Hanwha Group's Defense and Shipbuilding Businesses Are the Cash Cows, Driving 95% of Operating Profit

- Input

- 2026-04-20 06:59:00

- Updated

- 2026-04-20 06:59:00

[Financial News] Hanwha Group's profit structure is heavily skewed toward defense and shipbuilding. Based on a simple calculation that adds up each business division's results across the group, while excluding internal transactions between consolidated entities and equity-method gains and losses from affiliates and joint ventures, those two businesses account for as much as 95%. Hanwha Solutions, which operates in renewable energy, is expected to recover its earnings power starting this year. That is further bolstering the rationale for its 2.4 trillion won capital increase.

Shipbuilding and defense are keeping Hanwha Group afloat

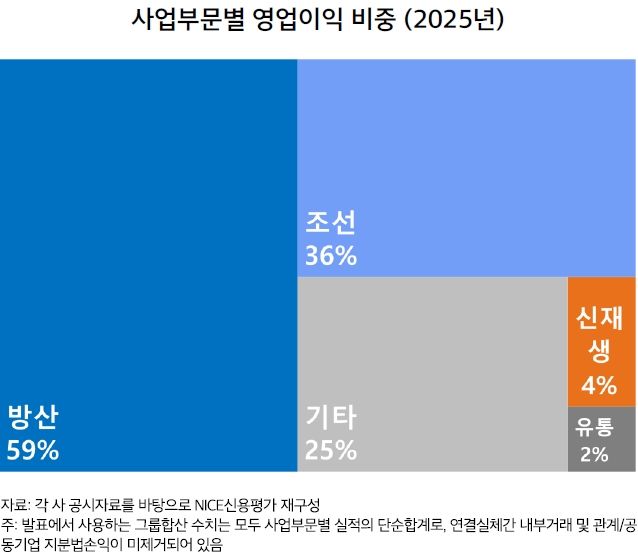

According to the industry on the 20th, NICE Investors Service recently presented Hanwha Group's operating profit mix by business segment for last year through its '2026 First-Half E-Seminar,' with defense at 59% and shipbuilding at 36%. Combined, the two segments accounted for 95% of the total. Renewable energy followed at 4% and distribution at 2%, while petrochemicals dragged operating profit down sharply with a deficit of nearly 1 trillion won.Kim Seo-yeon, senior researcher at NICE Investors Service's Corporate Credit Rating Division, assessed that "since 2023, external growth and earnings expansion centered on defense and shipbuilding have continued, but the group's former core businesses, petrochemicals and renewable energy, have seen deteriorating results since 2022."

The fundamentals of defense and shipbuilding remain solid. Backlog in the shipbuilding and defense segments jumped more than fourfold from 11 trillion won in 2021 to 47 trillion won last year. Hanwha Aerospace surpassed 3 trillion won in operating profit in 2025, setting a new record for the Korean defense industry, while Hanwha Ocean also moved into the black with 12.6884 trillion won in sales and 1.1091 trillion won in operating profit.

Hanwha Ocean is improving profitability as the share of revenue from high-priced orders rises, but it still faces investment and working-capital burdens. Hanwha Aerospace is also expected to post strong operating results amid the prolonged war, but its investment burden remains substantial. That raises concerns about cash generation.

He said, "Given the backlog, shipbuilding and defense are expected to deliver strong earnings power, and EBITDA has remained solid since 2023, but free cash flow generation has not kept pace."

He added, "Despite the expansion in earnings power, cash flow deficits have emerged because of investment funding needs. Since 2021, the group has faced annual cash shortfalls of more than 5 trillion won, and since 2023, the annual funding gap has remained at around 3 trillion won."

The cash shortfall was covered entirely through borrowing. The group's total debt rose to 44 trillion won at the end of last year, more than doubling from 21 trillion won at the end of 2021 and 23 trillion won at the end of 2022. Hanwha Solutions, with net debt of about 12 trillion won, and Hanwha Ocean, with about 5 trillion won, led the increase.

Hanwha Solutions says this year is the turning point, strengthening the case for its 2.4 trillion won rights offering

A notable point is the visibility of Hanwha Solutions' earnings recovery. He explained that "the cell customs clearance issue was resolved at the end of last year, and tighter regulations are creating a premium for non-Chinese products." In the U.S. solar module market, Chinese manufacturers account for 29.2%, while Hanwha Qcells has a 9.8% share, making it a beneficiary of the non-Chinese premium.He forecast that "once the cell plant begins mass production in the second half, a full-fledged competitive environment will be in place." If the integrated production system in the U.S. operates normally, the amount of AMPC receipts is also expected to expand significantly.

According to NICE Investors Service, Hanwha Solutions' quarterly AMPC receipts plunged during the period of cell customs clearance delays, but have since recovered. The company is expected to receive about 950 billion won for the full year.

This earnings recovery outlook strengthens the rationale for the 2.4 trillion won rights offering Hanwha Solutions is pursuing. On March 26, Hanwha Solutions resolved to carry out a rights offering through a shareholder allocation followed by a public offering of unsubscribed shares.

Hanwha Solutions said the move is "a key measure to restore financial stability and secure a foundation for future growth," and set a target of keeping its consolidated debt ratio below 150% and net debt at around 9 trillion won. However, the schedule has been delayed after the FSS on the 9th requested revisions to the securities filing.

From a credit perspective, if the rights offering is completed, Hanwha Solutions' net debt would fall from 12 trillion won to the 9 trillion won range. Combined with an EBITDA recovery, the net debt-to-EBITDA ratio would improve meaningfully. That could play a decisive role in defending against downward pressure on its AA-/Negative rating.

Regarding the current petrochemical restructuring, Kim, the senior researcher, said that "Yeochun NCC is idling its second and third plants and integration with Lotte Chemical is under way." She added that progress in the business restructuring will be a key issue in this year's regular review.

ggg@fnnews.com Kang Gu-gui Reporter