Domestic ETFs Fail to Capture Rapidly Changing Iran War Variables, Raising Investment Risk Warnings

- Input

- 2026-04-05 18:45:18

- Updated

- 2026-04-05 18:45:18

Geopolitical risks stemming from the Middle East are intensifying price distortions in domestic Exchange-Traded Funds (ETFs). Cases where the "premium/discount ratio"—the gap between an ETF’s market price and its actual value—exceeds the reference range of 1–2% are surging.

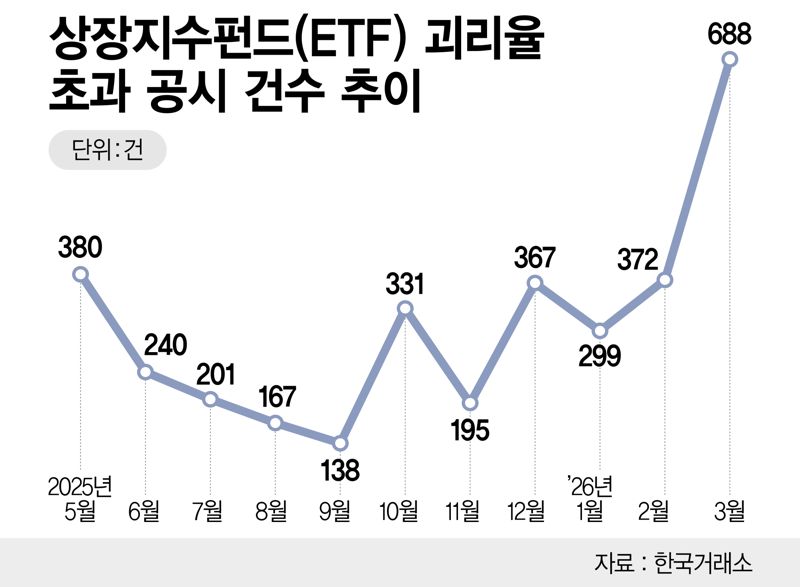

According to the Korea Exchange (KRX) on the 5th, there were 688 disclosures last month of ETFs exceeding the premium/discount threshold, the highest level in 11 months since April last year, when there were 1,060 cases.

In January and February this year, the number of ETF premium/discount excess disclosures stood at 299 and 372, respectively, but in March it jumped to roughly double those levels.

In just the first three trading days of this month, 158 cases have already been reported, bringing the cumulative total for this year to 1,517. That is about 40% of the full‐year figure for last year, which was 3,802.

ETF premium/discount excess disclosures are made based on the ratio calculated as of the previous trading day. The premium/discount ratio refers to the difference between the ETF’s market price and its net asset value per share, which is derived from its underlying assets such as stocks and futures. A positive ratio means the ETF is trading above the value of its underlying assets, while a negative ratio indicates it is trading below that value. When the absolute value of the ratio is low, the ETF price is closely tracking the underlying assets; when it is high, the ETF price is considered distorted.

For ETFs investing in domestic assets, a disclosure is required when the premium/discount ratio exceeds 1%, and for overseas assets, when it surpasses 2%. Under normal conditions, significant premiums or discounts are mainly seen in ETFs whose underlying assets are overseas. Time-zone differences between foreign markets and the Korean stock market, as well as differing price limits, tend to create such gaps. In particular, if there is a large price move in the overseas underlying assets after the Korean market closes, a widening of the premium/discount is inevitable. In these cases, securities company liquidity providers (LPs) usually step in with quotes to help narrow the gap.

Since last month, however, notable premium/discount distortions have also appeared in ETFs that invest domestically. As the Korea Composite Stock Price Index (KOSPI) and KOSDAQ (Korea Securities Dealers Automated Quotations) indices swung in response to the Middle East crisis and a sharp rise in oil prices, ETF prices failed to immediately reflect changes in the value of their underlying assets. Ultimately, the speed at which LPs adjusted prices could not keep up with market volatility, causing the premium/discount ratios to widen. Early last month, for example, the KODEX KOSDAQ 150 ETF, which tracks the KOSDAQ 150 Index, recorded a premium/discount ratio of -1.23%, triggering an excess disclosure.

fair@fnnews.com Reporter Han Young-joon Reporter