When Will the Path Open for Corporate Virtual Asset Investment? Regulatory Uncertainty Creates a Double Burden [Crypto Briefing]

- Input

- 2026-05-19 16:08:38

- Updated

- 2026-05-19 16:08:38

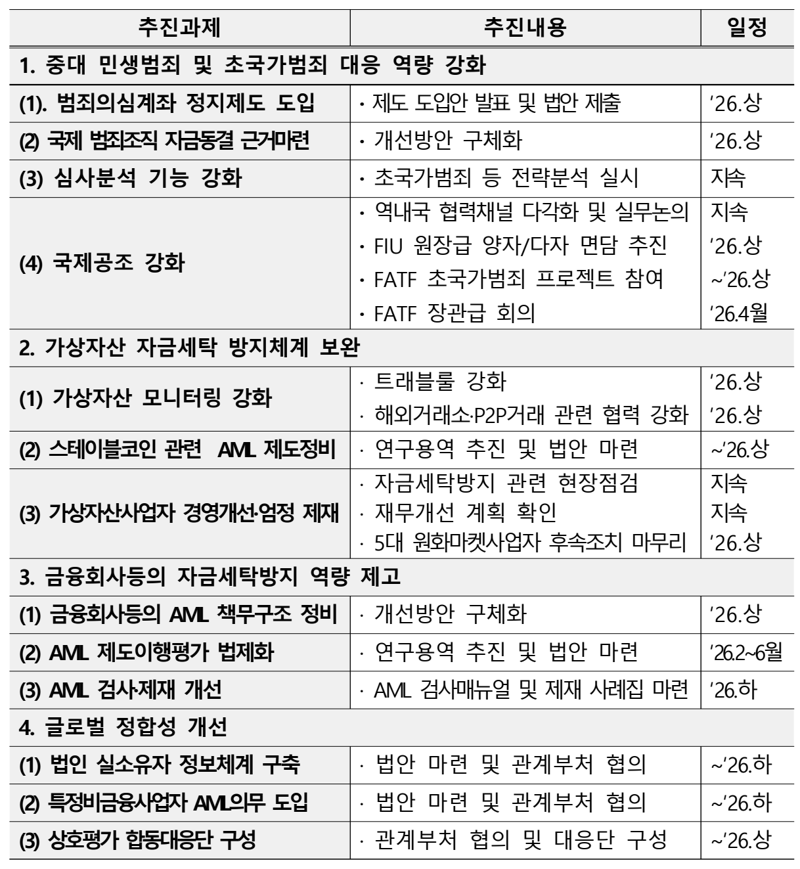

[The Financial News] Financial authorities have begun on-site inspections related to Phase 2 of the Financial Services Commission's Roadmap for Corporate Participation in the Virtual Asset Market, which would allow listed companies, excluding financial firms, and Professional investment corporations to invest in Virtual Asset. However, as the Phase 2 roadmap, which had been expected to take effect in the second half of last year, remains in limbo, uncertainty in the industry is deepening after recently proposed revisions to the enforcement decree of the Act on Reporting and Using Specified Financial Transaction Information emerged as a new regulatory variable.

According to financial authorities and industry sources on the 19th, the Financial Intelligence Unit (FIU) is reviewing the Customer Identification and suspicious transaction report (STR) systems of the five KRW Market exchanges through the Digital Asset eXchange Alliance (DAXA). It was also reported that a closed-door meeting was held the same day at Government Complex Seoul with representatives from the KRW Market to discuss the proposed revision to the enforcement decree of the Act on Reporting and Using Specified Financial Transaction Information.

Earlier, the FSC allowed non-profit corporations and others to sell Virtual Asset for cash conversion purposes under Phase 1 last June. Phase 2 would allow listed companies and Professional investment corporations to receive real-name accounts and trade Virtual Asset for investment and treasury purposes, but the detailed criteria and timeline have yet to be set.

The FIU is reviewing guidelines for KRW Market operators, including stronger bank verification of the source of corporate funds, recommendations to use independent Virtual Asset custody providers, and expanded investor disclosures. However, no criteria for issuing real-name accounts or specific implementation date have been presented. An industry official said, "The timing may also be tied to discussions on the General Act on Digital Assets, but because corporate investment permission is not a matter regulated by law, it is difficult to pinpoint when it will be implemented."

Market concerns are especially centered on the scale gap with global markets. On Coinbase, a large share of trading volume comes from institutional investors, and the exchange is diversifying its revenue streams through not only Virtual Asset trading fees but also interest income from stablecoin (USD Coin (USDC)) holdings and derivatives operations.

By contrast, domestic exchanges still face major limits on proprietary trading and business expansion, with even under Phase 1 of the roadmap only sales for the purpose of covering operating expenses being allowed. Their revenue structure also depends on trading fees from Virtual Asset such as Bitcoin, making it difficult to narrow the competitiveness gap with global exchanges even if corporate funds flow in.

The Phase 3 roadmap, which would expand participation to general corporations, is also expected to take considerable time, as it is scheduled only after the enactment of the General Act on Digital Assets and the overhaul of foreign exchange and tax regulations. Another industry official said, "The United States has already moved beyond approval of Spot Bitcoin ETF and Spot Ethereum ETF to establish an ecosystem centered on corporations and institutions. In Korea, instead of tying the industry’s hands with new obligations that do not align with global standards, we need to quickly improve the real-name account issuance process for Phase 2 of the corporate roadmap and readjust overly restrictive provisions in the enforcement decree in line with the Risk-Based Approach (RBA)."

While the Phase 2 corporate roadmap remains stalled, revisions to the enforcement decree of the Act on Reporting and Using Specified Financial Transaction Information are moving ahead. Under the revision, from January next year, any transaction of 10 million won or more involving domestic virtual asset service providers such as KRW Market exchanges and foreign virtual asset service providers or non-custodial personal wallets must be automatically reported to the FIU as an STR.

The virtual asset industry and legal circles argue that the revised decree could run counter to the AML purpose of the Act on Reporting and Using Specified Financial Transaction Information. They say the parent law imposes STR obligations on the premise of a "reasonable suspicion of illicit property," and that requiring automatic reporting of all transactions solely on the basis of a 10 million won threshold exceeds the scope delegated by law. There are also concerns that when corporations move Virtual Asset for Asset Allocation and liquidity management, it is difficult to transfer even one Bitcoin worth more than 100 million won in a single transaction, which could lead to fragmented transfers in units of 9.9 million won.

An industry official said, "The United States has already gone beyond approving Spot Bitcoin and Ethereum ETFs and has established a Virtual Asset ecosystem centered on corporations and institutions. Rather than burdening the industry with new obligations that do not match global standards, Korea needs to swiftly improve the real-name account issuance process for Phase 2 of the corporate roadmap and recalibrate overly restrictive provisions in the enforcement decree to align with the Risk-Based Approach (RBA)."

elikim@fnnews.com Kim Mi-hee Reporter