Conglomerates, Private Equity, Law Firms, and Retail Investors [Lee Hwan-joo’s View]

- Input

- 2026-03-31 06:00:00

- Updated

- 2026-03-31 06:00:00

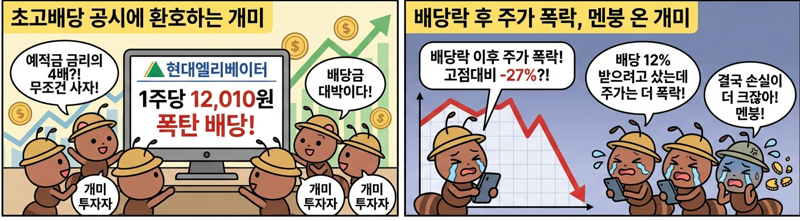

What should I do?" A friend asked me this not long ago. Hyundai Elevator’s share price, which had hit a peak of 113,000 won on February 23, had fallen to around 87,000 won, about 23% below the high.I am hardly a stock market guru myself, so all I could offer was a rather empty consolation: "If you hold on and collect the dividends, maybe the price will go up someday. " On February 10, Hyundai Elevator announced via regulatory filing that it had decided on a cash dividend of 12,010 won per share.1%, up to roughly four times higher than deposit rates of 3–4%. In 2022, the company’s dividend had been only 500 won per share, the recent low.

It then jumped to 4,000 won in 2023 and 5,000 won in 2024 after Hyundai Elevator received damages from a shareholder derivative suit won by Schindler Group. The 12,010-won "windfall dividend" was an unprecedented event made possible by the Schindler damages and the sale of Hyundai Elevator’s headquarters building.

The record date for the dividend was February 28, meaning investors had to hold the shares until February 26 to be entitled to it. This is because, under Korea’s settlement system, trades are actually settled two business days after the buy button is pressed.

On the day of the announcement, Hyundai Elevator closed at 104,100 won. Rumors of a massive dividend had been circulating in the market, and the share price had been rising steadily even before the filing.The stock, which had been in the high 80,000-won range, broke through 100,000 won and then climbed above 110,000 won after the announcement. 4%, savvy investors chose to sell their shares and realize capital gains instead of receiving the dividend.Capital gains on domestic stocks are effectively taxed at zero for most individual investors. In theory, the share price should have dropped starting February 27, the ex-dividend date, when entitlement to the dividend was fixed.But smart money moved earlier, and the price began to fall before the ex-dividend date. From February 24, Hyundai Elevator’s share price plunged by 11,200 won over three trading days, from 111,700 won to 100,500 won.An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

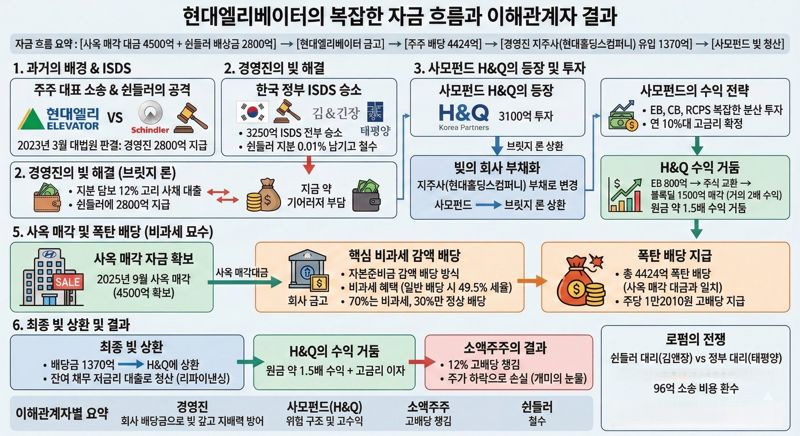

The Supreme Court ordered Hyundai Group executives to pay 280 billion won (170 billion won in principal plus 110 billion won in interest) to Hyundai Elevator. Immediately after the Supreme Court ruling, the executives, who lacked the cash, took out a high-interest bridge loan at 12%, using their Hyundai Elevator shares as collateral, to pay damages to Schindler Group.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.However, the 12% interest burden on the bridge loan quickly became a serious concern. At that point, a private equity fund stepped in.

