No Single Hegemon in Digital Currencies: Hyun-Song Shin’s BOK Also Moves Toward a ‘Multi-Moneyverse’

- Input

- 2026-04-07 07:00:00

- Updated

- 2026-04-07 07:00:00

His remarks are being interpreted as acknowledging the possibility that CBDC and Stablecoins can coexist. Accordingly, if Shin takes office as governor, the BOK is expected to continue pushing ahead with "Project Han-gang" while also formulating policy responses to won-based Stablecoins.

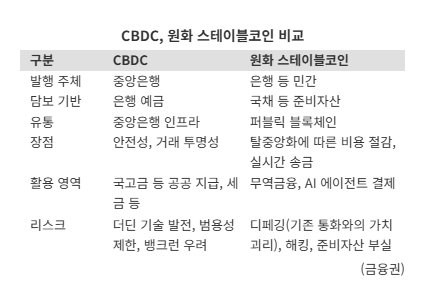

"Project Han-gang" is a scheme in which the Bank of Korea (BOK) issues a wholesale CBDC to financial institutions, and commercial banks then issue deposit tokens based on it for use by ordinary consumers. Because it is anchored in the central bank, it is considered highly safe, but critics say it has limits in terms of general-purpose use. It operates only within the BOK’s infrastructure, which creates constraints for cross-border remittances, and it may also curb technological scalability by restricting participation from non-bank players such as Financial Technology (FinTech) firms and card companies.

Back in August last year, when he was serving as chief economist at the Bank for International Settlements (BIS), Shin stressed the need to introduce a central-bank-centered digital currency platform at the World Congress of Economists, officially the 2025 World Congress of the Econometric Society (ESWC 2025). At the time, he said, "Project Han-gang must proceed without interruption." The BIS is working with central banks around the world to design expanded digital currency infrastructures, including Project Agora.

Even so, Stablecoins are already gaining traction rapidly in global markets, making it difficult to simply rule them out. In particular, in early commercial deployments of Artificial Intelligence (AI)-driven agentic commerce, Stablecoins are emerging as a strong candidate for machine-to-machine (M2M) payment and settlement. In Korea, legislative discussions are under way on the General Act on Digital Assets and related bills, while the United States is maintaining a policy stance that effectively restricts the issuance of a CBDC.

However, experts point out that Stablecoins have structural weaknesses that require a policy response. For example, a one-to-one exchange with legal tender is not always guaranteed. And because they are issued by the private sector on public blockchains, the central bank’s ability to exercise control is inherently limited. They are also relatively vulnerable to security risks such as hacking.

Shin himself has previously warned that Stablecoins could undermine the "singleness of money." The value of a Stablecoin pegged to the dollar could fluctuate from 1 dollar to 0.9 dollars or 1.1 dollars. There are also concerns that rising demand for dollar Stablecoins could serve as a channel for capital outflows.

In practice, major European central banks, including the Bank of England (BoE), are reviewing policy directions that would allow CBDC and Stablecoins to operate in parallel. François Villeroy de Galhau, governor of Banque de France, said at the International Monetary Seminar Conference (IMS Conference) in January, "CBDC is essential, but it cannot cover all use cases in a tokenized economy," adding, "The choice between tokenized bank deposits and private Stablecoins should remain open."

That said, both CBDC and Stablecoins face a common challenge: making themselves useful in everyday payments, namely in the retail finance space. Given that the current payment and settlement systems are functioning smoothly, there is little incentive for users to switch to digital currencies that require a separate transition process.

A source in the financial sector commented, "Shin appears to recognize the innovative potential of Stablecoins, but believes a cautious approach is necessary," adding, "In Korea, the legal foundations for both CBDC and Stablecoins are still insufficient, so the policy direction has yet to be clearly defined."

taeil0808@fnnews.com Kim Tae-il Reporter