A Young Worker Earning 2.6 Million Won a Month Still Struggles to Get By, Even While Saving — and It Wasn't a Matter of Willpower [Money Planning Office]

- Input

- 2026-05-30 15:00:00

- Updated

- 2026-05-30 15:00:00

Earning, spending, and saving money are lifelong routines, yet financial planning is often pushed aside. But money has its own age and will not wait. If you do not make choices along the way, it is left unattended; if you do not set a direction, it slips away. That is why we need to map out the flow of money across our entire lives.[Asset Planning Office]supports the design of a 'financial life' together with the Korea Financial Planning Association and the certification body for AFPK.

[Financial News] Wealth management also has a life cycle. The approach for people in their 20s is different from that of people in their 50s. The first direction is set in your 20s, when you begin earning money. If you train yourself to become a disciplined asset manager during this formative stage, everything that follows becomes easier. Of course, the gap between ideals and reality is wide. Closing that gap requires a clear plan. Above all, for people in their 20s, financial planning goes beyond simple investing and is directly tied to survival.Start by cutting housing costs

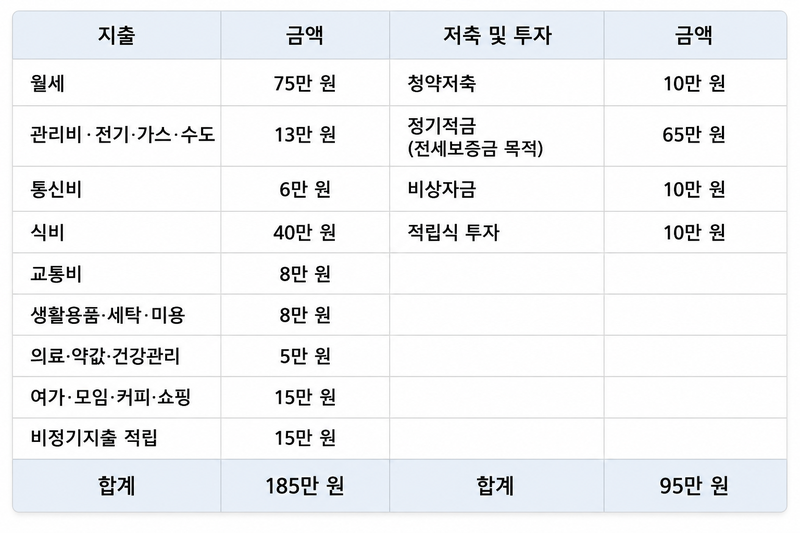

Take the case of Kim Ji-hoon, a 28-year-old man. By looking briefly into his life, we can find a direction for others in his age group. After graduating from college in the provinces and landing a job, he moved to Seoul. His take-home pay is about 2.6 million won a month. The first time he saw that amount in his bank account, he was thrilled. It was the first confirmation of what his efforts had earned him. But one year later, his account is empty.

The financial planner who advised him, Jo Hyeong-geun, an AFPK-certified planner, identified housing costs as the biggest leak. He pays a 10 million won deposit and 750,000 won in monthly rent for a studio apartment. Add maintenance fees and utility bills, and 900,000 won disappears every month. After paying phone bills and student loan installments, he is left with only about 1.3 million won. If a holiday or family event comes up, he has to rely on credit card installments. Cutting back on delivery food did little to improve the situation. In months when expenses rose, he had no choice but to reduce saving and investing.

Jo said that it is hard to save money with willpower alone, and he offered four guidelines for people in their 20s like Kim. What matters here is not awareness or understanding, but action. There is a vast gap between knowing something and awkwardly trying to start.

Young adults living in Seoul should check the housing support programs offered by the Ministry of Land, Infrastructure and Transport and the Seoul Metropolitan Government. What is needed is diligence, not cleverness. Kim's earned income exceeds 60% of the median income, so he does not qualify for the ministry's program. But he may meet the requirements for Seoul Youth Monthly Rent Support, which raises the threshold to 150%.

He can also make use of various jeonse lease and rental housing programs run by Korea Land and Housing Corporation (LH) and Seoul Housing & Urban Development Corporation (SH Corporation). There are more options than many people expect, so it is a good idea to check the relevant websites regularly for announcements.

Kim was able to receive Seoul's monthly rent support and save 200,000 won a month. It may seem like a small amount, but the effect grows over time. Jo explained that reducing monthly housing costs is not just about saving money, but about improving cash flow. He added that the savings created this way become the foundation for further saving.

Saving alone is not enough; there must be a goal

Saving money does not have to be the goal itself. The real issue is how to manage the money you have worked so hard to set aside. That is why money needs a destination.

Based on that idea, Kim set a goal of raising 30 million won for a jeonse deposit within two years so he could escape the burden of monthly rent. At first glance, that may not seem like a large sum, but Jo described it as a realistic benchmark for the minimum self-funded amount, typically 10% to 20%, required when taking out a Youth Jeonse Deposit Loan. In general, it is recommended to set overlapping plans: short-term plans of one to three years and long-term plans of five years or more.

Once you have created momentum and set a direction, the next step is to control irregular spending. This is the stage where you build a concrete method. In Kim's case, the main causes of the deficit were irregular expenses such as holiday spending, family events, and vacation costs. After adding them up and dividing by 12 months, the result was 150,000 won a month. That made the spending more predictable and therefore easier to control.

The final step is to build a structure that prevents money from leaking out. This means dividing bank accounts into categories such as salary, fixed expenses, living costs, and irregular expenses. When the paycheck comes in, fixed expenses such as housing costs and loan repayments are deducted first, and the budget for irregular spending is automatically transferred to a separate account.

Once spending money and saving money were separated, Kim naturally became more frugal. He used public transportation discount programs such as the Climate Card and cut food expenses to a minimum. As a result, his monthly living expenses were reduced to about 800,000 won. The money saved can then be redirected to savings. Jo advised that spending control must be built through structure, not willpower, if it is to last.

[email protected] Kim Tae-il Lee Hyeon-jeong Reporter