"The Middle East Is Not the End" ... The Wall of U.S. Rates That Is Cementing the 1,500-Won Era

- Input

- 2026-05-17 16:22:07

- Updated

- 2026-05-17 16:22:07

On the 17th, the financial sector said that the factors determining the won–dollar exchange rate are shifting beyond the geopolitical risk of the Middle East conflict and toward U.S. long-term interest rates.

For now, the Middle East conflict remains the key factor. A stronger dollar, driven by expected demand for dollars amid uncertainty and the possibility of a rate hike due to high oil prices, is pushing the exchange rate higher. The problem is that even if the war ends, structural factors that support a weaker won remain.

There is room for the exchange rate to correct if international oil prices, which would likely turn lower once the war ends, temporarily ease the burden on inflation. But some believe high oil prices will persist if the Middle East conflict drags on. That means there is still not enough reason for the Federal Reserve System (Fed) to abandon monetary tightening.

Persistent inflation is also testing the Fed's patience. In April, the United States Consumer Price Index (CPI) rose 3.8% from a year earlier. Core CPI, excluding the impact of oil prices, also rose 2.8%, beating market expectations.

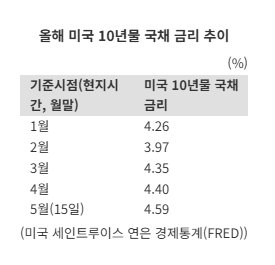

In the end, this environment is more likely to push up U.S. long-term interest rates, which have a more direct impact on the foreign exchange market than the benchmark rate. On the 15th (local time), the U.S. 10-year Treasury yield surged to 4.59%. On the same day, the 30-Year Bond Yield jumped to 5.12%, while Korean Treasury Bond Yield stood at 4.217% and 4.131%, respectively.

When U.S. market rates rise, dollars are drawn there, and pressure for foreign investors to leave the stock market increases. That makes the 'strong dollar, weak won' structure even more entrenched.

Even if the Bank of Korea (BOK) Monetary Policy Board raises the benchmark rate and the Fed chooses to hold steady, narrowing the US-Korea interest rate differential, Korea will still struggle to catch up with the United States in terms of market rates. That is because the Donald Trump administration is expected to push ahead with large-scale tax cuts as an economic stimulus measure ahead of the midterm election in November, which could send long-term rates higher again. Concerns over a wider fiscal deficit are expected to increase bond supply.

Jeong Yong-taek, chief economist at IBK Securities, said, "A current account surplus and capital inflows from inclusion in the World Government Bond Index (WGBI) could pull the exchange rate down to the mid-1,400-won range by the middle of this year or early in the third quarter," but added, "Once the war ends, U.S. policy will shift toward tax cuts, which will heighten concerns about the fiscal deficit and widen the yield curve (10-year yield minus the benchmark rate)."

Jeong noted, "Because Korea has relatively lower inflation and a smaller fiscal deficit than the United States, the market interest rate gap is expected to widen."

The domestic foreign exchange authorities have few effective options to respond to these external factors. In practice, the only tool available is to release dollars into the market. Foreign exchange reserves, the ammunition for such action, stand at about $430 billion, but they must also generate $20 billion a year in investment funds for the United States through interest and returns, making it impossible to deploy them freely.

[email protected] Kim Tae-il Reporter