Who Will Receive the High Fuel Price Support Payment? A Single-Income Family of Four Can Qualify with 320,000 Won in Health Insurance Contributions [Q&A]

- Input

- 2026-05-11 11:24:30

- Updated

- 2026-05-11 11:24:30

[The Financial News] A salaried worker, Mr. A, and his wife are a family of four with two elementary school children. If their combined monthly health insurance contributions total 310,000 won, they will be eligible for the second round of Financial Assistance for Damages Caused by High Fuel Prices. That is because the amount falls below the 320,000 won threshold for a four-person household with salaried insurance coverage. However, even if a household meets the health insurance contribution standard, it cannot receive the payment if its combined property tax base exceeds 1.2 billion won or if its financial income is more than 20 million won.

The government will begin the second round of Financial Assistance for Damages Caused by High Fuel Prices on the 18th, targeting people in the bottom 70 percent of the income distribution. On the 11th, it held a joint briefing at Government Complex Seoul and announced the payment plan and eligibility criteria. This support is determined at the household level, not the individual level. The government will select recipients based on each household's combined amount of health insurance contributions billed in March this year. Long-Term Care Insurance Contributions are excluded.

The exclusion standard for high-asset households is the same as the one used when Livelihood Recovery Consumption Coupons were distributed last year. Households are excluded if their combined property tax base or financial income exceeds a certain level. Below is a Q&A summary of the government's announcement.

— Can my household receive it?

△ Yes, if your household's combined health insurance contributions billed in March this year are below the government's standard. Health insurance contributions are calculated on the basis of the household total, not each individual. Long-Term Care Insurance Contributions are excluded. The government selected about 36 million people, or 70 percent of the population, as recipients after forming households based on resident registration records as of March 30, 2026. However, even if a household meets the health insurance contribution standard, it will be excluded if it falls under the high-asset household criteria.

— How much can a family of four pay in health insurance contributions?

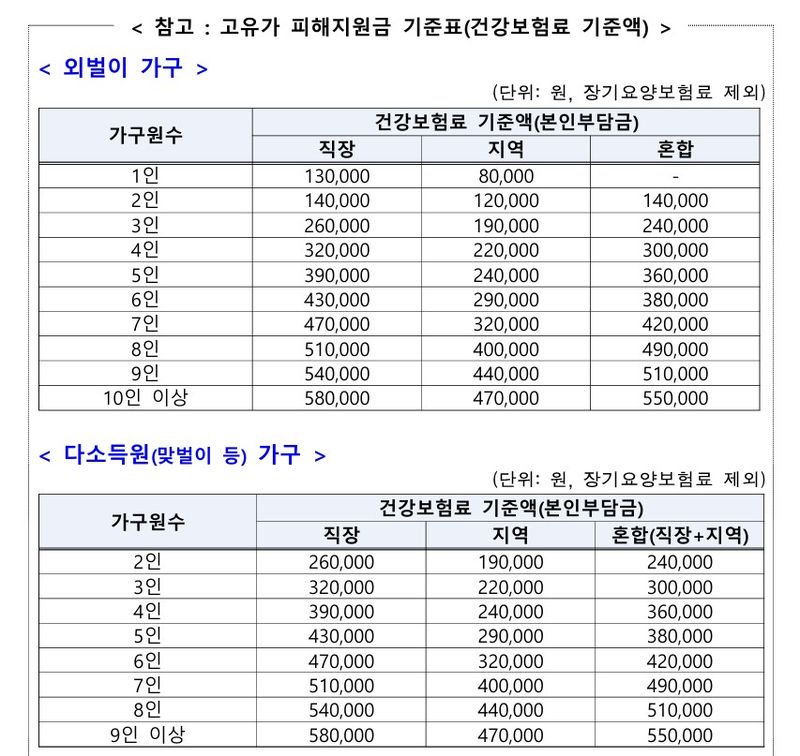

△ For a family of four with a single-income salaried insurance holder, the household is eligible if the combined monthly health insurance contributions are 320,000 won or less. The thresholds for single-income salaried insurance holders are 130,000 won or less for one-person households, 140,000 won or less for two-person households, 260,000 won or less for three-person households, 320,000 won or less for four-person households, 390,000 won or less for five-person households, and 430,000 won or less for six-person households.

