The Shadow of Large-Cap Concentration: 64% of KOSPI Stocks Still Undervalued

- Input

- 2026-05-24 18:10:17

- Updated

- 2026-05-24 18:10:17

According to the Korea Exchange (KRX) on the 24th, KOSPI's price-to-book ratio (PBR) stood at 2.40 times as of the 22nd, a sharp improvement from 1.35 times at the end of last year. Compared with 0.88 times on May 22 last year, it has risen by about 173%.

PBR is an indicator that shows how the market values a stock relative to its equity value. In general, a PBR below 1 is interpreted as a sign of undervaluation, meaning the market capitalization falls short of the company's net asset value on the books.

Backed by KOSPI's steep rally, South Korea's stock market briefly overtook Taiwan in market capitalization in mid-month. It now ranks sixth in the world, behind the United States, China, Japan, Hong Kong and India.

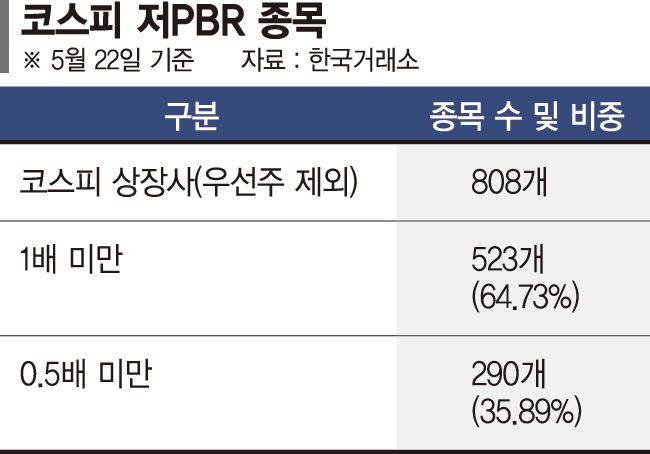

However, as the market's growth has been driven by large-cap stocks, many companies still have not crossed the 1-times PBR threshold. Of the 808 KOSPI-listed companies, excluding preferred shares, 523 stocks, or 64.73%, had a PBR below 1. Another 290 companies, or 35.89%, were below 0.5 times.

At the end of last year, 560 of 816 stocks, or 68.63%, had a PBR below 1. Even though KOSPI has surged 86.22% so far this year, 6 out of 10 stocks are still stuck at undervalued levels.

Brokerage analysts say the market's rise has been led by Samsung Electronics Co., Ltd. (SEC) and SK hynix, so polarization across individual stocks is inevitable. Lee Jae-man, a researcher at Hana Securities, said, "KOSPI's gains have been driven mainly by Samsung Electronics and SK hynix, and their combined market capitalization weight in KOSPI has risen to as much as 48%." He added, "Based on expected net profit in December, Samsung Electronics and SK hynix account for as much as 72% of KOSPI's total net profit, so this is only natural."

As the Government of South Korea is focusing on improving the market's fundamentals, low-PBR companies may also face the risk of being pushed out if they fail to strengthen competitiveness and improve shareholder returns.

A brokerage industry official said, "Even in a booming market, the fact that PBR has not improved means earnings and shareholder returns are still not strong enough." The official added, "Undervalued companies need to work harder to raise their corporate value."

Some also expect the introduction of a Korean-style bear hug to speed up the delisting of extremely undervalued listed companies. A bear hug refers to a tactic in which an acquirer publicly expresses its intention to buy and pressures a merger and acquisition by offering a price above the market level. If management refuses, it may face criticism for harming shareholder value.

Kim Soo-hyun, a researcher at DS Investment & Securities Co., Ltd., said, "The number of listed companies per $1 trillion of Gross Domestic Product (GDP) in South Korea is 1,368, about 10 times the level in the United States." He added, "The Government of South Korea and the ruling party are pushing policies aimed at allowing the market to self-correct, as in the United States and Japan."

He went on to say, "As the Financial Services Commission (FSC) establishes guidelines and pushes ahead with revisions to disclosure rules, an environment will be created in which underperforming and troubled companies can become targets of hostile M&A." He added, "In effect, a Korean-style bear hug appears likely to be permitted."