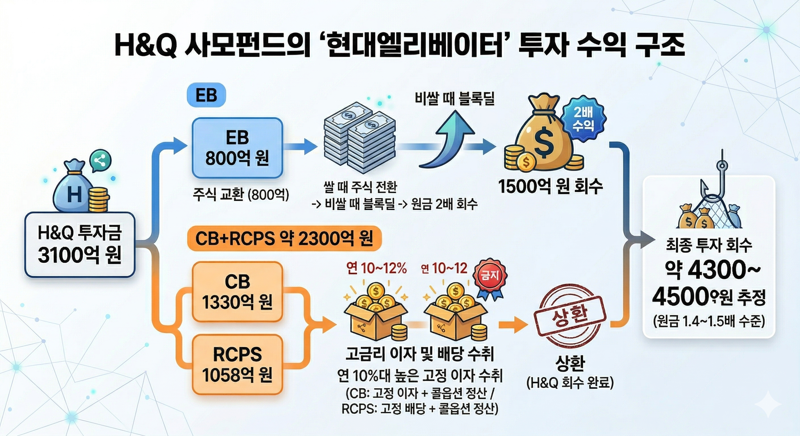

H&Q Korea Partners invested 310 billion won in Hyundai Holdings, the executives’ private company and the group’s de facto holding company. The executives used this money to repay the bridge loan.In effect, the executives’ personal debt was shifted onto the balance sheet of the company, Hyundai Holdings. The flow of funds can be summarized as: private equity fund → bridge loan → Schindler Group.But H&Q Korea Partners, which provided the capital, did not do so out of charity. It split the 310 billion won investment into a complex mix of exchangeable bonds (EB), convertible bonds (CB), and redeemable convertible preferred shares (RCPS).

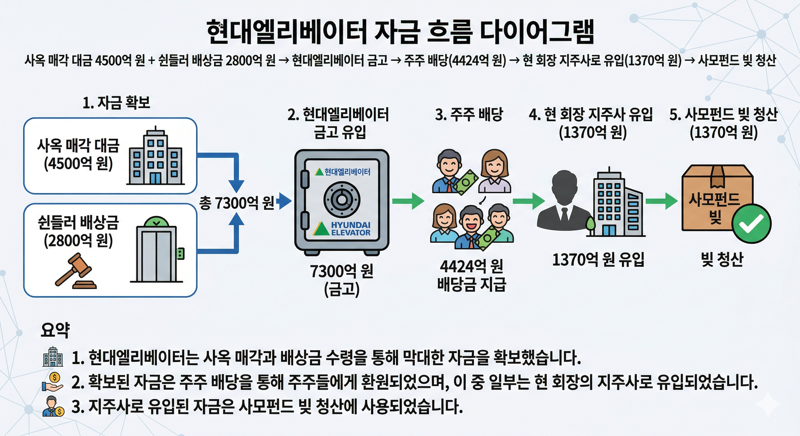

It also locked in a high interest rate in the double digits. H&Q Korea Partners converted 80 billion won of that amount, in the form of exchangeable bonds, into Hyundai Elevator shares and then sold them via a block deal, pocketing 150 billion won.In other words, it converted its loan into shares when they were cheap, sold them when they were expensive, and earned close to double its money on that portion alone. Even after that, Hyundai Holdings, controlled by the executives, still owed H&Q Korea Partners 230 billion won.Gemini-generated image by Reporter Lee Hwan-joo. A private equity fund that profited from a conglomerate battle Swiss elevator company Schindler Group won a shareholder derivative suit against the Hyundai Group management in March 2023.To repay this, Hyundai Elevator decided to sell its Yeonji-dong headquarters building in September 2025 for 450 billion won. Based on this cash, the company paid out the windfall dividend and the executives then used their dividend income to pay down the debt to H&Q Korea Partners.An illustration of how private equity fund H&Q Korea Partners, which played the role of white knight in Hyundai Elevator’s normalization process, realized its profits. Gemini-generated image by Reporter Lee Hwan-joo.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

If the building sale proceeds had been treated as profit and then distributed, tax would have been due, so Hyundai Elevator first tapped its capital reserve to pay shareholders without tax. Put differently, the company filled its coffers with the money from selling the building, then took cash out of another pocket—the one that could be used tax-free—and handed it to shareholders.The major flows of funds can be simplified as follows. 4 billion won in shareholder dividends → 137 billion won flowing into the executives’ holding company → repayment of private equity debt.An illustration of Hyundai Elevator’s building sale, the damages from Schindler Group, the subsequent dividend payments, and the repayment of private equity debt. Gemini-generated image by Reporter Lee Hwan-joo.The link between Schindler Group and the windfall dividend Schindler Group accused the owner family of privatizing the company and launched an attack on Hyundai Elevator, ultimately winning the shareholder derivative suit. Saddled with 280 billion won in damages, the owner borrowed money to reimburse the company.An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

