"Even with 2 Billion Won in a Stock Account, I Can't Use It"... The Disease That Eats Away at Life After Retirement – and Even Your Children's Lives [Retiree X’s Plan]

- Input

- 2026-02-28 08:30:00

- Updated

- 2026-02-28 08:30:00

[Financial News] "If you drink this, you have to date me." The film "A Moment to Remember," starring Jung Woo-sung and Son Ye-jin, became a symbol of melodrama for people in their 20s and 30s at the time. It tells the story of a lover who is losing her memory and the partner who watches over her. Back then, dementia felt like a dramatic device, a narrative tool to make love stories more heartbreaking.

Early-onset dementia: 90,000–100,000 people

Today, things are different. For Generation X, dementia is no longer just something on a movie screen; it shows up in the statistics.

According to the National Health Insurance Service (NHIS),the number of dementia patients in their 50s rose from 3,179 in 2006 to 6,547 in 2011, more than doubling in five years,a surge of over twofold in just half a decade. There are no recent official figures, but given the trend, the current number may have already exceeded 50,000.

In fact, early-onset dementia, which develops before age 65, accounts for about 8–10% of all dementia cases. In absolute numbers, that is estimated at roughly 90,000 to 100,000 people.

People in their 50s are at the stage of starting or finalizing their retirement plans. They are paying off mortgage loans, covering their children's education costs, and managing assets for old age.If dementia strikes at this point, the problem goes far beyond a medical diagnosis and shakes the entire household structure. Income falls, expenses rise, and decision-making ability weakens. The basic assumptions behind retirement planning can collapse.

The most feared disease: dementia

Fear of dementia is not just an emotional reaction; it shows up clearly in the numbers.

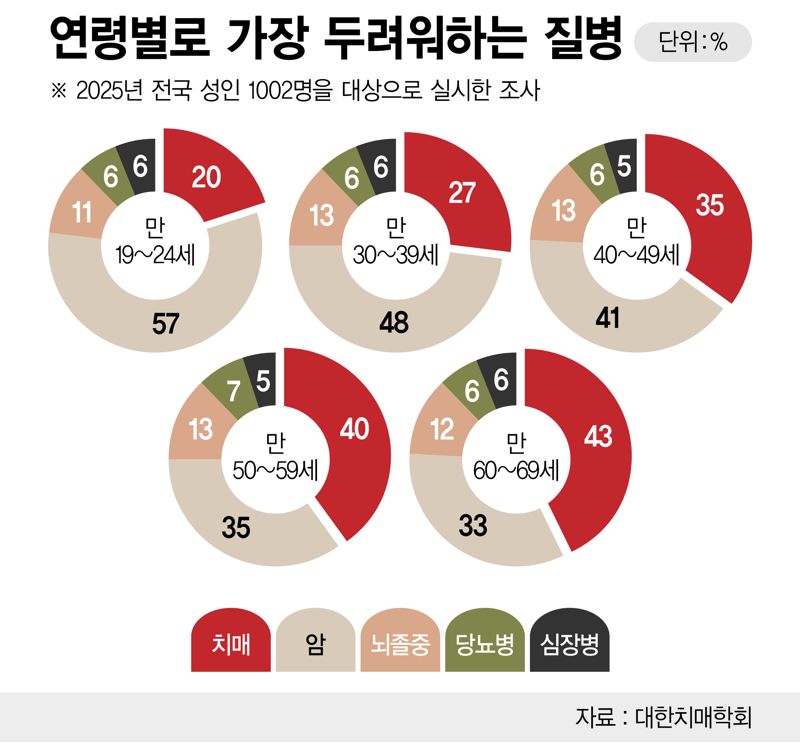

In a 2025 survey by the Korean Dementia Association of 1,002 adults nationwide, dementia ranked first or second among the most feared diseases by age group. People aged 19–24, those in their 30s, and those in their 40s named cancer as their top concern, but people in their 50s and those 60 and older all chose dementia. Notably, even relatively younger generations cited dementia as the second most worrying disease after cancer.

