A $50 Billion Tokenization Market, but South Korea Is Still in Its Infancy... "Securing Liquidity Comes First"

- Input

- 2026-05-14 12:00:00

- Updated

- 2026-05-14 12:00:00

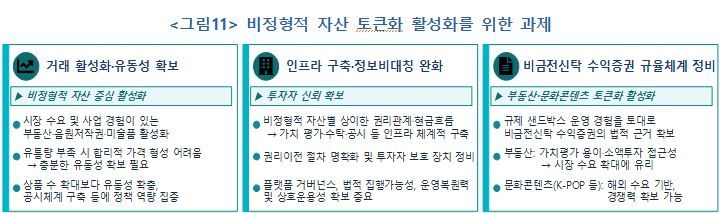

Park added that if sufficient circulation is not established in the early stage, it will be difficult to form rational prices and smooth trading, which could weaken investor trust. He said that rather than simply increasing the number of products, actual transactions must take place through abundant liquidity and standardized disclosure systems.

The Organisation for Economic Co-operation and Development (OECD) also identified a lack of liquidity and an underdeveloped ecosystem as reasons for the slow adoption of asset tokenization in a report published in January last year, titled 'Asset Tokenization and Distributed Ledger Technology in Financial Markets.' In other words, there is not enough liquidity for large institutional investors to enter the market.

As of the end of March, the global asset tokenization market was worth $50.37 billion, or about 75 trillion won, while South Korea's cumulative fractional investment market stood at about 640 billion won as of January. The figures are not directly comparable because the scope and timing of the data differ, but a simple comparison shows that South Korea's market is less than 1% of the global total.

It is also necessary to build core infrastructure related to asset valuation, custody, disclosure, transfer of rights and investor protection to reduce information asymmetry between issuers and investors.

Establishing a legal basis is essential. Rather than relying on limited frameworks such as regulatory sandboxes, a broader foundation must be created. In South Korea, amendments to the Act on Electronic Registration of Stocks and Bonds and the Financial Investment Services and Capital Markets Act in February created an environment for the issuance and circulation of token securities. However, the revisions only included Investment Contract Securities, while non-monetary trust beneficiary securities such as those tied to real estate and music copyrights were excluded.

Park said government bonds and Money Market Funds (MMFs) are relatively easier to tokenize because they have standardized cash flow structures and can improve accessibility through smaller denominations. By contrast, stocks are more difficult because corporate actions such as dividends, paid and bonus share issuances, and treasury share cancellations must all be handled on-chain.

Park explained that asset tokenization can greatly improve transaction efficiency by processing the entire process, from trade execution to settlement and post-trade management, on a distributed ledger. He added that it can enable transactions beyond time and geographic constraints, increase flexibility in financial market operations, and even support commodity settlement, thereby eliminating settlement and partial-settlement risks.

The next challenge is ensuring interoperability. The OECD also cited limited interoperability as one of the constraints on the tokenization market. The problem is that individual projects are not compatible with one another. In other words, they are conducted in a closed manner within a specific institution's private blockchain, making it difficult to move or connect assets across different chains.

As a means of payment, Park proposed central bank money, including Central Bank Digital Currency (CBDC), as well as deposits and deposit tokens, to preserve the singularity of money and ensure trust. He said stablecoins could be used as a supplementary option if strict regulatory compliance, feasibility and the stability of reserve assets are secured.

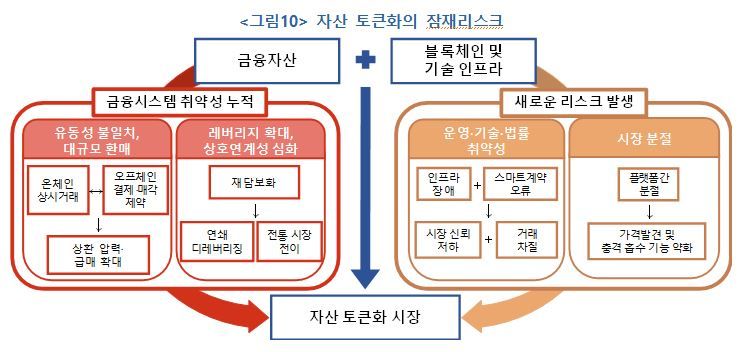

Tokenization could also increase leverage and deepen interconnectedness, raising concerns that systemic vulnerabilities may accumulate. Park noted that while it makes asset fragmentation and collateralization easier, it could also encourage rehypothecation. He warned that if prices fall, it may trigger sharp asset sales and greater market volatility.

Above all, if ties with the stablecoin market become stronger, shocks could spread to the short-term government bond and deposit markets, which serve as its underlying assets. Park said, "We are paying close attention to the possibility that these issues could accumulate into systemic risk."

taeil0808@fnnews.com Kim Tae-il Reporter