"Put 20 million won in your middle school daughter’s account and buy Samsung Electronics stock for her, and the tax is zero"... Even giving your son 200 million won for his wedding can be 'tax evasion' [Retiree X’s Plan]

- Input

- 2026-06-13 07:55:08

- Updated

- 2026-06-13 07:55:08

"Min-jun has 120 shares of Samsung Electronics. How many do I have?"That is the kind of question that makes many parents’ hearts sink these days. More and more parents are gifting assets to their children while they are still minors, then growing those assets through stock investments and other means. When the children become adults, the enlarged assets become entirely theirs, with not a single won in tax.

[Financial News] A report that, as of 2024, more than 700 recipients under the age of 1 had received gifts before turning one became a major talking point. Their average gift amount per person was 91.41 million won, far above the annual salary of an ordinary office worker. That is why people reacted with a mix of envy and frustration, saying, "How is the world turning out like this?"

But the real issue is the reality of wealth inequality hidden behind those numbers. This is the structural backdrop that forces parents in their 50s and 60s, facing their children’s independence and marriage, to quickly start calculating gift tax.

Widening wealth gaps: 'Give it while you're alive'

In fact, the wealth gap is widening far more sharply than income inequality.

According to the Survey of Household Finances and Living Conditions by the Ministry of Data and Statistics, the Bank of Korea, and the Financial Supervisory Service (FSS), the top 10% of households by assets held 44.4% of total net assets, while the bottom 50% accounted for just 9.8%.

The people who feel this shift most painfully are today’s parents in their 50s and 60s. Their children are reaching marriageable age, but soaring home prices are on a completely different scale from what they faced when they were newlyweds. Inheritance feels like a distant future, while lease deposits and home purchases for their children are immediate realities. As a result, more parents are opening their wallets while they are still alive.

But this is not just a story about the wealthy. Any money given to help a child with a lease deposit or wedding funds is legally considered a gift. People who hand over money without fully understanding the rules often end upbeing asked by the National Tax Service to explain the source of the fundsand are usually caught off guard.ordinary parents

.

Gifting to minor children? ... The magic of compounding

The trend of gifting assets during one’s lifetime is expanding to minor children as well.

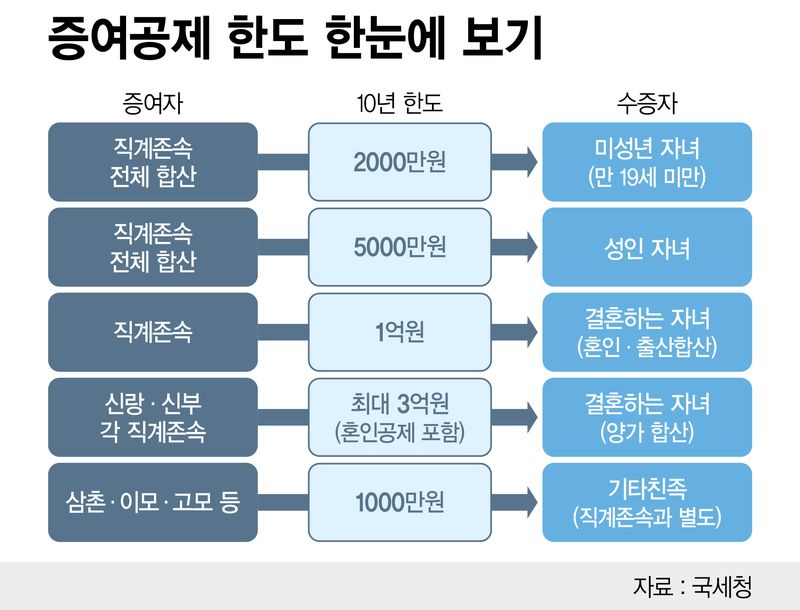

According to the National Tax Service, as of 2024, there were 14,217 minor recipients under the age of 18, accounting for 9.2% of all gift tax filings. The value of the gifted assets reached 1.2382 trillion won.At present,the gift tax deduction limit for minor children is 20 million won over 10 years

A look at gift tax deduction limits at a glance /Graphic by Reporter Jeong Gi-hyeonThe earlier you start gifting, the more times you can use the deduction. If you give 20 million won when the child is born, another 20 million won at age 10, and then 50 million won each at adulthood and at age 30, you can theoretically transfer a total of 140 million won legally and tax-free by the time the child turns 31.If investment returns are added on top of that, the gap widens even further. That is because gains from long-term investments in stocks or funds made with the gifted money are fully recognized as the child’s property.