The frequent missing-person alerts that pop up on smartphones also show this reality. "We are looking for △△△, who has been wandering in ○○. If found, please call 112." Many of the missing are older adults. Not all of them necessarily have dementia, but it is hard to say these cases are unrelated to cognitive decline. Dementia has become part of everyday scenes, not just a statistic.

An era of 1 million dementia patients, and one in four is a potential patient

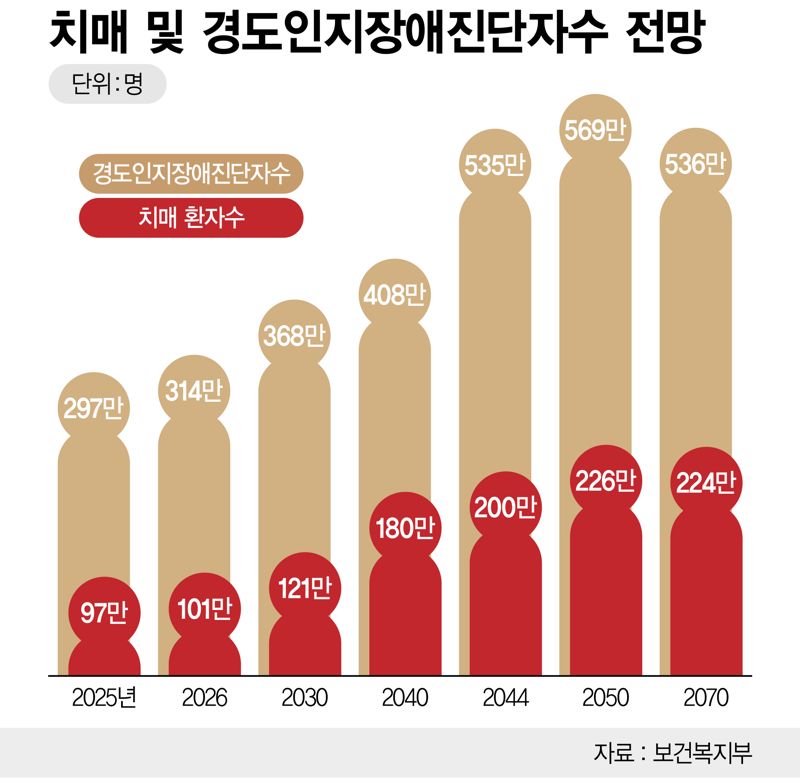

The concern is becoming reality. In 2026, Korea will enter the era of "1 million dementia patients." Dementia is no longer an issue limited to a small group of the elderly or to certain families.

According to a recent epidemiological survey on dementia by the Ministry of Health and Welfare, the number of dementia patients aged 65 or older in Korea is estimated at about 970,000 in 2025, with a prevalence rate of 9.17%. The figure is expected to reach 1.21 million in 2030 and 2.26 million by 2050.

The pace is far too fast to be dismissed as a natural consequence of an aging population.

Another number deserves even more attention: the population with mild cognitive impairment (MCI), which is far larger than the number of dementia patients. Mild cognitive impairment refers to a state in which memory or judgment has begun to decline, but daily life is still manageable. Put simply, it is "the stage right before dementia."

As of 2025, the estimated number of people with mild cognitive impairment in Korea is about 2.98 million, or roughly 28% of seniors aged 65 or older. In other words, more than one in four older adults is "not yet demented, but could cross that line at any time."

This number is projected to rise to 3.68 million in 2030 and to about 5.68 million by 2050.Given the speed at which the elderly population is growing, dementia is already a "present, ongoing reality," not a "future that will eventually arrive."

The cost backlash: the biggest expense item in retirement planning

Dementia is one disease among many, but its impact spreads across every aspect of life. It affects not only the patient but the entire family.Hospital bills and nursing home fees rise, and continuous caregiving labor is required.In the past, caregiving was absorbed within large extended families. Now it has shifted to nursing homes, in-home care, and paid caregiving services. Care has been externalized, and the costs have been individualized.

