Double inverse ETFs hit record lows, retail investors take a hit but keep buying

- Input

- 2026-03-22 18:32:15

- Updated

- 2026-03-22 18:32:15

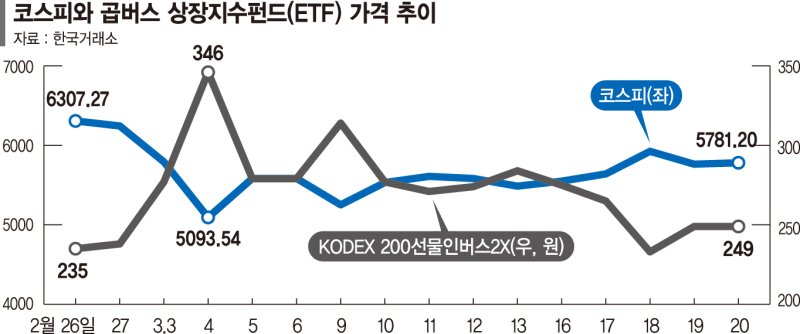

According to the Korea Exchange on the 22nd, KODEX 200 Futures Inverse 2X closed at 233 won on the 18th, marking its lowest closing price ever. Mirae Asset TIGER 200 Futures Inverse 2X ETF at 246 won, RISE 200 Futures Inverse 2X ETF at 237 won, and PLUS KOSPI 200 Futures Inverse 2X ETF at 483 won also set record lows on the same day. These Exchange-Traded Funds (ETF) are double inverse leveraged ETFs that deliver twice the daily decline of the KOSPI 200 Index Futures. Since April last year, the KOSPI has risen sharply, and these products have been stuck in a downtrend for about a year, but investor interest has flared up again since late last month as geopolitical risks in the Middle East emerged.

However, as these products continue to set new lows, some are arguing that double inverse leveraged ETFs are effectively doomed to lose money. The previous record lows for these ETFs were set on the 26th of last month, when the KOSPI closed at an all-time high of 6,307.27. When the ETFs hit fresh lows again on the 18th of this month, the KOSPI stood at 5,925.03, roughly 400 points below its peak. In other words, even though the index has not revisited its record high and has not even recovered the 6,000 level, the double inverse leveraged ETFs have fallen to new lows. According to NH Investment & Securities, as of the 18th, 15,832 of its clients held KODEX 200 Futures Inverse 2X, and 99.99% of them were sitting on losses. Their average return was minus 56.19%.

The main reason double inverse leveraged ETFs struggle to generate positive returns in a sideways market is the so-called negative compounding effect. The Korea Capital Market Institute explains that if the underlying index rises 10% one day and falls 9% the next, the cumulative return of the index is still +0.1%, but the double inverse leveraged ETF would show a return of -5.6%. The index edges up slightly, yet the ETF ends up with a significant negative return.

There are also hidden trading costs embedded in these products. As the price of a double inverse leveraged ETF falls, the bid-ask spread widens, pushing up transaction costs. The minimum tick size for an ETF is 1 won. When the ETF price drops sharply, even a 1-won move represents a large percentage change, which can widen the gap with its actual Net Asset Value (NAV). Since most double inverse leveraged ETFs now trade at penny-stock levels, trading has become highly inefficient.

Kwon Min-kyeong, a research fellow at the Korea Capital Market Institute, noted, "The negative compounding effect can be particularly pronounced in leveraged and inverse products," adding, "Investors who trade frequently need to recognize that valuation losses and trading costs can end up being much larger than they initially expected."

Even so, retail investors’ enthusiasm for double inverse leveraged ETFs shows no sign of cooling. Since the start of this month, the five major double inverse leveraged ETFs have generated a combined trading value of 20.6893 trillion won. KODEX 200 Futures Inverse 2X alone accounted for 20.3864 trillion won in turnover, ranking third in trading volume among 1,072 ETFs. Individual investors are responsible for about half of all trading in these products. Their purchases of KODEX 200 Futures Inverse 2X totaled 9.8483 trillion won, nearly half of the ETF’s overall trading value of 20.3864 trillion won. A source in the financial investment industry pointed out, "During the COVID-19 pandemic, when markets were extremely volatile, many late-arriving retail investors piled into these products out of Fear of Missing Out (FOMO), hoping to make quick gains, but most ended up with losses," adding, "These instruments are designed for short-term trading, and the longer you hold them, the harder it becomes to generate positive returns."

fair@fnnews.com Reporter Han Young-jun Reporter