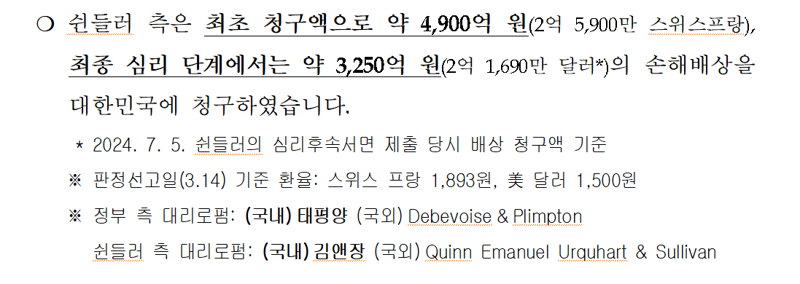

To cover the shortfall needed for the dividend, Hyundai Elevator sold its headquarters building. Separately, Schindler Group also filed an Investor–State Dispute Settlement (ISDS) claim of more than 300 billion won against the Korean government.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.It argued that Korean financial regulators had failed to stop Hyundai Elevator’s management from repeatedly conducting dilutive rights issues that harmed shareholders. Fortunately, the Korean government won a complete victory against Schindler Group in the ISDS merits proceeding.

01% of the shares. The management was able to use the company’s dividends to pay off its own debts and maintain control over the firm.5 times its principal plus hefty interest income by rescuing a troubled conglomerate. Retail investors who recently bought into Hyundai Elevator also benefited from the company being forced, in a sense, to open its vault and pay out a dividend yield of 12%.Yet many small shareholders who held Hyundai Elevator shares suffered losses in the process. When even a global giant like Schindler Group has walked away, the pain of retail investors hardly needs to be spelled out.In a way, the Schindler case may be one scene in which our government is paying, through ISDS claims, the price for having tolerated a backward capital market in the past. Elliott Investment Management’s challenge to the unfair merger at Samsung C&T Corporation and Schindler Group’s protest against Hyundai Group’s dilutive rights issues are examples.Throughout this process, legal experts have been fighting hard to minimize the government’s losses. On the afternoon of the 14th, Minister of Justice Jeong Seong-ho gives a briefing at Government Complex Seoul in Jongno-gu, Seoul, on the ruling in the Investor–State Dispute Settlement (ISDS) case filed by Swiss global elevator company Schindler Group against Korea.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

Schindler Group appointed Kim & Chang as its domestic counsel and Quinn Emanuel Urquhart & Sullivan as its international counsel. The MOJ appointed Bae, Kim & Lee LLC (BKL) as the government’s domestic counsel and Debevoise & Plimpton as its international counsel.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.6 billion won of the government’s litigation expenses. " Screenshot of the MOJ press release.

In other words, Schindler Group spent at least around 11 billion won on legal fees alone for the ISDS case. In the Korean legal market, there is a saying that being number two is more important than being number one.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

In particular, in ISDS cases where foreign companies sue the Korean government, Kim & Chang is often the first firm that global corporations approach. From the perspective of a law firm that puts "the client’s interests" above all else, representing foreign companies in ISDS cases inevitably means taking positions that run counter to the Korean government’s national interest.Back in 2006, attorney Lim Sung-woo of a major law firm publicly criticized Kim & Chang. He argued that "Kim & Chang is not qualified to be a leading law firm," suggesting that it had abandoned legal ethics and behaved more like a group of merchants than a community of legal professionals.Gemini-generated image by Reporter Lee Hwan-joo. A private equity fund that profited from a conglomerate battle Swiss elevator company Schindler Group won a shareholder derivative suit against the Hyundai Group management in March 2023.Kim & Chang responded by filing a petition with the Korean Bar Association (KBA) against Lim, and Lim in turn filed a petition with the KBA against Kim & Chang. Lim claimed that "Kim & Chang has adopted an organizational structure that challenges the very foundations of the Attorney-at-Law Act." Kim & Chang countered that Lim’s remarks amounted to defamation and interference with business. The KBA, acting as mediator, decided to close the case without disciplinary action, effectively choosing not to render a judgment on Kim & Chang’s organizational structure.These details are described in depth in the book "Kim & Chang Law Office" by authors Im Chong-in and Kim Hwa-sik. Lee Joon-ki, managing partner at Bae, Kim & Lee (BKL), which led the government to victory in the Schindler Group case, said, "Following the Lone Star Funds ISDS case, contributing to the management of national risk in this Schindler case once again demonstrates our firm’s ability to respond to complex crises," adding, "We aim to be the first law firm that comes to mind in times of crisis, not only for the government but also for corporations, as the nation’s representative firm." It was a meaningful win against Kim & Chang. A summary illustration of the entire article.

Gemini-generated image by Reporter Lee Hwan-joo.

An illustration showing the complex relationship between Hyundai Elevator’s windfall dividend, retail investors, private equity funds, and an Investor–State Dispute Settlement (ISDS) lawsuit.

In the next installment, we will look at the brutal history of retail investing in the Korean stock market, focusing on dilutive rights issues.

hwlee@fnnews.com Lee Hwan-joo Reporter