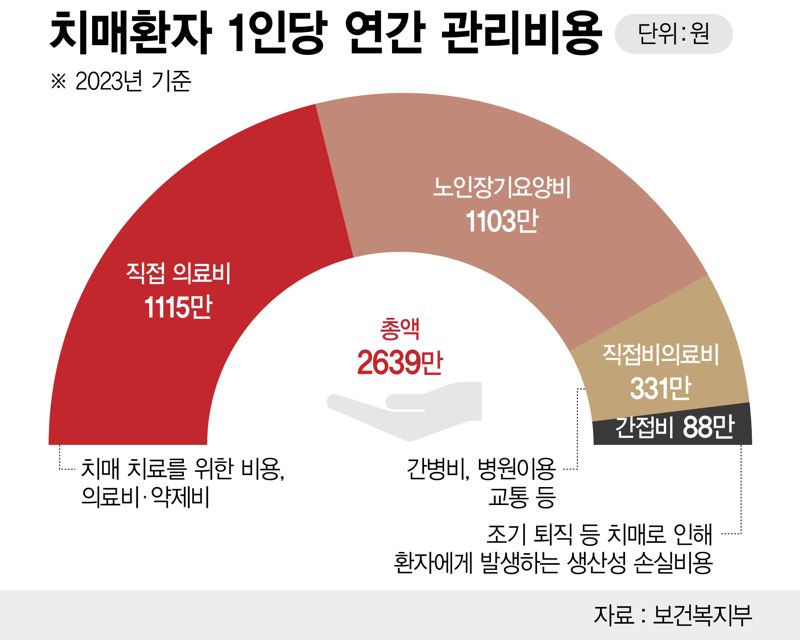

According to the Ministry of Health and Welfare,the annual management cost per dementia patient in 2023 was 26.39 million won,including 11.15 million won in direct medical costs, 11.03 million won in long-term care benefits, 3.31 million won in direct non-medical costs, and about 880,000 won in indirect costs. Direct medical costs cover medical treatment and medication for dementia, while direct non-medical costs include caregiving expenses and transportation to and from medical facilities.

This annual dementia management cost exceeds 40% of the average household income in the same year, which was about 60.29 million won.

Of course, families do not pay all of this out of pocket. Korea has a strong safety net in the form of Long-Term Care Insurance.Once a person is assessed and assigned a care grade, the state covers 80% of the cost for institutional care such as nursing homes and 85% for in-home services such as visiting care.Even after adding food costs and non-covered items, the actual monthly burden on families can be reduced to around 600,000–1.2 million won.The problem is that even this "reduced cost" becomes a fixed monthly financial blow for those who are not prepared.

In reality, Park Cheol-won (a pseudonym), a 57-year-old living in Gwanak District in Seoul, saw his bank account usage change dramatically after his mother was diagnosed with dementia three years ago. He now spends about 800,000 won a month on a care worker, diapers, and hospital bills. One day it hit him: "What about me? My kids will end up going through the same thing for me." He recalculated his retirement costs. Dementia is not someone else's problem. As you read this article, you need to figure out what size bill dementia could present to your own household.

A deeper shift: the erosion of decision-making power

What makes dementia truly frightening is not simply the loss of memory.The more fundamental problem is the weakening of decision-making power.

As the disease progresses, patients find it increasingly difficult to decide on their own to withdraw savings, cancel insurance policies, or sell real estate. At that point, asset "ownership" and asset "control" begin to diverge.

You may have assets but be unable to use them easily. Banks insist on verifying the account holder's identity, and financial institutions worry about disputes. Families trying to raise money quickly for hospital bills find themselves stopped by procedures and paperwork.

At this point, dementia moves beyond the realm of medicine and into the realm of personal finance.

Traditional retirement planning has been all about numbers: how much to save, how long the money will last, what rate of return to expect on pensions. In a society living with dementia, however, the core question changes.

Once I can no longer make decisions, how do I want my money to be used? If you cannot answer this, the size of your assets may not matter much.

Systems already in motion

Since announcing the first Comprehensive Plan for Dementia Management in 2006, the government has been rolling out new measures every five years.