For regional insurance holders, the threshold is 220,000 won or less for a four-person household, while mixed households with both salaried and regional insurance holders are subject to a limit of 300,000 won or less.

— How are dual-income couples calculated?

△ For multi-income households with several members engaged in income-generating work, such as dual-income families, the standard of "household members + 1" is applied. For example, a four-person household with two salaried insurance holders is eligible not under the standard four-person threshold of 320,000 won, but under the five-person threshold of 390,000 won or less. The government said it took into account the fact that dual-income households could be relatively disadvantaged under a simple combined-contribution standard. Dual-income couples with different registered addresses are generally considered separate households, but if applying the combined contributions of both spouses is more favorable, they may be recognized as the same household.

— If parents live separately, are they considered part of the same household?

△ In principle, people listed together in the resident registration record as of March 30, 2026 are considered the same household. Even if they have different addresses, a spouse and children who are dependents under health insurance are regarded as part of the same economic unit and included in the same household. By contrast, parents and siblings with different addresses are classified as separate households, even if they are dependents.

— What if a household has a lot of real estate or financial assets?

△ That may be the case. Households will be excluded if their combined 2025 property tax base exceeds 1.2 billion won or if their combined financial income for 2024 exceeds 20 million won. If a household falls under these criteria, no member of the household can receive the payment. The government estimates that about 937,000 households, or 2.5 million people, will be excluded. A property tax base of 1.2 billion won corresponds to a publicly assessed home value of about 2.67 billion won for a single-home owner. Financial income of 20 million won is roughly equivalent to bank deposits of about 1 billion won at an annual interest rate of 2 percent.

— Are there age-based criteria for young people or older adults?

△ No separate age criteria apply. Eligibility is determined by health insurance contributions, household composition, whether the household is a high-asset household, and the region of residence, rather than by special preferences for young people, older adults, or family size.

— How much can people receive?

△ The amount varies by region of residence. The Seoul metropolitan area will receive 100,000 won per person, non-metropolitan areas 150,000 won, depopulation regions designated for preferential support 200,000 won, and special support areas 250,000 won.

A family of four in the Seoul metropolitan area can receive up to 400,000 won, a family of four in non-metropolitan areas up to 600,000 won, and a family of four in a special support area up to 1 million won.

— When can people apply?

△ The application period runs from the 18th through 6 p.m. on July 3. Applications can be submitted online or offline. During the first week of implementation, a weekday system will be applied based on the last digit of the applicant's birth year. Credit and debit card applicants can apply through card company websites, apps, call centers, ARS systems, or bank branches. Applications for Local Love Gift Certificates and prepaid cards will be handled according to guidance from each local government.

— How long can the funds be used?

△ The support funds must be used by August 31. The government urged recipients to use the funds within the period, as any remaining balance will be restricted after the deadline.

— Can people be re-screened if they lose a job, close a business, give birth, or divorce?

△ Yes. If family relations changed after March 30 due to marriage, birth, divorce, or death, or if income fell because of job loss or business closure and health insurance contributions need to be adjusted, an objection can be filed. Applications can be submitted online through e-People or in person at the administrative welfare center in the applicant's town, township, or neighborhood office. Submitted objections will be reviewed by local governments and NHIS.

— Where can people check their health insurance contributions and property standards?

△ Health insurance contributions can be checked on the NHIS website, app, or customer center. The property tax base can be confirmed through Wetax and the Smart Wetax app, while financial income can be checked on Hometax. General questions about applications and payments can be directed to National Government Call Center 110 and the Dedicated Call Center for the High Oil Price Damage Support Fund.

spring@fnnews.com Lee Bo-mi Reporter