"Even Without Investing in Stocks, You Can Receive 5.54 Million Won a Month"... If You Use This Method, the 1 Million Won Pension Becomes 1.36 Million Won [Retiree X’s Plan]

- Input

- 2026-05-30 08:30:00

- Updated

- 2026-05-30 08:30:00

[Financial News] Park Jeong-ho, 68, a pseudonym, who lives in Eunpyeong District, Seoul, receives 1.84 million won a month from the National Pension Service (NPS). Including the period after retirement when he was rehired, his contribution history is nearly 30 years. His wife, Kim Jeong-hyeon, 66, a pseudonym, receives 430,000 won a month. Kim said, "My husband kept paying while working at a company, but I had a long period when I stopped working to raise our children. We grew old together, but our bank accounts are completely different." They built a household together, yet their retirement pensions are very different. More than four times different.

930,000 couples receive pensions together... the average is 1.2 million won

According to data released by the Ministry of Health and Welfare (MOHW) on May 20,the number of married couples receiving the National Pension Service (NPS) together reached 930,853 couples, or 1.86 million people.The figure has steadily risen from 428,000 couples in 2020 to 625,000 in 2022 and 783,000 in 2024, and it surpassed 930,000 couples for the first time this month. In six years, it has more than doubled. As a result, the share of married couples among all old-age pension recipients rose from 19.4% in 2020 to 28.5%. Three out of ten recipients are married couples.

The average combined pension for couples is 1.2 million won a month as of this monthThat is 1.5 times higher than the 810,000 won average in 2020.

However, the average combined pension amount for couples varies widely.

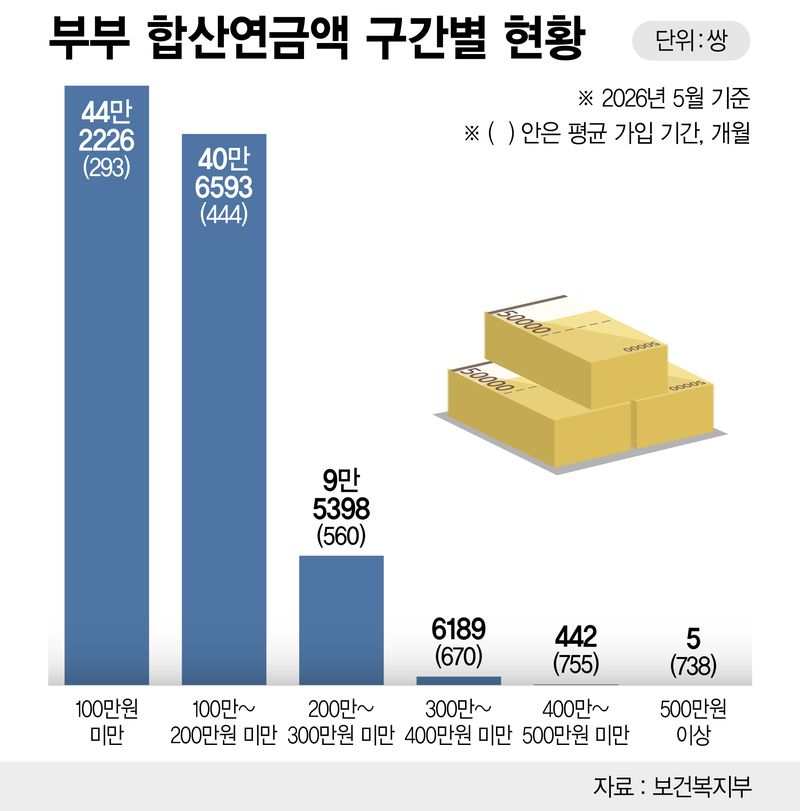

By bracket, the largest group is couples receiving less than 1 million won combined, at 422,000 couples. Another 407,000 couples receive between 1 million and 2 million won, 95,000 couples receive between 2 million and 3 million won, and 6,636 couples receive more than 3 million won. Nearly half of all couples receive less than 1 million won together.

The minimum monthly living expense for retirement, based on an individual, is 1.392 million won(according to a 2024 survey by the National Pension Research Institute), which means the combined amount for two people does not even reach that level.

There are couples receiving a combined 5.54 million won... and the reason was simple

At the other end of the spectrum, there are couples receiving 5.54 million won a month combined. There was a reason.According to the Ministry of Health and Welfare (MOHW), the couple's combined contribution period was 677 months. The husband contributed for 333 months and receives 2.65 million won, while the wife contributed for 344 months and receives 2.89 million won.

