Asian retail virtual asset markets see diverging fortunes under shifting regulations [Crypto Briefing]

- Input

- 2026-04-02 15:57:07

- Updated

- 2026-04-02 15:57:07

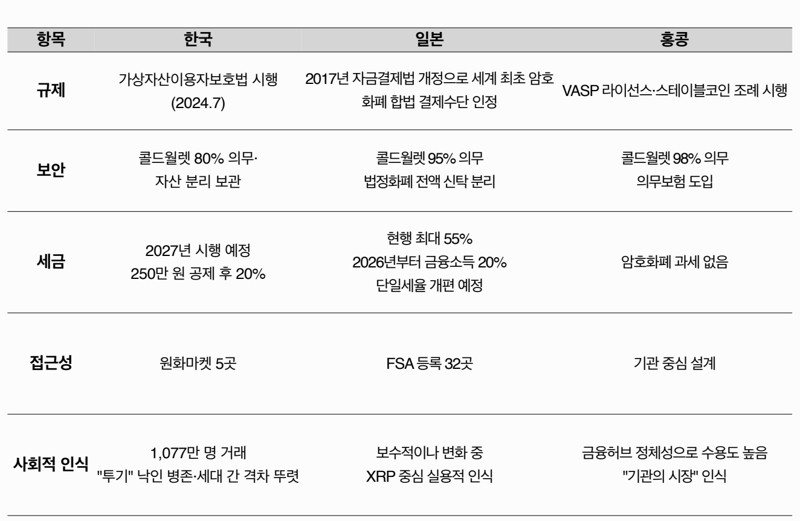

According to Financial News, Asia’s virtual asset market is expanding on the back of growing institutional capital, but the retail segment is showing starkly different dynamics depending on each country’s regulatory environment and incentives. Japan, in particular, is moving this month to overhaul its virtual asset tax regime, cutting the maximum rate from 55% to a flat 20%, while uncertainty still hangs over South Korea’s 22% virtual asset tax, which is set to take effect next year after three postponements.

Web3 research firm Tiger Research Inc. and industry sources said on the 2nd that Japan and Thailand are using tax benefits to draw in individual investors. South Korea, by contrast, is experiencing growing "digital capital flight" despite its globally high trading volumes, due to a lack of product diversity.

Japan is pushing to reclassify virtual assets so they fall under the Financial Instruments and Exchange Act, and to shift them from being treated as miscellaneous income taxed at up to 55% to being taxed as financial income at a flat 20% rate. Based on a joint analysis with HTX (cryptocurrency exchange), Tiger Research Inc. projected that "Japan’s latest tax reform will resolve the cost burden that has long been a stumbling block for the country’s retail market and become a driving force to turn the ‘crypto-curious’ into actual users."

Thailand is also taking an aggressive approach. The Government of Thailand is currently implementing a measure that exempts individuals from income tax on capital gains from trading via licensed exchanges for five years, through 2029. It has also allowed investment token services through securities firm mobile trading applications, blurring the line with traditional finance and greatly enhancing retail accessibility. As a result, trading volume in Thai baht (THB)-denominated stablecoins has grown to become the second largest among nine Asia-Pacific (APAC) markets, following Korean won (KRW)-denominated stablecoins.

South Korea, on the other hand, is facing a paradoxical situation in which quantitative growth and qualitative outflows are occurring at the same time. According to a survey of virtual asset service providers released by the Financial Intelligence Unit (FIU) under the Financial Services Commission for the second half of last year, the domestic virtual asset market capitalization stood at 87.2 trillion won, down 8% from the first half. Yet the number of users, measured by accounts, rose 3% to 11.13 million.

At the same time, the outflow of South Korea-based virtual asset investors to overseas platforms has become pronounced. In the second half of last year, total external transfers from domestic exchanges reached 107.3 trillion won. Of that, about 90 trillion won—roughly 84%—went to whitelisted overseas exchanges and personal wallets that had completed identity verification. Industry observers say large sums are moving offshore so investors can trade leveraged products and altcoins that are not available on Korean won-based virtual asset exchanges, known as the KRW Market. If, under the revised Income Tax Act taking effect next year, a combined 22% tax—20% in other income tax plus 2% in local income tax—is imposed on virtual asset transfer and lending income above a 2.5 million won exemption, the exodus from the domestic coin market is expected to accelerate further.

Hong Kong also has a solid institutional framework, having become the first in Asia to approve spot Bitcoin and Ethereum exchange-traded funds (ETFs). However, multiple regulatory requirements mean that many of these products are sold primarily to professional investors with at least 8 million Hong Kong dollar (HKD) in assets, leaving retail investors with limited direct access.

A Tiger Research official commented, "As traditional financial institutions in the United States of America (USA) and Hong Kong enter the virtual asset market with products such as spot Bitcoin ETFs, domestic exchanges must prove their unique value proposition." The official added, "The key question is how effectively they can offer virtual asset-native services—such as enhanced access to Decentralized Finance (DeFi)—in localized ways that securities firm apps cannot replicate. That will determine who takes the lead in Asia’s retail market going forward."

elikim@fnnews.com Mi-hee Kim Reporter