Shadow banking expands amid economic downturn: "More securitization of loans and card receivables"

- Input

- 2026-02-09 06:13:00

- Updated

- 2026-02-09 06:13:00

According to the financial investment industry and Korea Investors Service (KIS) on the 9th, securitization of loan receivables reached 16 trillion won last year, up 43.3% from a year earlier.

KIS analyzed that demand for alternative funding has grown mainly among companies rated A or below, leading to an increase in securitized products backed by loan receivables.

The industry expects securitization demand to remain strong as an alternative funding tool for companies. Issuance of primary collateralized bond obligations (P-CBOs) totaled 5.6 trillion won, up 11.5% from the previous year. P-CBO issuance is closely tied to the scale of support for small and mid-sized companies and to the policy stance of related public institutions.

A Primary Collateralized Bond Obligation (P-CBO) structure provides credit enhancement for bonds issued by companies with low credit ratings that find it difficult to sell bonds directly. Policy finance institutions such as credit guarantee agencies back these bonds, and the enhanced securities are then sold to the market. In the current downturn, funding strains at small and mid-sized firms are effectively driving up P-CBO issuance.

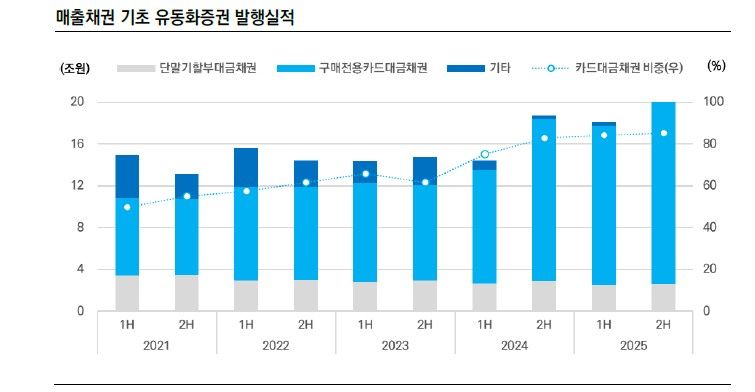

Financially sound companies have also increased their funding through securitized products. Issuance of securitizations backed by card payment receivables from corporate members reached 33.6 trillion won, a 27.6% rise from 26.3 trillion won a year earlier. Lee Eung-jun, a researcher at KIS, said, "Securitization of card payment receivables is generally used as a way for card companies to book off (sell) receivables and for corporate members to secure liquidity." Major participants include Hyundai Card, Shinhan Card, and Lotte Card.

He explained, "Based on the credit ratings of corporate members, A1 accounts for more than half, and together with A2, makes up most of the exposure."

Kim Bong-hwan, a researcher at Korea Ratings Corporation, stated, "Securitization of trade receivables related to corporate purchase payments increased sharply from the previous year as issuance demand grew for corporate liquidity management."

He added, "When Homeplus filed for rehabilitation proceedings last March, about 400 billion won of securitized products backed by Homeplus trade receivables tied to corporate purchases went into default." He went on, "As a result, the increase in issuance of securitized products backed by trade receivables from lower-rated companies was relatively limited."

However, some experts argue that securitization of card payment receivables needs closer monitoring. They point out that it effectively increases non-loan, debt-like funding that does not appear as borrowings on financial statements.

Non-loan, debt-like funding refers to financing transactions that are not recognized as liabilities or borrowings on the balance sheet. Such funding has characteristics that lie somewhere between traditional borrowings and other items such as other payables, off-balance-sheet liabilities, or equity.

Kim Ga-young, a researcher at NICE Investors Service, pointed out, "Securitization of purchasing cards (card sales receivables) is a major borrowing-like liability that is not recorded as borrowings." She added, "Because it is recognized as a liability in accounting, it does not affect leverage ratios such as the debt ratio or equity ratio, but it is classified as other financial liabilities rather than borrowings, which means indicators based on total and net borrowings do change." In other words, even when companies raise funds through card sales receivables, their total and net borrowings do not increase.

She continued, "If non-loan, debt-like funding is used repeatedly and grows excessively in scale, there is a risk that financial soundness indicators alone will underestimate a company's actual repayment burden and financial risk." She warned, "If refinancing problems arise, these structures can become a link between liquidity crunches and credit rating downgrades, so related transactions are a key monitoring factor in credit assessments."

khj91@fnnews.com Kim Hyun-jung Reporter