The longer the war drags on, the harder Korean stocks get hit... Korea Composite Stock Price Index (KOSPI) could fall to 5,500 [US–Iran war]

- Input

- 2026-03-03 18:26:09

- Updated

- 2026-03-03 18:26:09

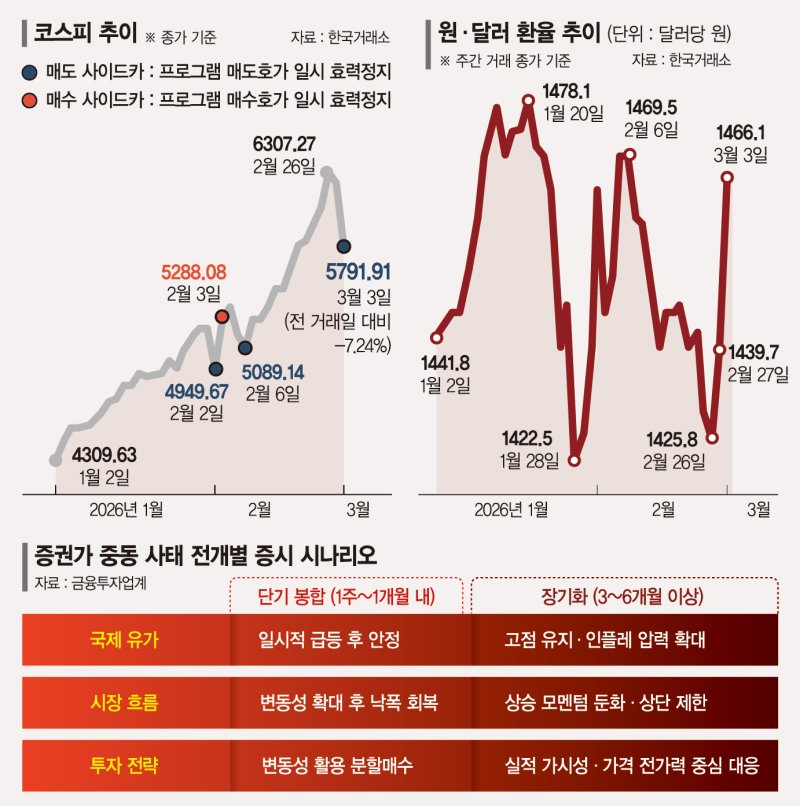

On the 3rd, analysts said the sharp sell-off in the domestic market that day reflected an immediate reaction to geopolitical risks, combined with profit-taking after a strong rally since the start of the year. With the Korea Composite Stock Price Index (KOSPI) having surged 48.17% in just January and February, the emergence of Middle East–related risks prompted foreign and institutional investors to accelerate profit-taking, according to experts.

That said, many expect that if the crisis is resolved quickly, the move will remain a short-lived bout of risk-off sentiment. Whenever geopolitical tensions rise, investors tend to increase their allocation to safe assets in the short term and cut back on equities. Looking at past Middle East conflicts, however, there have been many cases where, after a brief spike in oil prices, stock markets gradually recovered their losses as long as there was no actual disruption to supply. If the real-economy impact remains limited this time as well, analysts project that markets will shift from heightened volatility to a gradual recovery phase.

Lee Sang-yeon, an analyst at Shinyoung Securities, explained, “Given the strong rally in the Korea Composite Stock Price Index (KOSPI) at the start of the year, the index level itself created a favorable environment for investors to lock in profits.” He added, “Looking back at recent periods of rising geopolitical risk, during both the Russo-Ukrainian war and the Israel–Hamas war, the KOSPI recovered all of its losses from the event day within a week.”

Brokerages are most wary of a scenario in which the war drags on. If elevated oil prices are sustained at high levels, they could cap the upside for equities. Rising energy costs can push up inflation expectations, weakening hopes for interest-rate cuts and in turn putting pressure on valuations. In that case, the market could move beyond a short-term volatility phase and enter a more structural shift in which the upward momentum slows.

Kang Dae-seung, an analyst at SK Securities, said, “If high oil prices persist, they could become a factor driving global inflation higher.” He continued, “If this slows the pace of monetary easing through the inflation channel, the momentum for supplying real liquidity to markets is likely to weaken.”

Some, however, believe that the correction in the Korean market will be limited, as the direct impact on the semiconductor sector—the key driver of earnings improvement—is not expected to be large. The geopolitical risks stemming from the Islamic Republic of Iran (Iran) are not seen as factors that would fundamentally damage the semiconductor cycle, which sits at the core of the KOSPI earnings cycle.

Yoo Myung-gan, an analyst at Mirae Asset Securities, noted, “More than 60% of memory semiconductor demand comes from data centers, most of which are located in the United States of America (US).” He added, “The share of semiconductor raw materials sourced directly from regions adjacent to the Islamic Republic of Iran (Iran) is limited, and suppliers’ conservative capital expenditure stance amid macro uncertainty could actually help support memory semiconductor prices.”

Experts are opening up the possibility that, in the short term, the lower end of the KOSPI trading band could extend down to the 5,500 level. However, they also agreed that if valuations fall to around 1.55 times on a 12‐month forward price-to-book ratio (P/B ratio) basis, and assuming the earnings recovery led by memory semiconductors remains intact, the likelihood of an additional sharp decline will be limited.

koreanbae@fnnews.com Bae Han-geul Reporter