"25,000 Won in Annual Interest, 200,000 Won in Stock Gains in Two Days" Retirees in Their 60s Break Open Deposits and Jump Into Margin Investing [Retiree X’s Plan]

- Input

- 2026-05-16 08:30:00

- Updated

- 2026-05-16 08:30:00

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

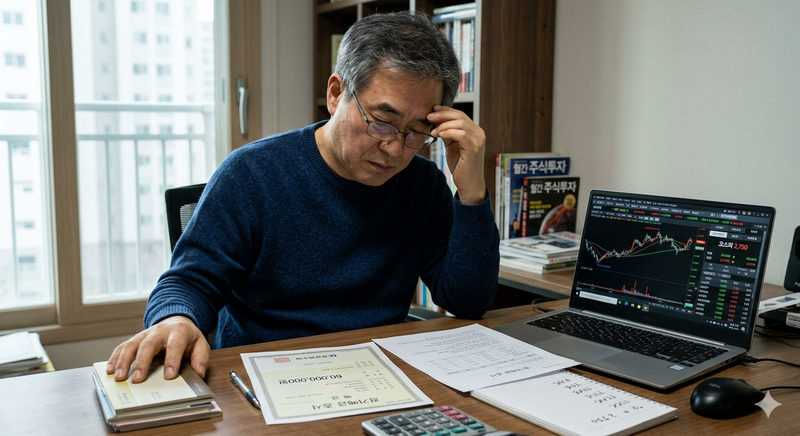

/ AI-generated image by NanoBana to help readers understand the article [Financial News] "A one-year time deposit of 10 million won that I made a year ago has matured. After taxes, the interest came to about 250,000 won.I was really annoyed by how little it was. I decided that wouldn’t be enough, so I bought stocks for the first time.In just two days, I made a 2% return, or 200,000 won. I’m still a stock beginner, but I think I need to pay more attention from now on.I’d appreciate a lot of help from my seniors. " That post recently appeared on a well-known investment community.

Next to the author’s ID was the number “62. ” It marked the moment a retired generation, which had spent its life managing assets mainly through deposits and savings accounts, entered the stock market for the first time.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

The response was enthusiastic. Comments included, “It’s not too late to start now,” “Brother, this market is feeding everyone right now,” and “Try studying leveraged Exchange-Traded Funds (ETFs).

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.The returns are on another level. ” Recommendations poured in, and leveraged ETF suggestions even appeared.

The market has changed, and so have people As the KOSPI broke through the 6,000 and 7,000 levels, which had never been seen before, interest in the stock market has risen rapidly. On the 15th, just seven trading days after crossing 7,000, the index also surpassed 8,000, raising expectations for an era of “10,000-point KOSPI.

” People who once checked preferential deposit rates at bank counters are now opening their Mobile Trading System (MTS) apps and discussing NVIDIA Corporation’s earnings and the premium gap in leveraged ETFs. It is now easy to spot people checking stock prices not only in restaurants but also on the street.

Park Kyung-cheol, 61, a pseudonym, from Nowon District in Seoul, was a typical deposit investor until just this past March. 5 million to 3 million won in monthly cash flow.Park said, "Whether it was a gathering with friends or relatives, all anyone talked about was stocks. Some people said they made 50% on Samsung Electronics and 60% on SK hynix," and added, " The fact that the interest I earned after putting money away for more than 10 years was less than a single day’s price swing for those people kept me up at night." He said. After buying semiconductor stocks in April, Park has made gains of more than 10%.Still, he said, "I’m scared even now. I also wonder whether this is really the right move.I’m trying to keep my goals small and thinking about cashing out. " The problem is that many people jump in without preparation.

This year, 73-year-old Jeon Hae-sook, a pseudonym, recently boasted to her son-in-law, Choi Jeong-ho, 53, a pseudonym, that she had made money in stocks. She bought a stock in the 3,000-won range and made 300,000 won.

When her son-in-law recommended a B stock with solid earnings, priced in the 300,000-won range per share, she رفض? No, must avoid Korean. She rejected it, saying it was too expensive.Valuation indicators such as the price-to-earnings ratio (PER) and price-to-book ratio (PBR) were not even considered. If the stock price was low, it was a cheap stock.If it was high, it was an expensive stock. That was all.

Choi said, "It seems she started investing after talking with people around her," and added, "Even when I give her various pieces of advice, she follows what her friends say more. " It is investing driven by mood rather than analysis.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

That is not a problem when profits are coming in. The difference becomes clear when the market turns volatile.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.They even borrow money The problem is that the enthusiasm does not stay within the bounds of “spare cash. 4376 trillion won as of April this year.

7 trillion won a year earlier. The increase among those in their 70s and older is especially striking.

Over the same period, their balances rose by more than 140%, marking the steepest upward curve among all age groups. A margin loan is, quite literally, investing with borrowed money.

It is a method of borrowing against stocks at a securities firm to buy even more shares. When stock prices rise, it creates a leverage effect that maximizes returns.

