Household and unsecured loans are easing, but mortgage rates keep rising

- Input

- 2026-03-27 12:00:00

- Updated

- 2026-03-27 12:00:00

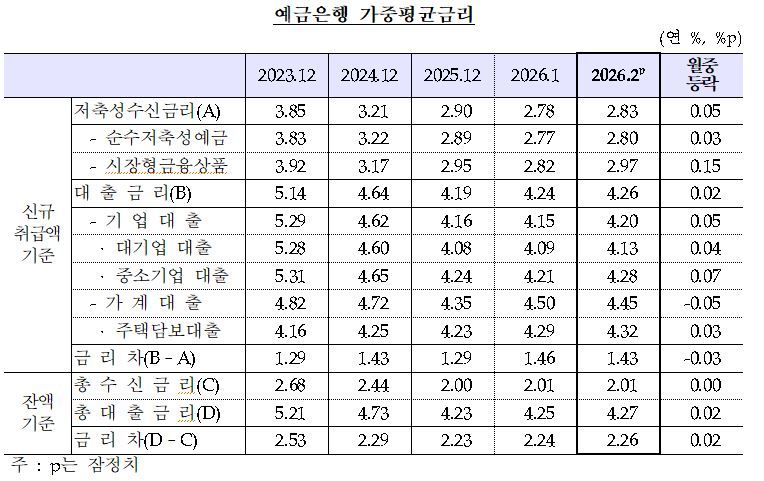

According to the "Weighted Average Interest Rates of Depository Corporations for February 2026" released by the Bank of Korea (BOK) on the 27th, the average interest rate on new household mortgage loans at deposit banks stood at 4.32% per annum in February. This was up 0.03 percentage points from 4.29% a month earlier.

This is the highest level in 2 years and 3 months since December 2023, when the rate was 4.48%. It also marks a fifth consecutive monthly increase since October last year, when the rate was 3.98%.

The rise is seen as a result of higher yields on five-year AAA-rated bank bonds, which serve as a key benchmark rate. The five-year bank bond yield climbed from 3.51% in December last year to 3.58% in January and 3.73% in February, continuing an upward trend.

Fixed mortgage rates rose 0.04 percentage points from 4.26% to 4.30%, while floating rates edged down 0.02 percentage points from 4.40% to 4.38%.

Lee Hye-young, head of the Financial Statistics Team at Economic Statistics Department 1 at the BOK, explained, "Although the five-year bank bond yield increased, the share of general fixed-rate mortgages, which tend to carry relatively higher rates, declined, limiting the overall rise," adding, "Yields on two-year bank bonds, which are the benchmark for fixed rates, went up, but COFIX (Cost of Funds Index), the benchmark for floating rates, fell."

The average interest rate on jeonse deposit loans was unchanged from the previous month at 4.06%. However, this level is still the highest in 11 months since February last year, when it stood at 4.09%. Within the broader category of guaranteed loans, which includes jeonse deposit loans, the average rate fell by 0.13 percentage points. This was attributed to a decrease in higher-rate guaranteed loans for reporters and similar products.

The average rate on general unsecured household loans fell 0.02 percentage points to 5.53%, marking a second straight monthly decline.

Taking mortgages, jeonse deposit loans, unsecured loans and other products together, the overall household loan rate dropped 0.05 percentage points to 4.45%. This was the first decline in five months since October last year, when the rate was 4.24%.

The share of fixed-rate loans in new household lending fell 3.9 percentage points from the previous month to 43.1%. It has been declining for seven consecutive months since August last year, when the share was 62.2%. The proportion of fixed-rate mortgages also dropped 4.4 percentage points to 71.1%, extending a downward streak that began in November last year, when the share was 90.2%.

Corporate loan rates rose from 4.15% to 4.20%, up 0.05 percentage points, as short-term market rates increased. Rates on loans to large corporations climbed 0.04 percentage points from 4.09% to 4.13%, while rates for small and medium-sized enterprises rose 0.07 percentage points from 4.21% to 4.28%.

The interest margin between new loans and deposits at deposit banks narrowed by 0.03 percentage points, from 1.46% to 1.43%.

The average rate on savings-type deposits in February was 2.83% per annum, up 0.05 percentage points from a month earlier. However, rates on pure savings deposits such as time deposits, as well as on market-based instruments like financial debentures and certificates of deposit (CDs), fell by 0.03 percentage points and 0.15 percentage points, respectively.

Based on end-February balances, the overall deposit rate was 2.01% per annum, unchanged from the end of the previous month. The overall loan rate stood at 4.27%, up 0.02 percentage points over the same period. The gap between the two widened by 0.02 percentage points to 2.26 percentage points.

Among non-bank financial institutions, deposit rates on one-year time deposits and installment savings products rose by 0.05 percentage points at mutual savings banks, 0.10 percentage points at credit unions, 0.02 percentage points at mutual finance cooperatives, and 0.10 percentage points at the Korean Federation of Community Credit Cooperatives. For lending rates, all of these institutions saw increases—0.14 percentage points at mutual savings banks, 0.03 percentage points at mutual finance cooperatives, and 0.05 percentage points at the Korean Federation of Community Credit Cooperatives—except credit unions, where rates edged down 0.01 percentage points.

taeil0808@fnnews.com Kim Tae-il Reporter