"Honey, who stuck a straw in my paycheck account?"... A single-income breadwinner in his 40s and the suffocating bill on the 25th [How Much Is Enough]

- Input

- 2026-04-05 09:00:00

- Updated

- 2026-04-05 09:00:00

[Financial News] On the 25th of every month, an alert reading "Salary deposited" pops up on the smartphone of office worker Mr. A, age 43.

But the sense of relief does not even last half a day. Once the mortgage principal and interest, apartment maintenance fees, allowances for both sets of parents, and the fees for his 7-year-old son's soccer class and study materials are automatically withdrawn, his account is stripped down to bare bones in an instant.

After work, sitting across from his wife at the dinner table, Mr. A forces a wry smile and cracks a joke with a sting in it.

"Honey, did someone install a bottomless jar in my paycheck account? The money doesn’t just pass through—it logs out the moment it logs in."

He meant it as a joke, but a deep shadow briefly crosses both their faces.

This is the suffocating reality of a single-income household in its 40s living in the Republic of Korea (South Korea) in 2026. This weekend, we take apart the chilling household ledgers of single-income breadwinners—books that never seem to balance no matter how much they cut back.

◇ Fact check: Numbers that prove the fall of the single-income household, and the betrayal of real wages

Mr. A’s self-deprecating sigh is no exaggeration. Economic indicators, including the Household Income and Expenditure Survey published by Statistics Korea, lay bare the harsh reality facing single-income households in cold, unforgiving numbers.

Above all, the income gap with dual-income households is painful. According to Statistics Korea, the average monthly income of dual-income households is already about 1.6 times that of single-income households—roughly in the 8 million won range versus the 5 million won range.

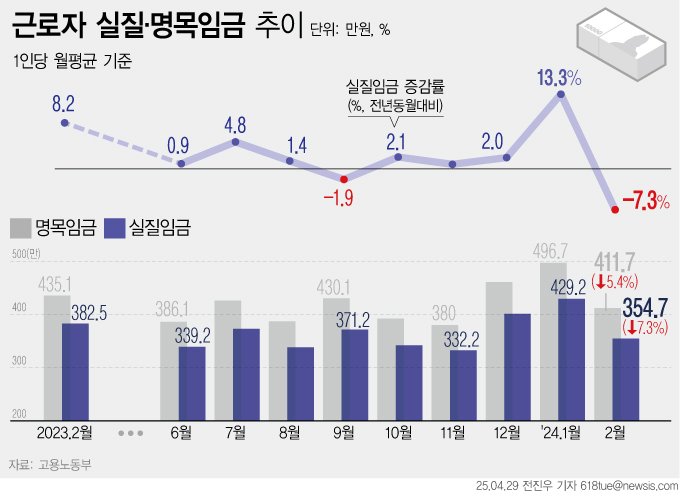

On top of this, high inflation and high interest rates are tightening the noose around single-income breadwinners. Nominal wages have inched up only slightly, but once soaring prices are factored in, workers’ real wages have been flat for months or even shrinking.

To make matters worse, there are too many fixed costs that drain away money before the wallet is even opened.

Taxes, health insurance premiums, and mortgage interest—grouped under so-called "non-consumption expenditures"—have been climbing steeply every year and now hover near 30% of total household spending, an all-time high. In particular, with high interest rates driving double-digit growth in interest costs, disposable income—the money that actually pays for food on the table—has shriveled to the limit.

Unlike dual-income households, where two paychecks can spread out the shock of rising prices and interest rates, single-income households with only one earner are structurally forced to absorb this massive economic blow along their bare spine, with no buffer at all.

◇ The wife's dilemma: "I want to work again too, but..."

Whenever they face this suffocating household ledger, no one feels more frustrated than the wives. Full-time homemaker Ms. B, age 39, also clutches her chest every month as she watches the numbers slide deeper into the red.

"It’s not like I’m staying home because I want to relax. I had my own career, and I gave it all up to focus on raising our 7-year-old. But when I try to go back to work, there’s hardly anywhere willing to hire someone with a career gap, and in reality, a babysitter’s wages cost more than what I’d earn."

Her protest cuts straight to the core of the dilemma facing single-income families in South Korea.

It is not that wives refuse to work. Rather, a lack of social infrastructure and the barrier of career breaks trap them in a structure that effectively forces them out of the labor market, leaving husbands to shoulder the entire financial burden alone.

◇ "Honey, I’ll try to save a bit more on my lunches this month"

Economic experts broadly agree that the current pattern of price increases will not be resolved in the short term.

An official at an economic research institute noted, "Inflation centered on essential consumer goods and public utility charges rapidly erodes the disposable income of single-income households with a weak income base," and added, "The biggest ticking time bomb is that they have virtually no financial buffer to fall back on in an emergency."

Amid this relentless barrage of grim statistics with no clear solution, Mr. A decides to give up the last bit of comfort he had left. He swaps his 10,000-won cafeteria lunches for convenience-store boxed meals and has the worn soles of his old shoes replaced once more instead of buying a new pair.

Caught between his child’s bright soccer uniform and his wife’s weary sighs, the single-income breadwinner in his 40s silently closes the ledger for the 25th yet again.

With no one to blame and nowhere to run, countless men like Mr. A in South Korea brace their bodies against the crushing weight of responsibility—and tomorrow, they will once again squeeze into a packed subway at dawn.

jsi@fnnews.com Jeon Sang-il Reporter