▶Dementia Relief CenterThere are 256 centers nationwide that provide early screening, family counseling, case management, and linkage to long-term care grades. For families who do not know where to turn after a diagnosis, these centers serve as the first gateway.▶Long-Term Care InsuranceOnce a person is graded, they can receive services such as in-home care, day and night care, and admission to care facilities. There is some out-of-pocket payment, but it is very different from bearing the full cost alone.

▶Expansion of public guardianship and asset-management supportThe government is also strengthening systems to protect the rights and manage the assets of people with dementia. Plans under discussion include expanding public guardianship and piloting programs to support asset management.

Recently, the government announced the Fifth Comprehensive Plan for Dementia Management (2026–2030). The plan calls for expanding prevention and early screening, strengthening community-based care, and broadening public guardianship and asset-management support. It signals an intention to treat dementia not only as a medical issue but also as a matter of daily life and rights protection.

However, these systems do not operate automatically. You have to know about them, apply for them, and incorporate them into your planning before they can truly function as a safety net.

What Retiree X needs to check right now

Experts advise that people prepare for dementia in advance.

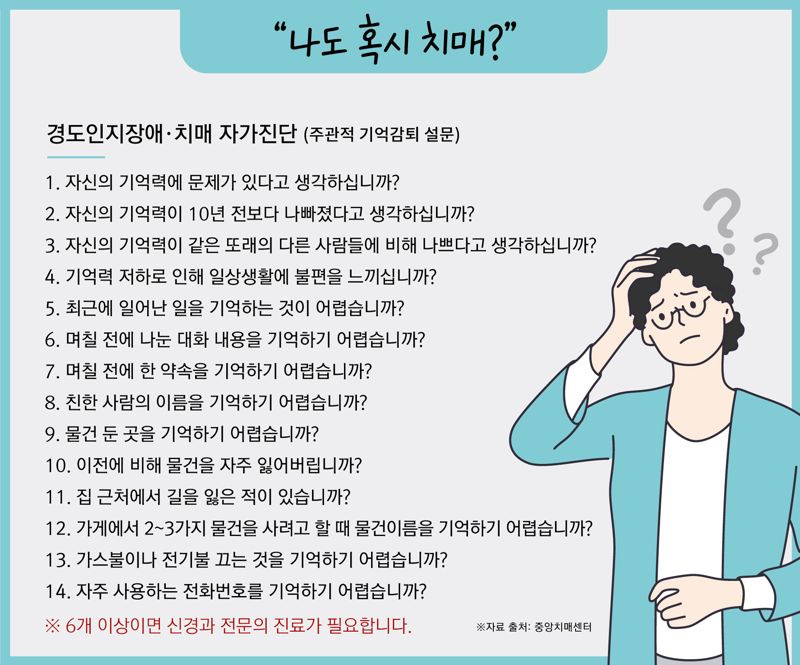

□Do you know where your parents' assets are and how they are structured?□ Is the beneficiary designation on insurance policies clear?□ Have you estimated the likely size of medical and long-term care expenses?□ Have you agreed on roles and responsibilities among siblings?□ Have you set up financial safety measures such as alerts for large transfers?□ Above all, have you started the conversation that says, "Let's decide this while we still have our judgment"?Preparation is not just an issue for the wealthy. Once decision-making ability declines, the range of available options shrinks rapidly.

Caregiving-related bankruptcy or tragedy is not about a lack of filial piety; it is about a structure that was never prepared.Dementia is not an individual misfortune but a constant in an aging society. Retirement planning can no longer be completed with pension calculators alone. It must expand to include the variable of cognitive decline.And one more question remains: If you have assets but reach a point where you cannot use them, what will you do? In the next installment, we will look at the moment when dementia freezes your money and examine the structure of "dementia money."

The old formula "retirement = exit" is collapsing. In an era when average life expectancy is 83, and Generation X is entering full-scale retirement, the very concept of retirement is being redefined. Retiree X’s Plan tells the stories of their "second act in life."[Retiree X’s Plan]is published every Saturday morning for our readers. Subscribe to the reporters' pages to receive it more conveniently.

kkskim@fnnews.com Kim Ki-seok and Jung Myung-jin Reporter