They alsoapplied for deferred pension payments for five yearsto further increase their benefits.

The couple with the longest combined contribution period has 902 months. Each spouse contributed for 451 months. The husband receives 1.59 million won a month, and the wife receives 1.29 million won. They have been enrolled since the pension system was introduced in 1988 and used voluntary continued enrollment and back payments.

The reason is simple: each of them paid in for a long time. For couples receiving between 3 million and 4 million won, the average combined contribution period is 670 months, 2.3 times longer than that of couples receiving less than 1 million won.

The number of high-benefit couples receiving more than 3 million won rose from 70 in 2020 to 6,636 this month, an increase of about 94 times in six years. As long-term contributors begin to reach pension age in earnest, the upper end is rising quickly.

Why do bank accounts diverge within the same household?

Pension payments differ not only from family to family, but even within the same household.

The gap between Park Jeong-ho and Kim Jeong-hyeon's monthly pensions, 1.84 million won and 430,000 won, is not just the result of personal choice. It is the result of the system.

When the National Pension Service (NPS) began in 1988, women who left their jobs because of marriage or childbirth had to pay premiums on their own. That was not an easy choice without income.If they applied for contribution exemption, that period was completely excluded from their enrollment history. The five- or ten-year gap is now showing up in their bank accounts.

As of January 2026, the average monthly old-age pension for women was 432,000 won, while for men it was 821,000 won. Among the 116,166 people receiving more than 2 million won a month, only 2,577 were women, or 2.2%. The remaining 113,589, or 97.8%, were men.

The number of female recipients rose 80-fold, from 30,000 in 1999 to 2.41 million in January. The number of recipients has surged, but the gap in benefit amounts has not narrowed.

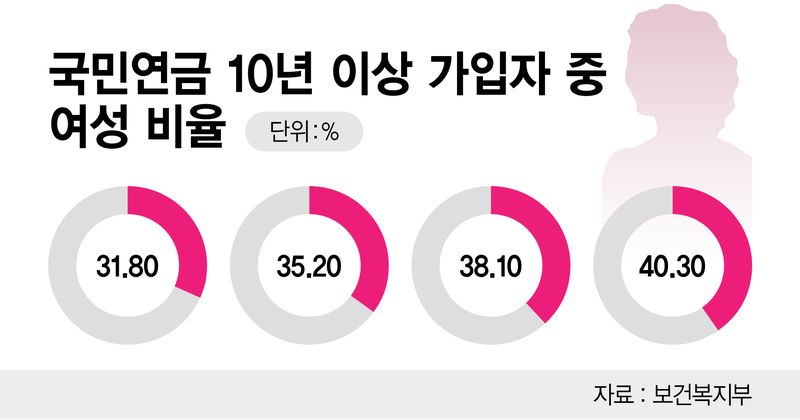

There are signs of change. According to the Ministry of Health and Welfare (MOHW), the share of women among those enrolled for at least 10 years rose steadily from 31.8% in 2018 to 40.3% in 2024. The increase reflects more women building contribution records through voluntary enrollment even without income.

The number of women enrolled voluntarily rose from 20,000 in 2005 to 308,000 in 2020. More time is needed before the gap narrows, but the direction is changing.

How can the gap be reduced?

Kim Seong-ho, 56, a pseudonym, who lives in Yangcheon District, recently logged into the Financial Supervisory Service (FSS)'s integrated pension portal and felt somewhat relieved after checking his expected benefits. If he maintains his current enrollment status, he is expected to receive about 1.65 million won a month starting at age 65. That is the result of paying premiums continuously for nearly 27 years.

By contrast, his wife, Lee Mo, 52, is expected to receive about 1 million won a month. She had periods when she stopped working for marriage and childcare, and her total contribution period is about 18 years so far. Kim said, "I didn't know the pension gap would be this big even though we're growing old together. Raising children isn't exactly a break from work, so I feel a little wronged."

There is still a way to narrow the gap.

It is back-payment.By paying premiums now for past periods of contribution exemption, members can extend their enrollment history.Up to 10 years, or 120 months, can be covered. If a member remains in the 10- to 19-year range, monthly benefits are usually only 200,000 to 600,000 won. But once the total exceeds 20 years, the likelihood of entering the 1 million won-plus bracket rises sharply. The total amount paid and the expected increase in benefits should be compared first.

