Overlapping Listings Above 11% in Korea vs. 0.05% in US to Be Principally Banned from July

- Input

- 2026-04-16 18:09:35

- Updated

- 2026-04-16 18:09:35

On the 16th, the Financial Services Commission and KRX held a "Public Seminar on Improving the Overlapping Listing System" at the Korea Exchange Conference Hall in Yeouido, Seoul. The event served as a forum to design detailed rules for the new framework of principally banning overlapping listings while allowing exceptions, which was announced at last month’s Meeting for Capital Market Stability and Normalization presided over by the president. Individual and institutional investors, the Korea Listed Companies Association (KLCA), securities firms, the Korean Venture Capital Association (KVCA), and experts from academia and the legal community attended. The government and KRX plan to reflect the feedback gathered at this seminar and other channels, draw up draft amendments to KRX rules in April, and give prior notice before implementing the new system as early as July.

In congratulatory remarks, Chairperson of the Financial Services Commission Lee Eog-weon characterized the significance of this reform as "applying the newly introduced fiduciary duty to shareholders to the listing system as well." The Financial Services Commission intends to strictly distinguish between overlapping listings that asymmetrically concentrate listing benefits in the hands of a few and those that are fair to all shareholders and create new value, and to review them accordingly.

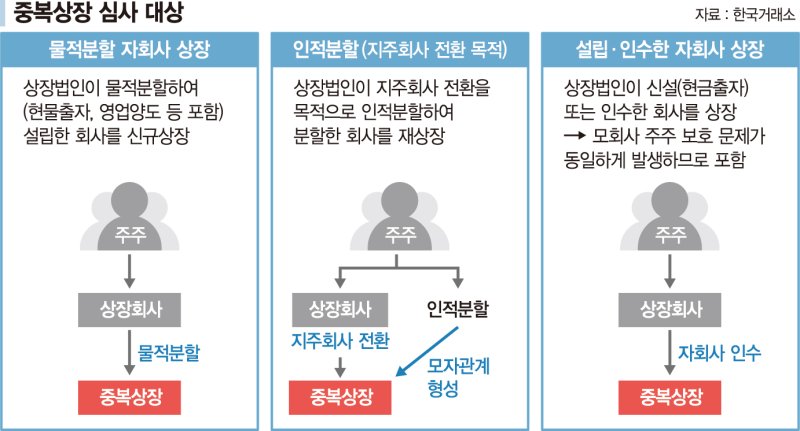

According to the implementation plan disclosed by KRX that day, a special provision on overlapping listings will be newly added to the listing regulations, and three main review criteria will apply: operational independence, managerial independence, and investor protection. If a company fails to meet these criteria, its listing will be denied.

First, operational independence will examine whether a subsidiary’s core business can be conducted independently without relying on the parent company. Key evaluation items include the similarity of main products and major customers, as well as the degree of dependence on the parent for Research and Development (R&D), raw material procurement, and sales. Managerial independence will focus on whether the subsidiary’s decision-making and governance structure are independent. This includes assessing the independence of the board composition, the presence of full-time management, and the extent of the parent company’s involvement in major decisions. Investor protection will review the necessity of listing the subsidiary, efforts to communicate with and protect shareholders, and whether the parent company’s general shareholders have given their consent.

Three types of cases will be subject to review: new listings of companies established through a physical spin-off (in-kind contribution or business transfer) by a listed company; relisting after a spin-off carried out to convert into a holding company structure; and listings of subsidiaries newly established or acquired by a listed company. KRX has made it mandatory for the parent company’s board to assume a fiduciary duty to shareholders, assess how the subsidiary’s listing will affect the parent’s general shareholders, and disclose the results.

However, differences in position among stakeholders emerged at the seminar. Investor representatives argued that overlapping listings serve as a structural cause for expanding the control of controlling shareholders and that this is one of the factors behind the Korea discount. In contrast, corporate representatives expressed concern that if overlapping listings become impossible, more subsidiaries will seek overseas listings, which could weaken the competitiveness of Korea’s capital market. They also countered that if subsidiaries acquired through mergers and acquisitions (M&A) are barred from conducting an Initial Public Offering (IPO) simply because their parent is a listed company, the M&A market could shrink.

Academics and legal experts pointed to conflicts of interest in corporate governance and the risk of distorting the value of control rights. In a presentation, Na Hyun Seung, a professor in the Department of Business Administration at Korea University, argued that overlapping listings deepen conflicts of interest between controlling and minority shareholders and structurally depress the parent company’s share price through channels such as double-counting of earnings and constraints on returning profits from assets. He identified these channels as contributing to the Korea discount. At the same time, he warned that a blanket ban on overlapping listings could dampen investment in capital-intensive new businesses, and therefore stressed the need for policy measures such as allowing exceptions.

elikim@fnnews.com Kim Mi-hee Reporter