The last report under Governor Rhee Chang-yong: "Why the exchange rate jumps even with a surplus"

- Input

- 2026-04-17 06:00:00

- Updated

- 2026-04-17 06:00:00

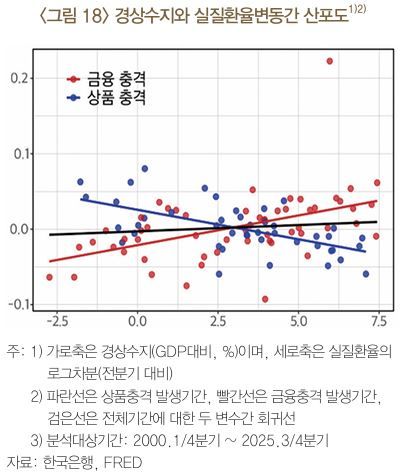

The BOK’s analysis shows that since 2015, "positive financial shocks"—episodes in which capital outflows push the exchange rate higher—have become more important. Comparing the period before 2014 with the period from 2015 to the third quarter of 2025, the frequency of such positive shocks rose from 21.4% to 34.9%, an increase of 13.5 percentage points. By contrast, "negative financial shocks," defined as capital inflows that lead to a lower exchange rate, fell from 35.7% to 18.6%, a drop of 17.1 percentage points.

Korea’s currency also reacts more sensitively than those of other advanced economies. Korea’s regression coefficient was 0.65, while the figures for the United States of America (US) and Japan were about 0.07 and 0.38, respectively. In other words, for the same financial shock, Korea’s currency tends to depreciate more.

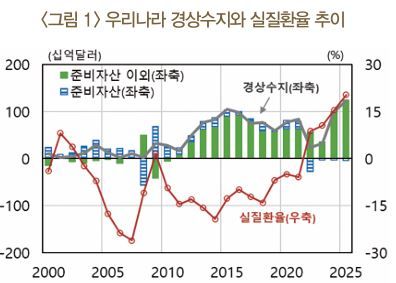

The BOK attributed this pattern to the growing influence of domestic residents on the exchange rate and the expansion of net capital outflows. It judged that this tendency has become even more pronounced since the second quarter of 2023. In fact, despite recording a record current account surplus of 123 billion dollars last year, the exchange rate climbed to 1,480 won per dollar by year-end.

Kim Jihyun, head of the International Finance Research Team in the BOK’s International Department, explained, "As external asset accumulation has increasingly been led by the private sector, capital outflows through the financial account have had a greater impact on the real exchange rate and the current account." She added, "As residents’ preference for overseas assets rises, the exchange rate can move higher, and the resulting relative price adjustments and reduced domestic absorption can in turn generate a current account surplus."

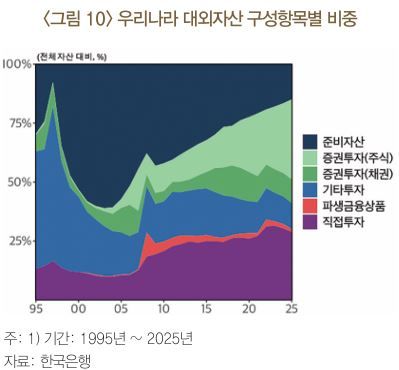

In fact, this composition of external assets is closer to that of advanced economies. Securities investments account for 38.7% of external assets in advanced economies, compared with 15.6% in emerging economies. Korea’s share is 5.4 percentage points higher than the advanced-economy average. As of 2024, 67.7% of Korea’s overseas equity investment was in the US, about 2.3 times the advanced-economy average of 29.5%.

Kim noted, "Compared with the past, non-residents now play a relatively smaller role in foreign exchange market supply and demand, while capital outflows and inflows by the domestic private sector have become more important." She continued, "Financial shocks such as shifts in preferences toward overseas assets trigger capital outflows and depreciation of the domestic currency, and this can widen the current account surplus." She pointed out that this pattern was especially evident during the Global Financial Crisis (GFC) in 2008 and the surge in overseas securities investment in 2025.

She also said, "Since 2000, more than 80% of the fluctuations in the real won–dollar exchange rate can be attributed to financial shocks," adding, "Most of these financial shocks stem not from changes in saving behavior, but from shifts in demand for dollar assets."

taeil0808@fnnews.com Kim Tae-il Reporter