Even without income, one can pay premiums as a voluntary member. After age 60, another option is voluntary continued enrollment, which extends the period until age 65. Starting in 2026, the childbirth credit has been expanded to 12 months for the first child. Because credits are not always applied automatically, it is necessary to check directly with the National Pension Service (NPS).

If you take it early, benefits are cut by 30%; if you delay, they rise by 36%

The gap also appears in the age at which benefits begin.

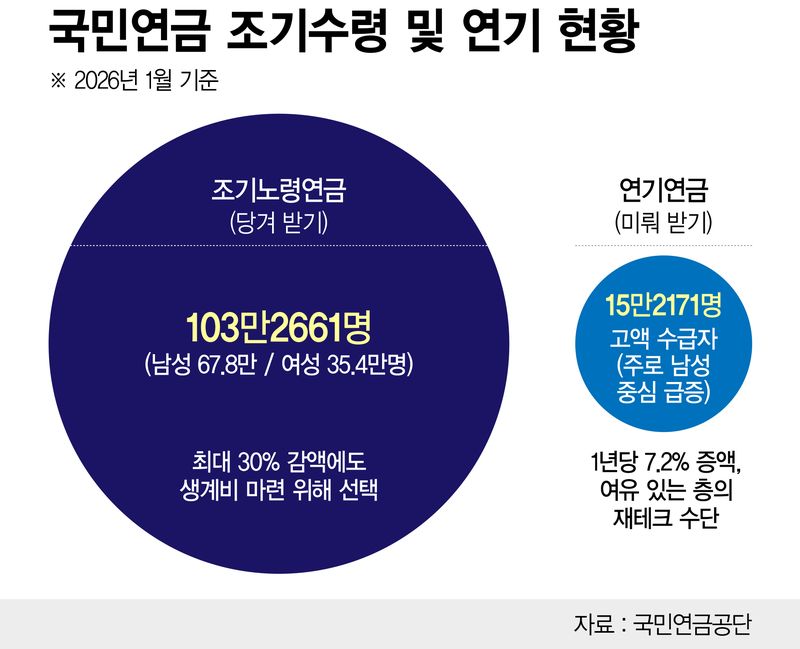

As of January 2026, there were 1,032,661 recipients of early old-age pensions. That is 1.5 times higher than the 673,842 recipients in 2020, just over five years earlier. People apply even knowing that benefits are reduced by 30%. In practice, retirement at age 60 comes before the pension start age of 63 to 65. For those who struggle to find reemployment, that gap is a cliff in living expenses.If benefits are taken five years early, the monthly amount falls by 30%, and the reduction remains for lifeThe reduction remains in effect until death.

By contrast, the number of deferred pension recipients surged 2.6 times over the same period, from 58,908 to 152,171.For every year of delay, benefits rise by 7.2%, and if delayed for the maximum five years, payments increase by 36%.The couple receiving the record-high combined 5.54 million won chose exactly this option. Those with room to wait do so, while those in urgent need take benefits early. That is why retirement inequality is widening even within the National Pension Service (NPS).

Starting in June this year, the income threshold for reducing benefits for working recipients will rise from 3.09 million won to 5.09 million won a month. Retirees who are reemployed will be able to combine pension income and earned income more flexibly than before.

The National Pension Fund has grown to 1,600 trillion won... If you understand and prepare, your benefits can grow

Recently,the sharp rally in the stock market pushed the National Pension Fund above 1,600 trillion won, easing concerns about depletion.The system has also changed.

But the 430,000 won a month that appears in Park Jeong-ho's wife's bank account will not change overnight. The difference between a combined 5.54 million won and 1.2 million won is not luck, but a record. How long each person paid in, and how consistently. First, couples should check how many years of contributions they have now and whether any gaps can be filled.

According to the National Pension Research Institute, 86.6% of members as of 2024 do not know their expected pension amount. On the Financial Supervisory Service (FSS)'s integrated pension portal, users can check not only the National Pension Service (NPS) but also retirement pensions and private pensions at a glance. On the National Pension Service (NPS) website's "My Pension Lookup" page, users can also simulate expected benefits before and after back-payment.

The old formula that "retirement means stepping away" is breaking down. In an era when life expectancy reaches 83, Generation X is entering retirement in earnest, and the very concept of retirement is being redefined. The story of their "second act" is captured inRetiree X’s Planand will meet readers every Saturday morning. If you subscribe to the reporter page, you can receive it conveniently.

kkskim@fnnews.com Kim Gi-seok Reporter