There is, however, one thing to watch out for. If grandparents first give a child 20 million won and use up the deduction limit, the parents’ deduction room disappears. That is because the limit is calculated by combining both sides of the family.

Yom Ji-hoon, a tax accountant at Gahyeon Tax Corporation, explained, "There is no need to wait just to stay within the deduction limit." He added, "If you have the financial room, it can sometimes be better to acquire real estate in the child’s name early, even if that means paying some tax. Any increase in value after the purchase belongs to the child."

Once parents’ money is involved, the story changes

Although gifts to minor children are increasing, many parents still run into late reporting problems after giving money to adult children.

Park Jin-su, 59, who lives in Suwon, Gyeonggi Province, visited a tax accountant for the first time last year ahead of his son’s home purchase. His son was trying to sign a contract for a small apartment on the outskirts of Seoul, but his income alone was not enough to cover the down payment. After much discussion, Park and his wife decided to contribute 50 million won.

From Park’s perspective, it seemed like a natural thing to do. "I thought it was just a little help with my son’s home purchase, so I didn’t think there would be a tax issue," he said.

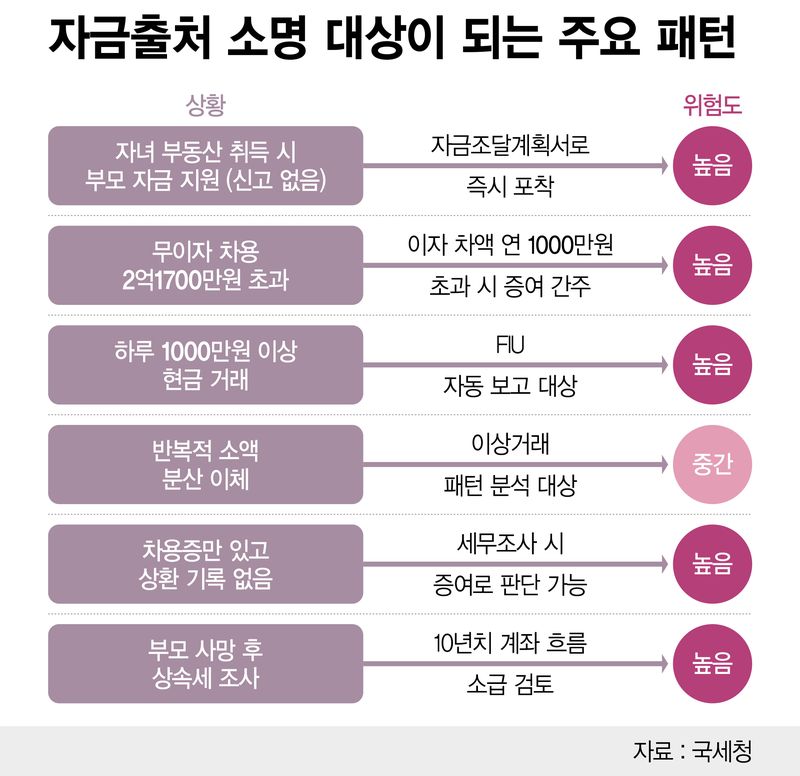

But once parents’ money is mixed into the process of a child acquiring real estate, the chance of being asked to verify the source of funds rises sharply. The son’s financing plan included the parents’ support, and Park later received a notice requesting an explanation of the source of the money.

The 50 million won Park sent was within the adult child deduction limit of 50 million won, so no gift tax was imposed. Still, the tax accountant he consulted advised that "even if there is no tax, it is better to file a gift report and document the source of the money for future explanation."

"If the father gives 50 million won and the mother gives 50 million won, isn’t that 100 million won?"

Park and his wife also learned a number of things for the first time during the consultation.

Under current rules,parents can receive a gift tax deduction of up to 50 million won over 10 years when gifting to an adult child (Article 53 of the Inheritance and Gift Tax Act). One common misunderstanding is to think this limit applies separately to each parent. But the tax law treatsall direct ascendants, including parents and grandparents, as one group. It is not calculated separately as 50 million won from the father and 50 million won from the mother.

Instead, the deduction resets every 10 years. If you gift 50 million won now, you can receive the 50 million won deduction again 10 years later. If the child is already an adult, simply filing now can make it possible to apply the deduction again after 10 years.

