"Blew Up Shorting Tesla, Now This?" Three Fatal Flaws in Michael Burry’s Attack on Palantir [Friday U.S. Stock Column]

- Input

- 2026-04-10 18:00:00

- Updated

- 2026-04-10 18:00:00

According to Financial News, legendary investor Michael Burry, best known as the real-life protagonist of the film "The Big Short," has once again stepped into the spotlight with a sharply critical view.

This time his target is AI-driven data analytics firm Palantir Technologies (PLTR). Pointing to the explosive revenue growth of Anthropic PBC, often described as a key rival to ChatGPT, he argued that Palantir’s market share is being eaten away.

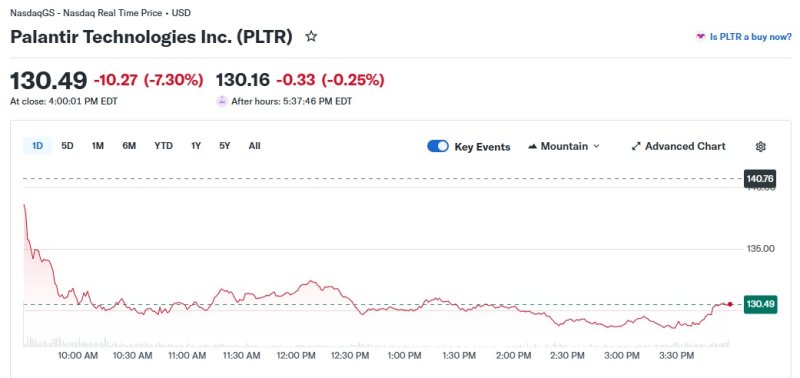

The warning from a heavyweight whose name alone can rattle Wall Street sent Palantir’s share price tumbling. Over just two days, the stock dropped more than 15%, including an 8% plunge on the night of April 9, falling to around 130 dollars. With this backdrop, Korean retail investors in U.S. stocks are understandably anxious as they wait for the market to open.

However, if you strip away the fear triggered by his reputation and focus coolly on business fundamentals and hard facts, it becomes clear that his argument contains obvious gaps that are difficult to accept at face value.

Anthropic PBC’s "Claude" and OpenAI’s "ChatGPT" are, at their core, builders of general-purpose AI "engines"—large language models (LLMs).

By contrast, Palantir’s Palantir Artificial Intelligence Platform (AIP) is more like a "vehicle"—a platform that connects those powerful engines to a company’s vast troves of sensitive internal data and safely orchestrates them toward specific objectives.

Palantir Technologies does not insist on any single AI model. If a client wants to use Anthropic PBC’s Claude, Palantir simply lets them run Claude on top of its platform.

In other words, the stronger Anthropic PBC’s engine becomes and the larger the overall AI market grows, the greater the demand for Palantir’s software that can safely embed and control this vast, untamed AI inside enterprises. The two are not locked in a zero-sum battle; they form a near-perfect symbiotic relationship that enhances each other’s value.

Yet anyone who understands the essence of value investing is likely to raise an eyebrow at this point.

Passing the extreme security requirements of the United States Department of Defense (DoD) or the Central Intelligence Agency (CIA) and becoming embedded as a core operational system creates an enormous barrier to entry that rivals can hardly challenge.

While the initial build-out requires substantial time and cost, once a system is locked in, it becomes virtually impossible to replace—even when administrations change. This functions as the ultimate "economic moat" and a highly reliable cash cow that remains resilient even in times of crisis, which Burry effectively dismisses.

Moreover, the real engine behind Palantir Technologies’ recent performance is not its government segment at all, but its rapidly surging "U.S. commercial (private-sector) business"—a fact that his argument conveniently glosses over.

Looking only at Palantir Technologies’ latest results, announced early this year (February 2026) for the fourth quarter of 2025, Burry’s thesis quickly loses steam. In that quarter, Palantir’s U.S. commercial revenue soared 137% year-on-year to 507 million dollars. The Remaining Deal Value (RDV), which represents the value of future revenue from signed contracts, also jumped 145% from a year earlier, surpassing 4.38 billion dollars.

No matter how impressive Anthropic PBC’s growth may be, claiming that it is "eroding market share" from Palantir Technologies—when Palantir has already delivered growth in the 130% range in the commercial market and smashed Wall Street consensus—is closer to willfully ignoring the numbers than to a fair assessment.

■ The perennial pessimist who surrendered to Tesla’s surgeThere is no denying that Michael Burry is a brilliant macro investor who correctly foresaw the 2008 global financial crisis. At the same time, however, he is also a perennial pessimist who calls for declines even in rising markets.

He famously took a large put-option short position against Tesla, Inc., arguing that Elon Musk’s company was overvalued, only to misjudge the pace of growth of an innovative business and suffer through a massive share-price rally before quietly closing out his position—a misstep well known on Wall Street.

He may be exceptional at spotting bubbles in the broader macro economy, but his track record shows frequent misjudgments when it comes to analyzing the micro-level business models and ecosystems of specific high-growth tech companies.■ Will you sell in fear, or happily buy the dip?

Ultimately, the decision rests with each individual investor. If you are 100% convinced that Michael Burry’s analysis reflects the true state of the market, then the most rational way to protect your portfolio may be to sell your shares now without hesitation.

But if you judge that his claims are merely a misreading of the innovation ecosystem and do not damage the intrinsic value or fundamentals of Palantir Technologies, the picture changes completely.

If the market, spooked by the words of a famous investor, temporarily pushes the stock price down, this loud "noise" can actually create a perfect bargain-sale window to increase your holdings in a company you believe in at the lowest possible price.

It is only the share price that wavers, not the essence of the business. If you firmly trust the "value" of a company you have studied thoroughly, then even a warning from a market legend can turn the current decline into a welcome buying opportunity rather than a source of fear.

jsi@fnnews.com Jeon Sang-il Reporter