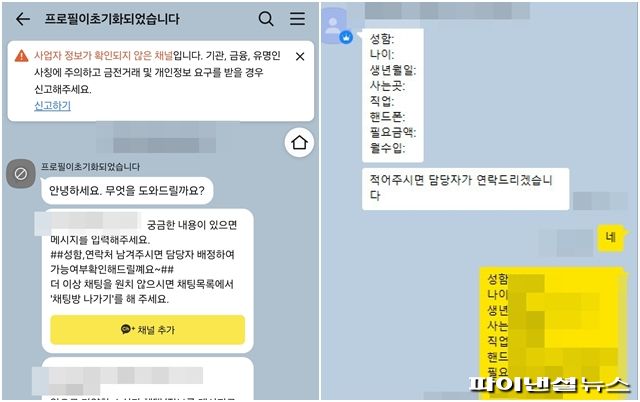

Victims who had already experienced collection calls and contact with people around them feared exposing their daily lives. Since they still lived with the anxiety that illegal collection could start again at any time, it was not easy for them to speak publicly about what had happened.A screen from an online loan consultation showing the warning, "Channel with unverified business information. " The company erased its profile and disappeared.The photo on the right shows another illegal lending operation. During the consultation, users were asked to enter personal information such as name, date of birth, occupation, mobile phone number, and desired loan amount.

Photo by Han Seung-gon. One consultation channel also explained a method involving an additional mobile phone line or handset installment payments .It also added that there would be "no impact on your credit score. " But a mobile line and installment contract still remain under an individual's name.If handset payments or telecom bills fall behind, delinquency problems can arise, and the risk that the SIM card or identity information could be abused in other crimes cannot be ruled out. Reports are rising, but collection is becoming more persistent The damage from illegal private finance is also reflected in consultation statistics.

According to the "2024 consultation results of the Illegal Private Finance Victim Reporting Center," released by the Financial Supervisory Service (FSS) in March 2025, there were 63,187 reports and consultations related to illegal private finance in 2024. 0%.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

The operator changes phones and bank accounts, moves offices, or works from a place where their location is not exposed. That is why, even if a victim reports the case, it inevitably takes time to identify the other party.

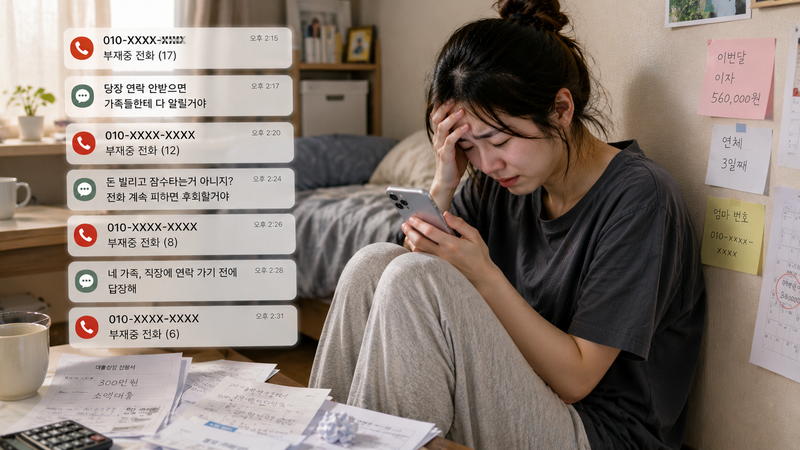

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.In the meantime, illegal collection continues. Lee said, "Money may be late by one minute or one day, but they seize on that and demand more.

" He added, "There are also cases that escalate into secondary and tertiary crimes, such as demanding nude photos, asking someone to open a bank account, or asking them to create a SIM card. " AI-generated infographic The system has been strengthened, but the psychological barrier to reporting remains Given the situation, the government is also stepping up its response.

President Lee Jae-myung emphasized the public role of financial institutions at a State Council of South Korea and Emergency Economic Review Meeting held at Cheong Wa Dae on the 6th, pointing to the reality that borrowers with mid- to low-credit scores are being pushed into secondary financial institutions, private lenders, and loan sharks. Institutional safeguards have also been added.

The revised Act on Registration of Credit Business and Protection of Financial Users, which took effect on July 22 last year, limits the validity of anti-social loan contracts. Contracts involving sexual exploitation, human trafficking, bodily injury, assault, or threats, as well as ultra-high-interest contracts exceeding 60% per year, three times the legal maximum rate, may be void for both principal and interest.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

\r\nHowever, victims still find it difficult to report. Some delay reporting out of fear that their family or company will find out, and collection efforts can continue while they are gathering evidence.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.In many cases, the contact numbers or accounts victims know are burner phones or burner bank accounts, so the anxiety does not disappear immediately even after a report is filed. AI-generated image to help readers understand the article Illegal collection spreads to family and workplace Collection efforts do not stop with the victim.

They may repeatedly call a family-run restaurant to disrupt business, or contact a company owner and coworkers to pressure them into repaying the money instead. There are also cases of posting IOUs on social media or tagging acquaintances to paint the victim as a "fraudster.

" More recently, AI-generated composite images have also been used as tools of intimidation. The pressure the reporter felt during the consultation stage was brief.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

Hanging up the phone was enough to end it.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

Family numbers, company numbers, acquaintances' contact details, and social media accounts all become channels for collection.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.Instead of calculating principal and interest, borrowers end up worrying first about who will be contacted today.

Lee said, "There was a case where someone borrowed 150,000 won and, six months later, had been extorted out of 150 million won." He added, "It is a structure in which money keeps being taken away." He said, "It does not end when you repay the money.

In some cases, the collection becomes even more aggressive after repayment." He went on to say, "Illegal private finance should not be seen as simple loan sharking, but as a new type of financial crime that uses burner phones and burner bank accounts," and pointed out that "the moment you borrow money, your personal information becomes a weakness, and that weakness is used to keep the victim trapped." We record the stories of real lives in writing.Even if rough around the edges, we capture the words gathered on the scene as they are.From alleyways and markets to someone's workplace, the record of an ordinary day that we passed by comes to our readers.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.

If you would like to follow [Recorder of the Low Places] more easily, please subscribe to the reporter page.

On the right are records of loan guidance calls received on a reporting number after the consultation. Photo by Han Seung-gon.hsg@fnnews.com Han Seung-gon Reporter