A man in his 50s who came for counseling with his daughter: "I plan to work until 70... Will I be prepared for retirement?" [Finance Q&A]

- Input

- 2026-05-03 05:00:00

- Updated

- 2026-05-03 05:00:00

[The Financial News] A man in his 50s, identified as A, visited a financial consultation service with his adult daughter, who lives independently and works full time. She wanted advice on her mother A's retirement preparation as she lives alone. A, who works as a fixed-term employee, says she is usually in good health and often tells her daughter, "I can work until I am 70." But her daughter is deeply worried about her mother. With the expected monthly National Pension Service (NPS) benefit at only about 510,000 won, she wants to know how much more money will be needed for retirement. She is also unsure whether she should buy insurance for her mother and how much extra cash should be set aside in case of illness. A currently lives in a jeonse home and is set to move into public rental housing next month. She is also wondering whether paying additional rental deposit would be worthwhile.

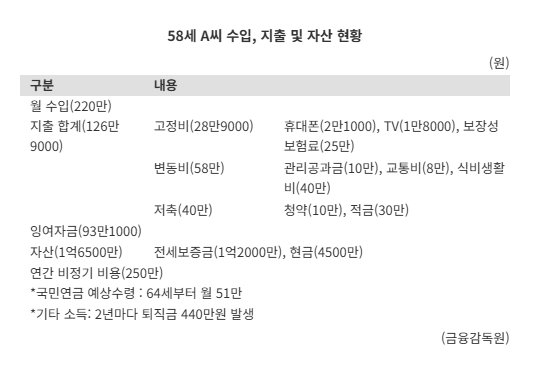

A, 58, has a monthly income of 2.2 million won. There is no irregular annual income. Monthly spending comes to 1,269,000 won. Fixed expenses total 289,000 won, including mobile phone bills of 21,000 won, TV fees of 18,000 won and protection insurance premiums of 250,000 won. Variable expenses amount to 580,000 won, including maintenance and utility fees of 100,000 won, transportation costs of 80,000 won and food and living expenses of 400,000 won. She saves 400,000 won a month, including 100,000 won for a housing subscription account and 300,000 won in installment savings. Annual expenses stand at 2.5 million won. Her assets total 165 million won, including a jeonse deposit of 120 million won and 45 million won in cash. She has no debt. As a fixed-term worker, she receives a severance payment of 4.4 million won every two years. She is expected to start receiving 510,000 won a month from the National Pension Service (NPS) at age 64.

According to the Financial Supervisory Service (FSS) on the 3rd, more children have recently been booking and visiting its financial advisory service together with their parents to seek retirement planning consultations for them. The agency said asset management should be carried out in a way that allows both parents and children to respect each other's lives and take responsibility for their own futures.

In its consultation, the FSS estimated that A's retirement living expenses would be 1.48 million won a month, below the average, because she is a frugal spender. Since her current job allows her to work until age 70, she could continue saving for about 12 more years. With her move to rental housing approaching, there is no longer a need to prepare for a higher jeonse deposit, and she may also be able to liquidate and use her jeonse deposit.

The amount needed at retirement is calculated as follows. If the expected retirement period of 20 years is multiplied by monthly retirement living expenses of 1.48 million won, and 100 million won is added for necessary liquid assets such as medical costs, the total required amount is projected at 455.2 million won. If she receives 510,000 won a month from the NPS starting at age 64, or 159.12 million won in total, she would face a shortfall of 296.08 million won.

However, if A works steadily until age 70, she is expected to be able to cover the gap. Her current assets amount to a little over 135 million won. Assuming she works for another 12 years until age 70, she could accumulate 188 million won by retirement by combining her annual savings capacity of 13.47 million won with 2.2 million won in annual severance pay.

Still, the FSS advised that A should build more pension assets, as she currently holds only cash assets. It stressed that because A is a fixed-term worker, her severance pay is settled every two years, and if she receives that money through an Individual Retirement Pension (IRP) account, she can reduce retirement income tax. Even if the funds are invested in a time deposit within a pension account, the returns are taxed at the pension income tax rate of 3.3% to 5.5%, rather than the 15.4% interest income tax.

She should also review her protection insurance. If she needs substantial medical expenses in the future due to health problems, she needs to check in advance what coverage her current protection insurance can provide. Knowing whether essential coverage is in place would help her daughter consider additional insurance later if more medical costs need to be prepared for.

If A suddenly becomes unable to work after age 65, the Basic Pension could also be an option. This year, the maximum Basic Pension for a single elderly household is 349,700 won a month.

For the rental deposit, however, paying more appears to be the better choice. An FSS official said, "If you pay additional rental deposit, the monthly rent goes down. When converted into an annual return, that benefit is higher than the interest rate on current cash deposits, so paying more is advantageous."

You can receive free, customized financial consumer counseling by entering the FINE financial consumer portal into an internet search engine or by calling the Financial Supervisory Service Call Center 1332 and selecting option 7 for financial advisory services.

nodelay@fnnews.com Park Ji-yeon Reporter