Full-time Homemaker in Her 50s: "No Income but Need to Prepare for Retirement... How Should I Use a Pension Account?" [Tax and Investment Q&A]

- Input

- 2026-03-22 05:00:00

- Updated

- 2026-03-22 05:00:00

[Financial News] Ms. A, a full-time homemaker in her 50s, currently has no wage or business income. She had long put off preparing for retirement, but recently decided she could not delay it any longer and started looking for information. Office workers commonly use pension accounts to receive year-end tax credits, and she wondered whether someone without earned income could also use a pension account to enjoy tax benefits, which led her to seek tax advice.

According to KB Securities, as of the 22nd, the pension account tax credit is a system that can be applied to any resident with comprehensive income.

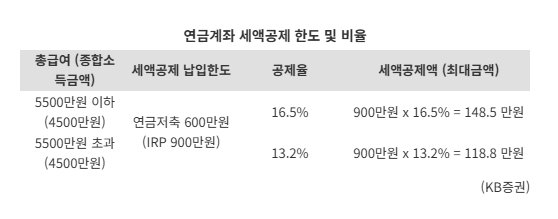

However, there are differences in which pension accounts you can join and in the applicable limits. An Individual Retirement Pension (IRP) is only available to people with wage or business income. With an IRP, you can receive tax credits on contributions of up to 9 million won per year. In contrast, someone like Ms. A, who has no income, must use a retirement pension savings account and can receive tax credits on contributions up to 6 million won per year. The tax credit rate depends on the size of comprehensive income: 16.5% of contributions if comprehensive income is 45 million won or less, and 13.2% if it exceeds that amount.

One important point is that if you only have financial income, then up to around 80 million won of such income may make you subject to comprehensive taxation on financial income, but the final tax due is often fully covered by the withholding tax already paid, leaving no additional tax to pay. In addition, withholding tax on financial income cannot be reduced through pension account tax credits. Only if you have financial income above roughly 80 million won and therefore owe additional tax beyond the withholding amount can you benefit from pension account tax credits.

Go-un Lee, a Tax Specialist Advisor at KB Securities, stressed that a pension account is not a vehicle that is limited only to the tax credit cap of 6 million won (9 million won for an IRP). He said, "You can contribute up to 18 million won per year, and if you roll over funds from an Individual Savings Account (ISA) at maturity, you can contribute the full rollover amount on top of that limit."

Particular attention should be paid to "excess contributions" that do not receive tax credits. The portion of pension account contributions that did not receive a tax credit—the principal—can later be withdrawn tax-free.

In other words, even if someone like Ms. A is currently in a situation where she cannot benefit from tax credits, she can still grow her assets through the pension account’s tax deferral effect. When needed, she can withdraw the principal that did not receive tax credits without any tax burden.

In addition, if you roll over ISA maturity funds into a pension account, you can receive an extra tax credit equal to 10% of the rollover amount, up to a maximum of 3 million won.

Lee emphasized, "If you have surplus funds, it is better not to be fixated on the tax credit cap. Make full use of the 18 million won annual contribution limit and ISA rollover funds to build as large a tax-saving basket as possible."

Using a pension account offers several tax advantages, including tax deferral, offsetting gains and losses within the account, and exclusion from the base for calculating national health insurance premiums.

If you invest in and redeem funds or Exchange-Traded Funds (ETF) in a regular securities account, 15.4% of your gains are withheld as tax, and only the after-tax amount is reinvested.

By contrast, with a pension account, you can reinvest the full pre-tax amount until you finally withdraw or close the account, maximizing the power of compound interest. Also, unlike a regular account where only profitable products are taxed, a pension account aggregates all gains and losses within the account and taxes only the final net gain.

When you receive income from a pension account in the form of annuity payments and the total annual amount exceeds 15 million won, you must choose between comprehensive taxation on the full amount or separate taxation at a flat rate of 16.5%. Lee explained, "At first glance, the 16.5% separate tax rate may look higher than the 15.4% withholding tax rate on financial income, but because it is treated as separate taxation, it is excluded from the base for comprehensive taxation on financial income and the tax obligation ends there. Under current rules, that pension income is also not included in the income base used to calculate national health insurance premiums."

He added that pension accounts tax all investment gains over principal regardless of product type. For this reason, it is more advantageous to hold in a pension account those products that are taxable in a regular account, such as overseas equity ETFs or high-dividend products, rather than domestic equity products whose capital gains are tax-exempt in a regular account.

Lee stressed, "Even a homemaker with no current wage income should actively use pension accounts as a strategic tool to grow retirement assets as much as possible—through measures like rolling over ISA maturity funds—and to protect against taxes and national health insurance premiums."

The Tax and Investment Q&A series, based on consultations with KB Securities tax specialists, is published on the fourth week of every month.

nodelay@fnnews.com Park Ji-yeon Reporter