Sell a Home, Make a 2 Billion Won Profit... From 90 Million Won to 360 Million Won, Will Capital Gains Taxes Rise? [Real Estate Atoz]

- Input

- 2026-04-18 14:00:00

- Updated

- 2026-04-18 14:00:00

[The Financial News] Three major bills introduced by lawmakers from the broader pro-ruling camp are drawing attention. They include the Income Tax Act amendment, the Comprehensive Real Estate Holding Tax Act amendment, and the Excess Land Gains Tax Act, which were proposed on the 8th by Yoon Jong-o of the Progressive Party. Their main provisions include abolishing the Special Deduction for Long-term Possession, eliminating the Fair Market Price Rate, and reviving the Excess Land Gains Tax.

1. Income Tax Act amendment - abolition of the Special Deduction for Long-term Possession

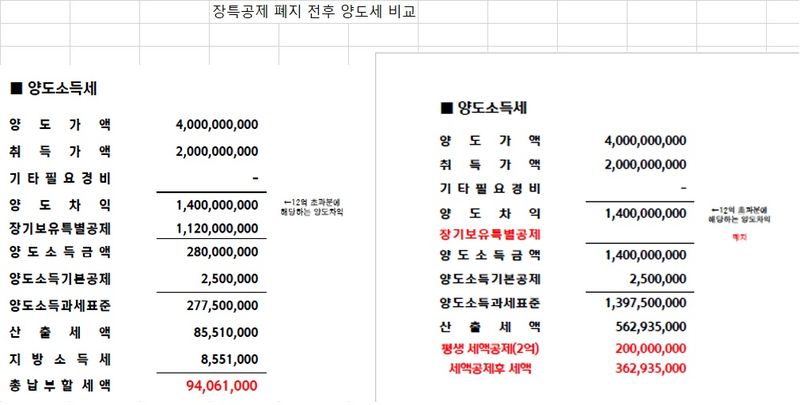

The key point of the Income Tax Act amendment is the abolition of the Special Deduction for Long-term Possession. Under the current system, a single-home owner can avoid capital gains tax on homes valued at up to 1.2 billion won if certain conditions are met. Even for homes worth more than 1.2 billion won, owners can receive a special deduction of up to 80 percent if they hold and live in the property for 10 years, with 40 percent for ownership and 40 percent for residence. This maximum 80 percent deduction has been in place since 2009.

The amendment seeks to abolish that deduction. Lawmakers argue that the deduction has fueled a rush for a single, high-end home in affluent areas such as Gangnam and has contributed to rising home prices. Under the current deduction system, owners of expensive homes pay less tax than multi-home owners. The bill proposes replacing it with a tax credit system that would cap lifetime tax relief at 200 million won per person.

If the Special Deduction for Long-term Possession is abolished and only 200 million won in relief is allowed, the capital gains tax burden on high-end homes would rise. According to an analysis by Woo Byung-tak, an expert committee member at Shinhan Bank's Premier Pathfinder, a single-home owner who bought a property for 2 billion won and sold it for 4 billion won would pay 94 million won in capital gains tax under the current 80 percent deduction. If the deduction is abolished and only 200 million won in relief is applied, that amount would rise to 360 million won.

Woo said, "If the Special Deduction for Long-term Possession is abolished, taxes would fall for homes that are not high-end properties," and added, "However, because of the 200 million won lifetime tax relief cap, the tax burden is likely to increase when additional homes are sold."

2. Comprehensive Real Estate Holding Tax Act amendment - abolition of the Fair Market Price Rate

The Comprehensive Real Estate Holding Tax Act amendment is also drawing attention. The proposed bill focuses on abolishing the Fair Market Price Rate. It also includes restoring the housing tax rate to its pre-tax-cut level and changing the single-home owner deduction requirement to actual residence.

The Fair Market Price Rate is the basis for calculating the tax base for the comprehensive real estate holding tax. The law states that the tax base is determined by multiplying the officially assessed value by a rate set by presidential decree within a range of 60 to 100 percent. At present, the rate for single-home owners is 60 percent.

For example, in the case of a single-home owner with a property officially valued at 2 billion won, the tax base would be 480 million won, calculated by applying 60 percent to the 800 million won remaining after subtracting the 1.2 billion won basic deduction. If the Fair Market Price Rate is abolished and 100 percent is applied, the tax base would rise to 800 million won. The higher the tax base, the higher the tax rate.

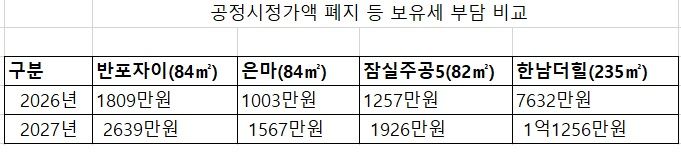

Woo Byung-tak analyzed how much the property tax burden, including the comprehensive real estate holding tax and property tax, would increase if the amendment were implemented as written. The analysis assumes that officially assessed values remain unchanged next year.

For an 84-square-meter unit at Eunma Apartment Complex in Daechi, the annual property tax would rise from 10.03 million won this year to 15.67 million won next year. For an 84-square-meter unit at Banpo Xi, it would increase from 18.09 million won to 26.39 million won, surpassing 20 million won. Even if official values remain frozen, the tax burden is expected to approach the upper limit.

3. Excess Land Gains Tax Act - maximum tax rate of 50 percent

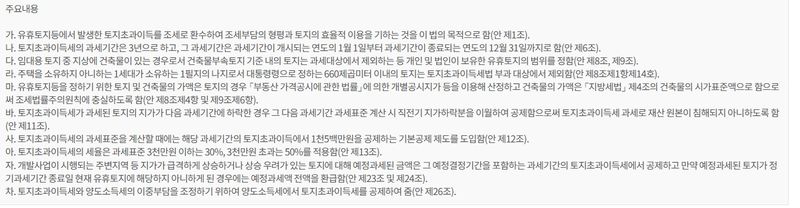

The Excess Land Gains Tax Act is also part of the debate. Its core idea is to investigate the value of idle land every three years and apply a progressive tax rate to the portion of land price gains that exceeds normal land price increases. It is an extension of the public concept of land.

According to the main provisions, the taxation period for the Excess Land Gains Tax would be three years. The key point is to tax excess gains when the price of idle land rises more than the normal land price increase between the start and end dates.

The tax rate would be 30 percent for gains of 30 million won or less and 50 percent for gains above that amount. If capital gains tax arises from the sale of land after the Excess Land Gains Tax has been paid, the previous tax would be deducted. The bill also includes a basic deduction of 15 million won.

One expert said, "Judging from the content of the bills, they do not appear very feasible," and added, "However, since the government and the ruling camp are discussing ways to strengthen capital gains and holding taxes as well as regulations on non-business real estate, there is still room for these measures to be reflected depending on the situation."

ljb@fnnews.com Lee Jong-bae Reporter