"People in Their 20s Made Tens of Millions of Won from Chicken Money"...A Powerful Weapon Praised by Buffett and Munger [In Chibeom's Stock Investment Boot Camp]

- Input

- 2026-05-23 09:00:00

- Updated

- 2026-05-23 09:00:00

It may vary by person, but the average monthly allowance for college students these days is said to be about 510,000 won. With dining-out prices rising, investing can feel like a luxury after covering food, transportation, and even clothing expenses. But what if you started putting to work just 50,000 won a month, or 10% of that 510,000 won? If you invested for 10 years at the S&P 500's historical long-term annual return of 10%, the results would be remarkable.That is only 50,000 won a month. Saving 50,000 won every month would add up to 6 million won in principal over 10 years. But once the 10% annual compound-interest engine kicks in, your assets would grow to about 10.24 million won after 10 years. That means 4.24 million won in pure interest income generated by compounding, or a bonus of more than 70% on top of your principal.

"Making money with the money I have, a system where money makes money. That's capitalism."

That line comes from the popular drama Itaewon Class. Robert Kiyosaki, author of the investment bestseller Rich Dad Poor Dad, also advises that true financial freedom comes from building a system in which the money you have saved grows on its own while you sleep or do other things — in other words, a structure where money makes money.

"How much can you really make with a few hundred thousand won?" The powerful weapon called 'time'

Of course, such advice sounds cliché to college students in their 20s or young professionals who have only just stepped into the stock market. "All I have in my bank account is a few hundred thousand won, maybe a few million at most as seed money." "With so little money, how much can money really make money?" Some even chase high-risk, soaring stocks or cryptocurrencies and end up with painful losses.But there is no need to be discouraged. People in their 20s have the most powerful weapon of all. It is time — the weapon that allows them to build a system in which money works for them and to let their money grow like a snowball.

The insight of one of the world's richest men, Warren Buffett: compounding

What was the secret behind Warren Buffett's rise to immense wealth? In a 2010 official letter to the charity The Giving Pledge, Buffett explained why he accumulated such vast assets."My wealth is the result of being born in the United States, having a few good genes, and the power of compound interest coming together."

Buffett, too, pointed to the magic of time: compounding. As you may know, most of Buffett's wealth was built only after he turned 50, when compounding began to accelerate. If people in their 20s start investing even small amounts now, they can enjoy the satisfaction of seeing their assets snowball for even longer than Buffett's did. There is absolutely no need to be disappointed by the fact that the amount is small today.

First step: Invest the price of chicken twice a month, or 50,000 won, and grow it to 10.24 million won in 10 years

It may vary by person, but the average monthly allowance for college students these days is said to be about 510,000 won. With dining-out prices rising, investing can feel like a luxury after covering food, transportation, and even clothing expenses. But what if you started putting to work just 50,000 won a month, or 10% of that 510,000 won? If you invested for 10 years at the S&P 500's historical long-term annual return of 10%, the results would be remarkable.That is only 50,000 won a month. Saving 50,000 won every month would add up to 6 million won in principal over 10 years. But once the 10% annual compound-interest engine kicks in, your assets would grow to about 10.24 million won after 10 years. That means 4.24 million won in pure interest income generated by compounding, or a bonus of more than 70% on top of your principal.

Shall we increase the investment amount a little? If you cut back on delivery food three or four times a week and invest 100,000 won a month, you would have 20.48 million won after 10 years. If you work a few more part-time shifts or save more of your allowance and invest 150,000 won a month, that becomes 30.73 million won. And if you enter the workforce and begin investing 200,000 won every month in earnest, you would hold 40.97 million won in your hands 10 years later. Small habits such as investing 50,000 won or 100,000 won a month in your 20s can lead to results that put you ahead of others in your 30s.

If a discharged soldier has saved 20 million won, that is equivalent to earning money for more than 10 years

The number of active-duty soldiers discharged each year is said to be around 180,000 to 200,000. For these individuals, if they had not spent a single won of the salary they received during their 18-month service period in the Army — or if they had deposited it into the Military Service Savings Account — the amount they could receive would be roughly 30.39 million won*. Even if they spent about 10 million won after discharge on necessities such as a laptop or travel expenses, they would still have 20 million won left. As explained above, that is the investment return they could achieve by investing 100,000 won a month for 10 years. In other words, they already have a substantial seed fund. Considering the magic of time, or the compounding effect, that money can create in the future, they should focus more on investing than on spending.*30.39 million won = (accumulated base salary of 20.10 million won) + government matching support of 9.90 million won + bank and state-supported interest of about 390,000 won