Uncles, aunts, and other collateral relatives are classified as a separate group. In that case, an additional deduction of up to 10 million won is available over 10 years. Even after using up the direct-ascendant limit, gifts from relatives are calculated separately.

For children about to marry, the 'marriage and childbirth deduction'

Park also has a 27-year-old daughter who is still unmarried. During the consultation, when the topic turned to her wedding funds, the tax accountant recommended making full use of the 'marriage and childbirth gift tax deduction,' which took effect in 2024.

Under this system, if a child receives assets from parents within two years before or after the marriage registration date, for a total window of four years, they can receive an additional deduction of up to 100 million won on top of the existing 50 million won deduction for adult children. In other words,up to 150 million won per child can be transferred without gift tax.

Even if the newlywed home contract comes before the wedding ceremony, the marriage deduction can still be considered as long as the money was given within two years before the marriage registration date. Since this deduction has a lifetime cap of 100 million won, using the full amount for marriage means the childbirth deduction cannot be claimed later when a child is born.

What if both the groom’s and the bride’s parents use the system? In that case, the groom’s side could provide 150 million won and the bride’s side another 150 million won, for a total of up to 300 million won in tax-free support for the newlyweds.

"Is a promissory note enough to stay safe?" ... The National Tax Service looks at bank balances

To avoid taxes, many parents try to treat the money as a loan rather than a gift. Park also asked, "If I write a promissory note and lend it interest-free, wouldn’t that be fine?"

The short answer is that this is a risky idea. Based on the current reasonable interest rate of 4.6%, gift tax issues arising from the interest difference may not be significant if the interest-free loan is about 217 million won or less. But that only applies to the interest calculation. Whether the principal was truly a loan must be proven separately through the promissory note, interest payment records, and records of principal repayment.

What matters more than the amount is whether it was really a loan.If a large sumis lent to a child with little or no income, and there are no financial records showing interest or principal repayment, the National Tax Service will treat the promissory note as a merely formal document and impose gift tax on the entire principal.

Hwang Jeong-gil, CEO tax accountant at Cheongdam Tax Management, said, "For example, if you want to borrow 300 million won from your parents and avoid gift tax issues, you should choose a structure that includes some interest payments." He added, "It is advisable to set a reasonable interest rate, write a promissory note, and transfer the interest to your parents’ account every year without fail." Hwang also noted, "Even if the interest-rate requirement is met, objective documentation of the loan agreement, actual interest payments, and proof that the child later repaid the principal from earned income are needed for the National Tax Service to recognize it as a real loan. Otherwise, not only the interest but the entire 300 million won principal could be assessed as a gift."

The National Tax Service and the tax industry are paying close attention to the following major patterns that trigger source-of-funds explanations.

The scarier problem is the one that appears years later

Park was able to sort things out relatively early, while the funds for the home purchase were still being reviewed. But in many cases, the problem surfaces much later.

There are cases where money parents contributed to help their children buy a home is checked again during an inheritance tax audit after the parents have died. Even if nothing seemed wrong at the time, past account movements remain on record. If they cannot be explained, additional penalties may be imposed.

Many people still think cash is safe. Butfinancial institutions report cash transactions of 10 million won or more per person per day to the Financial Intelligence Unit (FIU). Repeated cash transactions or split transfers can also become subject to source-of-funds analysis.

Tax accountants explain that "many people think it is fine as long as the amount does not exceed 10 million won, but in reality the entire flow of funds is often reviewed together."

In the end, the safest approach is to report within the deductible range and leave a clear record.

Is 'my' retirement secure?

After the consultation, Park went home and, for the first time, calculated his expected National Pension Service (NPS) benefits and the living expenses he would need after retirement. The calculations that began with his son’s housing funds led all the way to his daughter’s wedding funds, and he realized that his own retirement planning had been pushed to the back burner.

Today’s parents work hard to calculate what their children will need in the future. Their own retirement often comes second.

The old formula that 'retirement means exit' is breaking down. In an era when life expectancy reaches 83, Generation X is entering full-scale retirement, and the very concept of retirement is being redefined. The story of their 'second act in life' is captured in[Retiree X’s Plan]and will meet readers every Saturday morning. You can receive it conveniently by subscribing to the reporter page.

[email protected] Kim Gi-seok Reporter