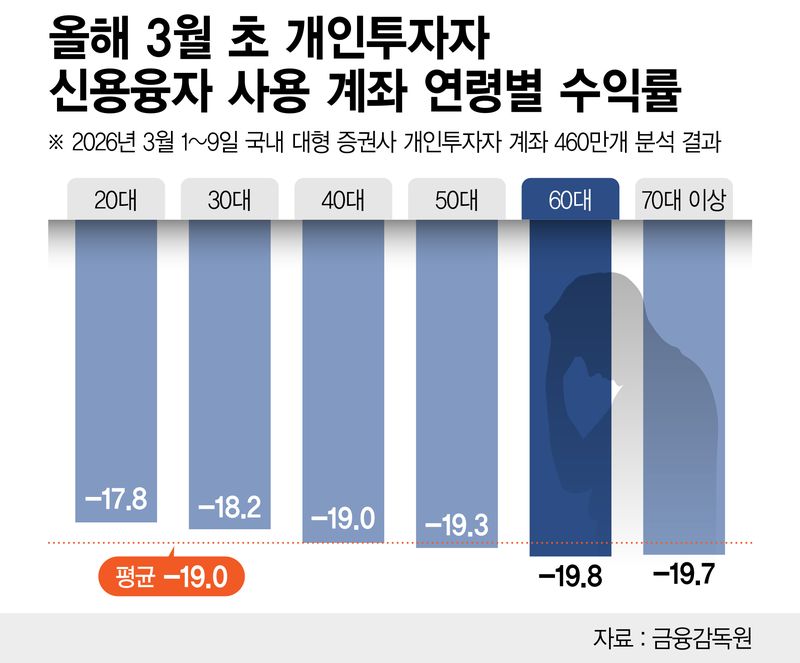

But if the market falls, losses are magnified as well. Most importantly, if the stock price drops below a certain level, the securities firm carries out a forced sale of securities.If losses grow, the risk of eroding principal rises accordingly. Recently, margin trading among retirees has also been increasing rapidly.A warning from the data: investors in their 60s suffer the biggest losses The problem comes when the market turns volatile. If the market is strong, profits are possible.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

But if it turns downward, the losses may become unbearable. 0%.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.2% loss rate for those who invested only with their own capital during the same period. 9%.Returns by individual investor accounts with and without margin loans / Graphic by Reporter Jeong Ki-hyeon What stands out is the age-specific data. 8%, the highest among all age groups.Experts note that older investors who entered the market late during the recent sharp rally may have been hit harder as volatility increased. One retirement expert explained this as a matter of “investment time.

” He said, "Younger generations still have time to make up for losses with earned income, but retirees feel the impact of losses on their lives immediately," and added, "Impatience clouds judgment and eventually leads to a vicious cycle of excessive margin investing. " Losses that could have been avoided if it had been my own money That structure was laid bare in March.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

804 trillion won.06%, or 698 points, in a single day.It was the biggest drop since the KOSPI launched in 1980.

The combined decline over March 3 and 4 reached about 20%.Forced sales are usually carried out two trading days after a sharp drop.On March 5 and 6, the amount of forced sales surged 245% from the previous period.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

Some securities firms also suspended margin trading.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.Korea Investment & Securities temporarily halted new margin purchases starting March 4, and NH Investment & Securities did so from March 5.It was the moment when people who did not want to lock in losses were forced out of the market.What happened after that was the problem.

6%, from its low, later breaking through 7,000 and even coming close to 8,000 on the 12th.

The problem was that they had already been pushed out of the market before the rebound.

Leverage gave investors no time to wait.

2% loss rate for those who invested only with their own capital during the same period. 9%."How much to protect" matters more than "how much to earn" It is true that retirement is difficult to sustain with deposits alone.In an environment of interest rates in the 3% range and inflation in the 2% range, deposits are barely enough to preserve asset value.The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

But the story changes if the investment is made with borrowed money, in a market that has already risen sharply, using leverage products for the first time.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.2% loss rate for those who invested only with their own capital during the same period. 9%.One securities industry official said, "There is a limit to relying on deposits alone when preparing for retirement," and warned, "But margin investing by retirees is also a problem.If a small return is pursued through excessive risk and things go wrong, the entire retirement period could be put in danger.

" Kim Jin-woong, a research fellow at NH Investment & Securities 100-Year Life Research Institute, advised, "The basic rule of investing is to do it with spare cash." He added, "After retirement, 3 to 5 years’ worth of living expenses should be managed in safe assets, and only the remaining funds should be invested." He continued, "The stock market is surging, so impatience may set in, but if you set a sufficient investment horizon, opportunities come more often than you think." He also said, "Rather than rushing in, it is better to begin investing in earnest after the market has corrected to some extent.

" A bull market may look like an opportunity to everyone.

But in investing after retirement, "how much to protect" can matter more than "how much to earn." The market has swung sharply and then recovered quickly.In the end, who endured that period, and with what kind of money, determined the success or failure of retirement.The old formula that “retirement means exit” is breaking down.The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.

In an era when life expectancy reaches 83, Generation X is entering full-scale retirement, and the very concept of retirement is being redefined.The story of their “second act” [Retiree X’s Plan] will meet readers every Saturday morning.If you subscribe to the reporter page, you can receive it conveniently.

The KOSPI, which seemed destined to keep rising, plunged more than 6% as soon as it hit 8,000. Experts warn that while retirement cannot be secured through deposits alone, increasing the share of stock investments too much can put old age at risk.[email protected] Kim Gi-seok Reporter