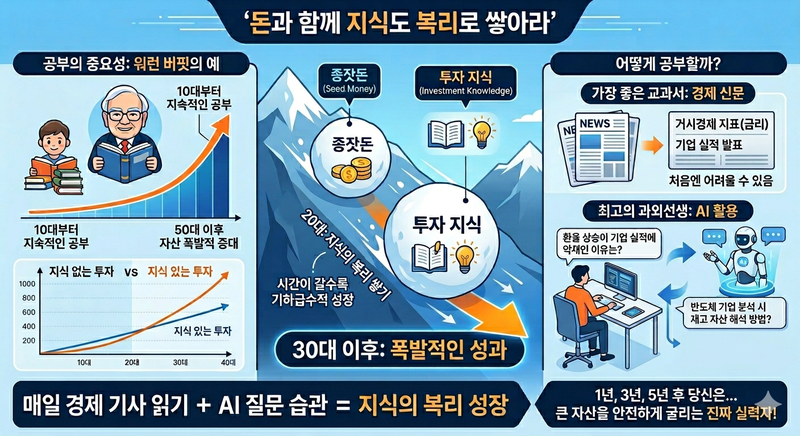

Second step: Build knowledge through compounding. Using AI is also effective

The second step may be the one you least want to hear, but it is about studying. While you are saving money, you also need to let your knowledge compound. Warren Buffett was able to dramatically grow most of his assets after his 50s because he had spent decades studying without stopping since his teens. For people in their 20s, when seed money is still limited, this is not just a period for parking money. It is the time to build the compounding of knowledge — to develop the ability to read the market before serious capital accumulates. If both your invested money and your knowledge snowball through compounding, you will achieve remarkable results by the time you reach your 30s.How should you study? You do not need to open a heavy textbook just because you are studying stocks. The best textbook is the financial newspaper. At first, even articles on macroeconomic indicators such as Fed rate hikes or corporate earnings reports may be hard to understand. At times like this, use the best tutor our generation has been given: AI.

If you get stuck while reading a financial article, copy the part you do not understand and ask AI. Try questions like, "Why is a rising exchange rate considered bad for corporate earnings?" or "How should I interpret inventory levels when analyzing a semiconductor company?" AI will explain complex macroeconomic indicators and difficult corporate analysis points in a way that is easy to understand and tailored to your level. If you keep reading financial news and asking AI questions about what you do not understand for one year, three years, or five years, your investment knowledge will also grow exponentially through compounding, and you will eventually become someone with the real skill to manage large assets safely.

For absolute beginners in investing, ETFs are better than direct stock picking

At this point, one question naturally arises. "I understand the principle, but which stocks should I put my precious money into to stay safe?" For novice investors in their 20s, analyzing individual companies and finding opportunities can be more difficult and risky than expected. That is why I recommend investing in domestic and overseas Exchange Traded Funds (ETFs), which adopt the concept of regular installment investing.An ETF is, simply put, a fund product like a "mixed gift set" that can be bought and sold directly on the stock market. For example, you can buy a U.S. index ETF that holds 500 of the world's best companies, such as Apple Inc., Microsoft, and Google, with just a few tens of thousands of won. Even if one company you bought goes under, the other 499 companies can hold up, giving you a built-in safeguard suitable for long-term compounding.

Of course, you should approach this through regular installment investing, buying the fund mechanically every month. When stock prices rise, you buy fewer units of the fund. When prices fall, you buy more units at a lower price with the same amount of money, which helps reduce your average purchase cost.

'Emotional highs and lows' and 'buy-sell-buy-sell' are the biggest enemies

It looks very easy. But many people in their 20s give up before they ever experience the magic of compounding. They keep checking their smartphone screens, reacting emotionally to whether their stocks are up or down today. If prices rise a little, they sell to lock in profits. If prices fall a little, they panic and cut losses. On this, Charlie Munger, Warren Buffett's lifelong partner and a legendary investor, offered advice in his book Poor Charlie's Almanack."The first rule of compounding is to never interrupt it unnecessarily."Charlie Munger, Poor Charlie's Almanack

Compounding shows almost no visible effect in the first one to three years. It feels boring because it seems no different from the principal. But if you keep adding money steadily through an installment ETF and do not withdraw it, there comes a point when the curve suddenly rises steeply. Munger said that the key to making money in investing is not the busy act of buying and selling, but the patience to let compounding work. The more your emotions waver, the more you need patience — close the stock chart, focus on your studies if you are a student, and on your work and precious daily life if you are employed, while not interfering with the snowball as it grows on its own.The privilege only people in their 20s have: decades of time to benefit from compounding

In the book The Almanack of Naval Ravikant: A Guide to Wealth and Happiness, which is about the legendary Silicon Valley investor Naval Ravikant, the concept of compounding is expanded one step further."All the returns in life, whether in money, relationships, or good habits, come from compounding."Naval Ravikant, The Almanack of Naval Ravikant: A Guide to Wealth and Happiness

I hope the wealth-building efforts you begin in your 20s are not just about increasing your bank balance by a few tens of thousands of won. They are a process of understanding the capitalist system, learning how to invest time, and automating the good habit of patience. To emphasize it again, the magic of compounding depends not on how much you start with, but on how long you keep it working without interference. Do not take lightly the privilege of having decades of time left in your 20s.The most valuable asset people in their 20s have is time.

[About the Author]

Senior Managing Director In Chi-beom worked for 30 years in corporate communications as a leader responsible for PR, IR, ESG, and CSR across finance (Samsung Life Insurance), IT (AhnLab, Inc., Hancom, SK Communications), and retail (Samsung Tesco). He is currently focused on writing books about investing and corporate communications at KPI Investment Advisory. He believes that stock market success comes above all from automating the right habits for handling money.

[email protected] Kim Seong-hwan Reporter