Hanwha Group: Defense and Shipbuilding Are Profitable, So Why Is Cash Running Short? [fn Market Watch]

- Input

- 2026-04-18 06:00:00

- Updated

- 2026-04-18 06:00:00

In a report released on the 18th, titled "Hanwha Group: The Need to Manage Cash Flow After Expansion Investment," NICE Credit Rating analyzed that "the earnings power of the defense and shipbuilding divisions is supporting the group's credit profile, but free cash flow (FCF) remains limited due to investment and working capital needs."

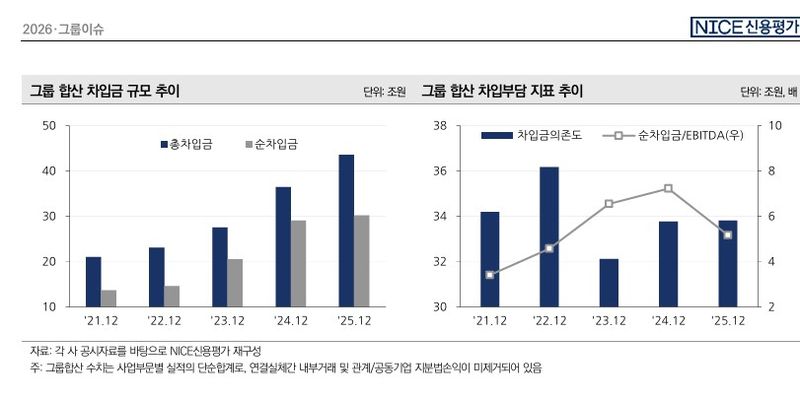

Last year, Hanwha Group's combined revenue reached 64 trillion won, up 13% from a year earlier, and its operating margin improved to 5.1% from 3.6%. At the end of the same year, total debt rose to 44 trillion won and net debt to 30 trillion won. The picture varies sharply by business division. The defense unit saw a sharp improvement in profitability, driven by stronger exports of flagship products such as K9 Thunder and K239 Chunmoo. Hanwha Aerospace's defense order backlog expanded to about 47 trillion won as of the end of 2025, improving earnings visibility.

Shipbuilding has also begun a full recovery, supported by the recognition of high-priced orders and more stable production processes. Hanwha Ocean secured an order backlog of 35 trillion won, about 2.7 times its annual revenue, laying the foundation for medium- to long-term growth.

By contrast, the petrochemical business faces unavoidable restructuring amid prolonged oversupply from China and weak demand. Yeochun NCC is pushing to establish a merged entity with Lotte Chemical while suspending plant operations, and Hanwha TotalEnergies Petrochemical is also discussing production cuts and cooperation measures.

For renewable energy, the key variable is whether Hanwha Solutions' U.S. business can normalize. In 2025, operating rates plunged as customs clearance was delayed under the Uyghur Forced Labor Prevention Act (UFLPA), resulting in an operating loss of 364.8 billion won. Recovery is expected in 2026 as customs clearance normalizes and production systems are established, but initial yields and cost stabilization still need to be confirmed.

The report said, "Hanwha Group is making money, but its cash flow structure is deteriorating."

Over the past three years, the group has recorded a cash shortfall of more than 5 trillion won annually, and it faced a funding gap of about 3 trillion won in 2025 as well. The pressure came from simultaneous investments in a U.S. solar value chain, expanded defense and shipbuilding capacity, and equity investments.

The shortfall was covered through borrowing. As a result, total debt rose to 44 trillion won and net debt to 30 trillion won. In other words, credit quality is being supported by defense while being weighed down by solutions.

Credit ratings also show clear differences by business. Hanwha Solutions and Hanwha TotalEnergies Petrochemical were both assigned AA- ratings with a "Negative" outlook. The ratings reflect the weak petrochemical cycle and uncertainty in the renewable energy business.

By contrast, Hanwha Aerospace (AA/Stable), Hanwha Ocean (A-/Stable), and Hanwha Energy (A+/Stable) all maintained stable outlooks.

NICE Credit Rating said, "The earnings power of the defense and shipbuilding divisions is supporting the group's credit profile, but cash flow pressure is unavoidable during an expansion phase," adding that "the gap between earnings and cash flow will persist for the near to medium term."

It also identified Hanwha Solutions and Hanwha Aerospace as the key affiliates that will determine the group's credit profile going forward. NICE Credit Rating said, "For Hanwha Solutions, the key issue is whether it can improve its financial structure through the normalization of its U.S. business and capital expansion. For Hanwha Aerospace, the main point to watch is financial stability management amid continued investment growth."

khj91@fnnews.com Kim Hyun-jung Reporter